Weekly Research Briefing: Half or Quarter?

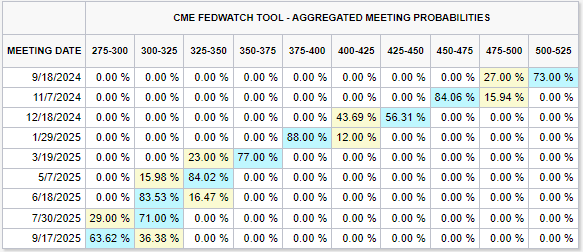

Wednesday brings the long awaited FOMC meeting where the Fed will begin its official wind-down of restrictive Fed Fund rates. While the markets assumed that a 25 basis point cut was in the bag, recent winks, nods and quiet conversations with Fed whisperers have pushed the market toward the likelihood of a bigger 50bp cut. The increased appetite seems to be originating from further concerns over the slowdown in new hiring. While the economy still has many positive signs, employers have been more reluctant to put up the help wanted sign. So rather than cut by 25bps and get an earful from the markets, the FOMC might cut 50bps and give companies a reason to grow into the year end. Continued falling inflation shows that they have room to cut. The final answer will be read and discussed on Wednesday.

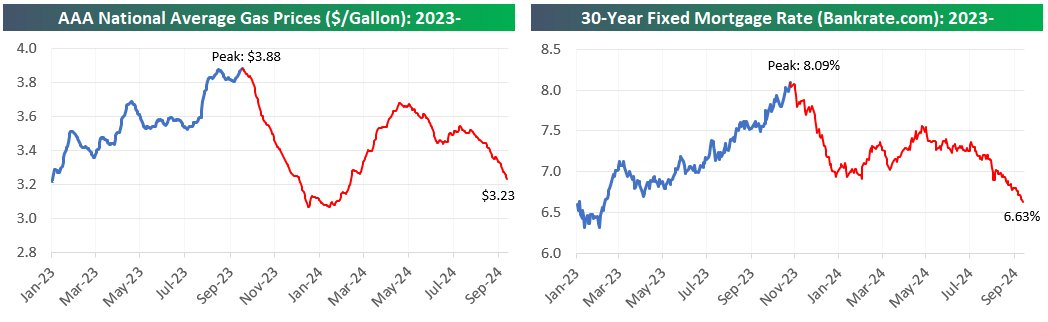

In the meantime, the U.S. Treasury yield continues to dig new lows with the 2 year now at 3.56%. Recall that this was at 5% in May. The Dow Jones Industrial Average is at a new all-time high. Mortgage rates are at 16 month lows. And national average gasoline prices are about to tap $3. The Fed just reported that U.S. household net worth has never been higher. Financial and housing assets have the wind at their backs right now as cash once again is beginning to look like trash. If the Fed pulls the 50 level, watch money market funds assets move into other asset classes.

While the FOMC meeting will get all the attention this week, the U.S. economy does have a big slate of data from the manufacturing, retail sales and housing sectors of the economy. Listen for any comments about future interest rate cut impacts. The big two-week bubble of investor conferences is now history as most companies move into their blackout periods ahead of the end of the Q3. Most of the tidbits and items that flowed from the CEO's and CFO's were positive about the state of the average consumer and the direction of interest rates. There were a few clunkers (like Ally Financial and Adobe), but for the most part, the reads were in-line to better (see credit card company and data center exposure comments for some real optimism). Some good stuff below. Have a fun FOMC day, great week and let us know how we can help.

The market is now pricing in a 60% chance of a 50 bps rate cut this month...

Former Fed head, Bill Dudley, wants a big cut this week...

The two objectives of the Fed’s dual mandate — price stability and maximum sustainable employment — have come into much closer balance, suggesting that monetary policy should be neutral, neither restraining nor boosting economic activity. Yet short-term interest rates remain far above neutral. This disparity needs to be corrected as quickly as possible.

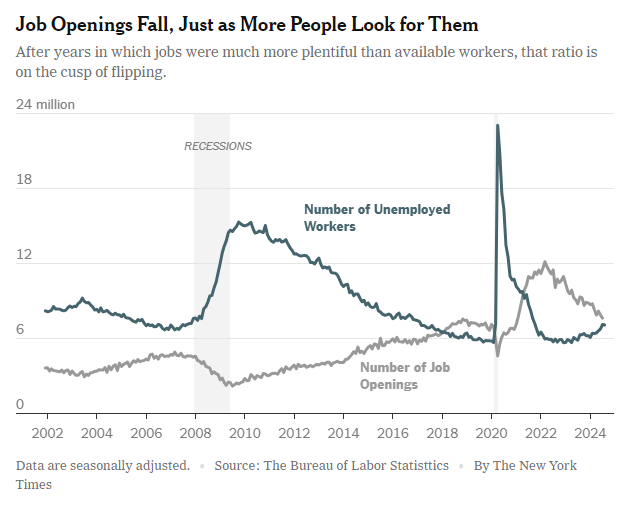

Consider the economic data. The unemployment rate has risen by 0.8 percentage points from its trough in January 2023. In the past three months, payroll employment has increased at the slowest pace since 2020. Wage inflation has moderated to less than 4%, while the Fed’s preferred measure of consumer price inflation is running around 2.5%. Although core consumer prices rose a bit more than expected in August, the move was driven by categories that tend to lag (insurance and shelter), and the latest producer price report suggests that the core personal consumption expenditures index will be considerably tamer.

One could even argue that the downside risks to employment outweigh the upside risks to inflation. When the labor market deteriorates beyond a certain point, the process tends to be self-reinforcing. Every time the three-month average unemployment rate has risen by more than 0.5 percentage from its low point during the prior 12 months, the ultimate result has been much larger increase — at least 1.9 percentage points — and a recession. The threshold might be higher this time, given that the rise in the unemployment rate has been fueled largely by rapid labor force growth. But this doesn’t invalidate the idea that a tipping point exists, and that the labor market has either crossed or is approaching it.

Greg Ip asks what Fed mistake would you rather make?

The Fed doesn’t get to wait for perfect knowledge before acting. It always risks doing too much, or too little. The question is, which is worse? Cutting rates half a point isn’t riskless. Long-term Treasury bond yields are already lower than short-term rates—a relationship called an inverted yield curve—and could fall even further, pulling down mortgage rates. Stocks could turn frothy. That would stimulate spending.

Inflation could also prove stickier or even edge higher, especially if oil rebounds or tariffs are raised. If that happens, the response should be straightforward: Don’t cut again. Rates would still be relatively high.

Cutting only a quarter point looks riskier, though. One reason oil and other commodity prices such as copper have fallen is because the global economy, in particular China and Europe, looks sickly. Mounting auto loan and credit card delinquencies show higher rates are biting. The yield curve is inverted because markets think interest rates ought to be lower.

The Fed has already erred on the side of moving slowly. In hindsight it should have cut in July given the weak employment and generally tame inflation data that followed. If the Fed only cuts a quarter point now and more weak data arrive, it would be even further behind the curve.

Time for the Fed to end the downside risk?

...some onlookers are beginning to worry that the Fed might fall behind the curve if it reacts too gradually — something that would leave it scrambling to lower borrowing costs quickly enough to keep the job market from falling to pieces.

“Not all slowdowns lead to recessions, but all recessions start with slowdowns,” said Skanda Amarnath, executive director at Employ America, an employment-focused research and advocacy group. “I think the data is signaling a certain amount of urgency.”

The Fed has been approaching rate cuts cautiously because it does not want to risk taking its foot off the economic brakes too early or too swiftly, allowing the economy to heat back up and making it harder to fully stamp out inflation.

But caution on the inflation front could translate into risk-taking on the employment front...

“It should be clear to everyone that many prepandemic economic relationships have not proven to be good policy guides post-pandemic,” Christopher J. Waller, a Fed governor, said in a recent speech. “While I don’t see the recent data pointing to a recession, I do see some downside risk to employment that I will be watching closely.”

Nomura's thoughts on a 50 basis point rate cut are well put...

When I hear people say “Well, 50 bps is telling the market that the Fed thinks we have a big problem and could lead to a risk-off tantrum,” my thought is that NOTHING in this steroidal, Frankenstein — cycle has been normal (unprecedented Monetary and Fiscal interventions, Market overshoots & undershoots, with violent turns and regime shifts creating Momentum shocks), as the fact is that we have experienced 11 Fed hikes in a year and a half, including multiple 75 bps blasts . . . so making commensurate — type moves on the policy reversal should kinda be expected, no?!

Anthony Noto speaks for most CEOs right now...

"And I was on CNBC last week and someone said, well, what's your view on rate cuts. And I made the point that if you are going to cut 75 basis points between now and year-end, you're much better off cutting 50 basis points now because you'll spur more economic activity next year because corporations are making decisions about next year now. And if they know they have 50 basis points on a huge balance sheet of debt, they could do more hiring, they could do more investing even having that information." – SoFi Technologies CEO Anthony Noto

Meanwhile the economy has several good areas... like cruise ship travel...

@carlquintanilla: JPMORGAN, on cruise lines: “.. demand backdrop for cruise remains ‘strong’ with ‘zero signs of softening in any lead indicator’ (i.e. booking curve, price or onboard spend). “.. Putting the pieces together .. raising 3Q EPS across the sector with our bottom-up model work pointing to mid-single- digit(+) yield growth in FY25 ..”

Higher end furniture demand is also turning up according to Restoration Hardware...

@bluff_capital: $RH "We are pleased to report that demand was up 7% in the second quarter and has continued to inflect positive, gaining momentum each month with July finishing up 10%. Demand accelerated into the third quarter with August up 12%."

And it sounds like Walmart had a solid back-to-school season...

Citi analysts citing meetings with Walmart management: It sounds like they had a really good back-to-school season, and management is optimistic about H2; They have not seen any “fraying” within their customer base - They are gaining share in both their core customer base as well as with higher income customers, and newer customers are sticking with them (and shopping across categories).- We came away believing WMT’s topline momentum and market share gains continue, most recently highlighted by a strong back to school season.

(TradeTheNews)

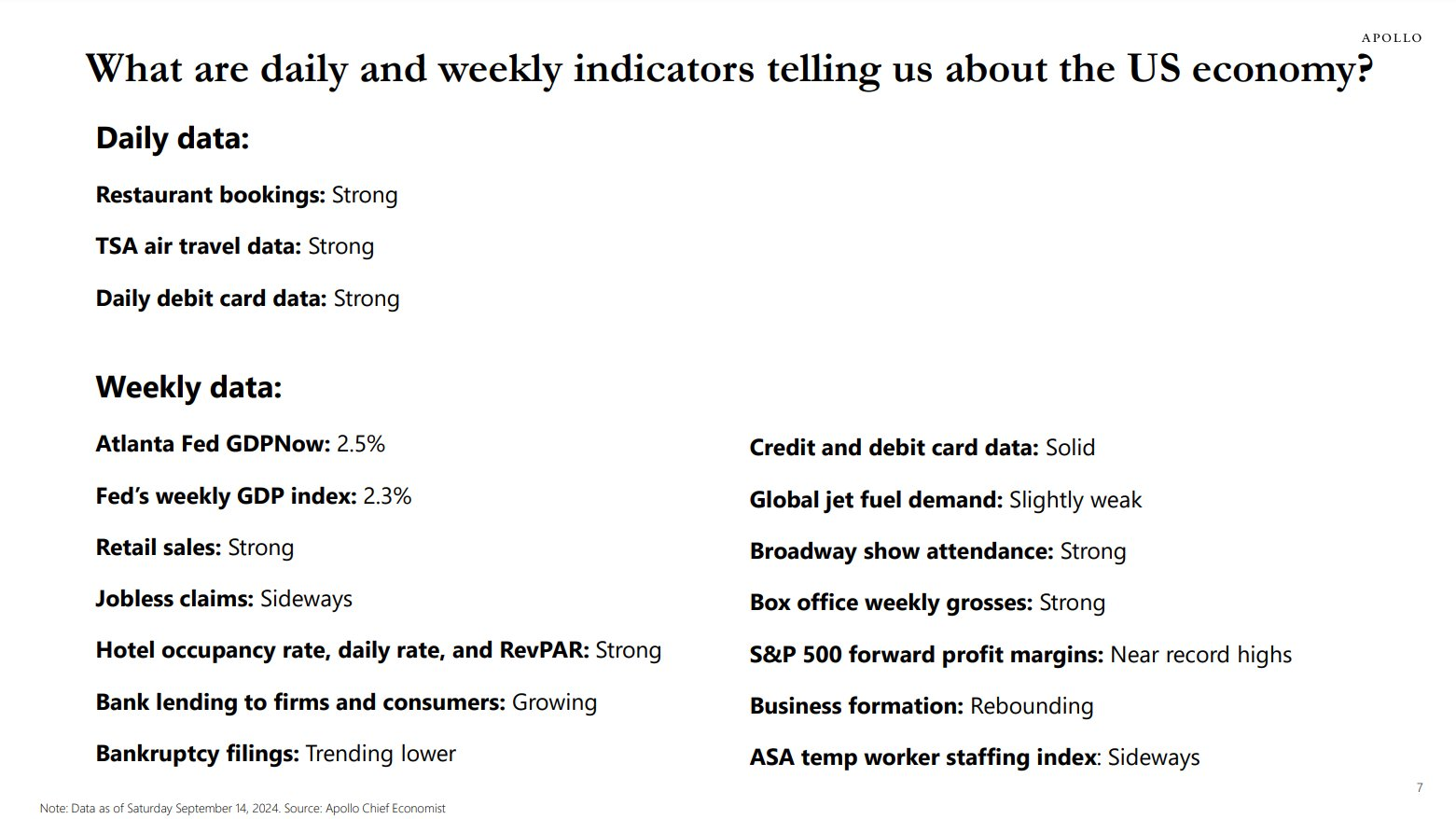

Even Torsten Slok's economic data monitoring shows an economy far away from recession...

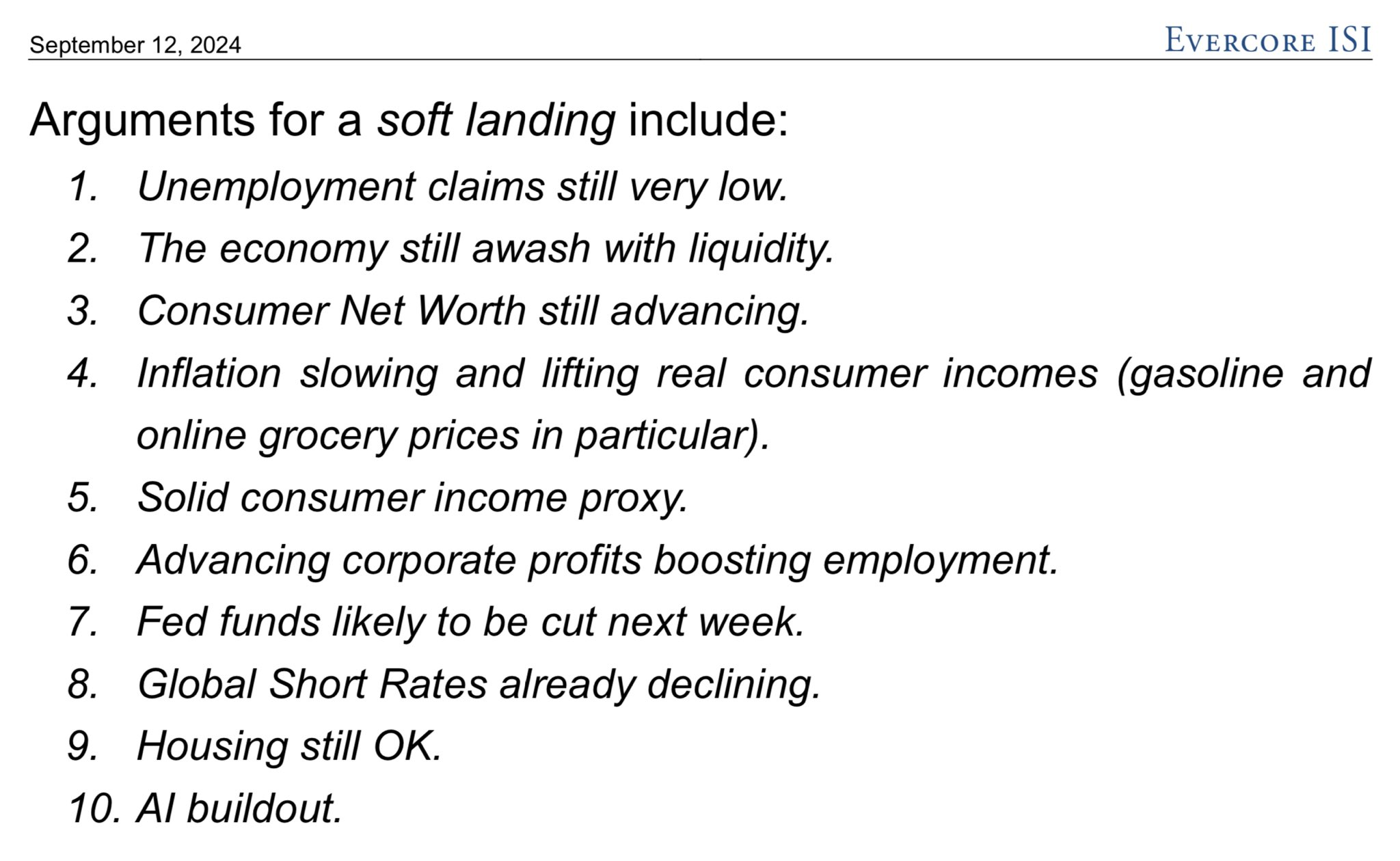

One of the most listened to economists in the market threw in the towel last week on a 'hard landing' call...

Ed Hyman at Evercore ISI: “History and experience say to stick with a hard landing outlook. However, the hard math that our team has reviewed says flip to a soft landing outlook. And that’s what we’re doing.”

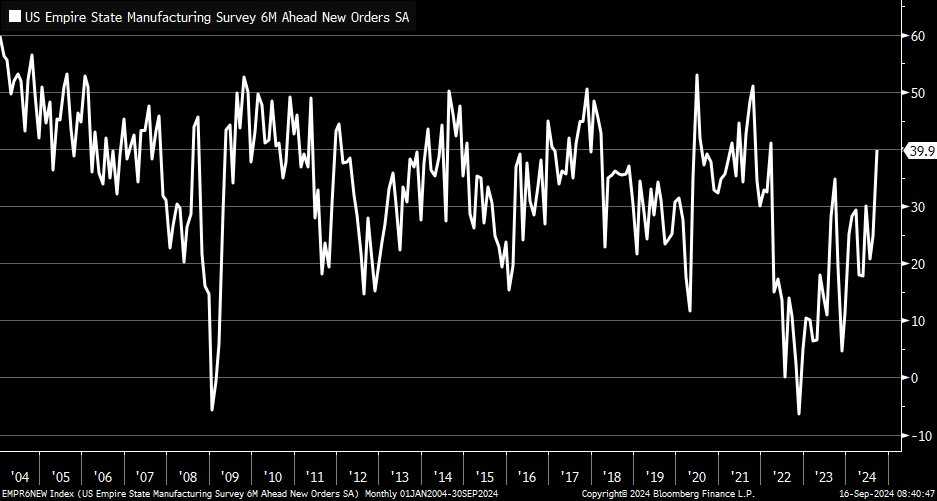

As for Monday's data, the N.Y. Fed manufacturing new order book jumped to 30-month highs...

@KevRGordon: Empire Manufacturing Index 6-month new orders outlook soared to +39.9 in September ... best since March 2022

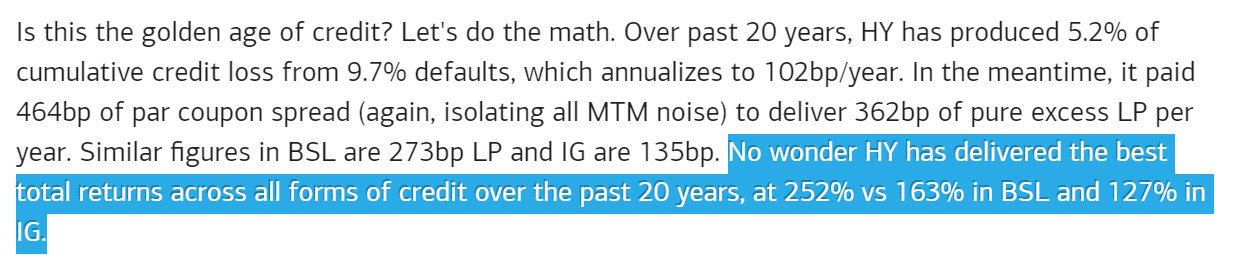

And one more time, the higher risk credit markets remain in the zone...

@tracyalloway: "The golden age of credit"" by the numbers, via BofA:

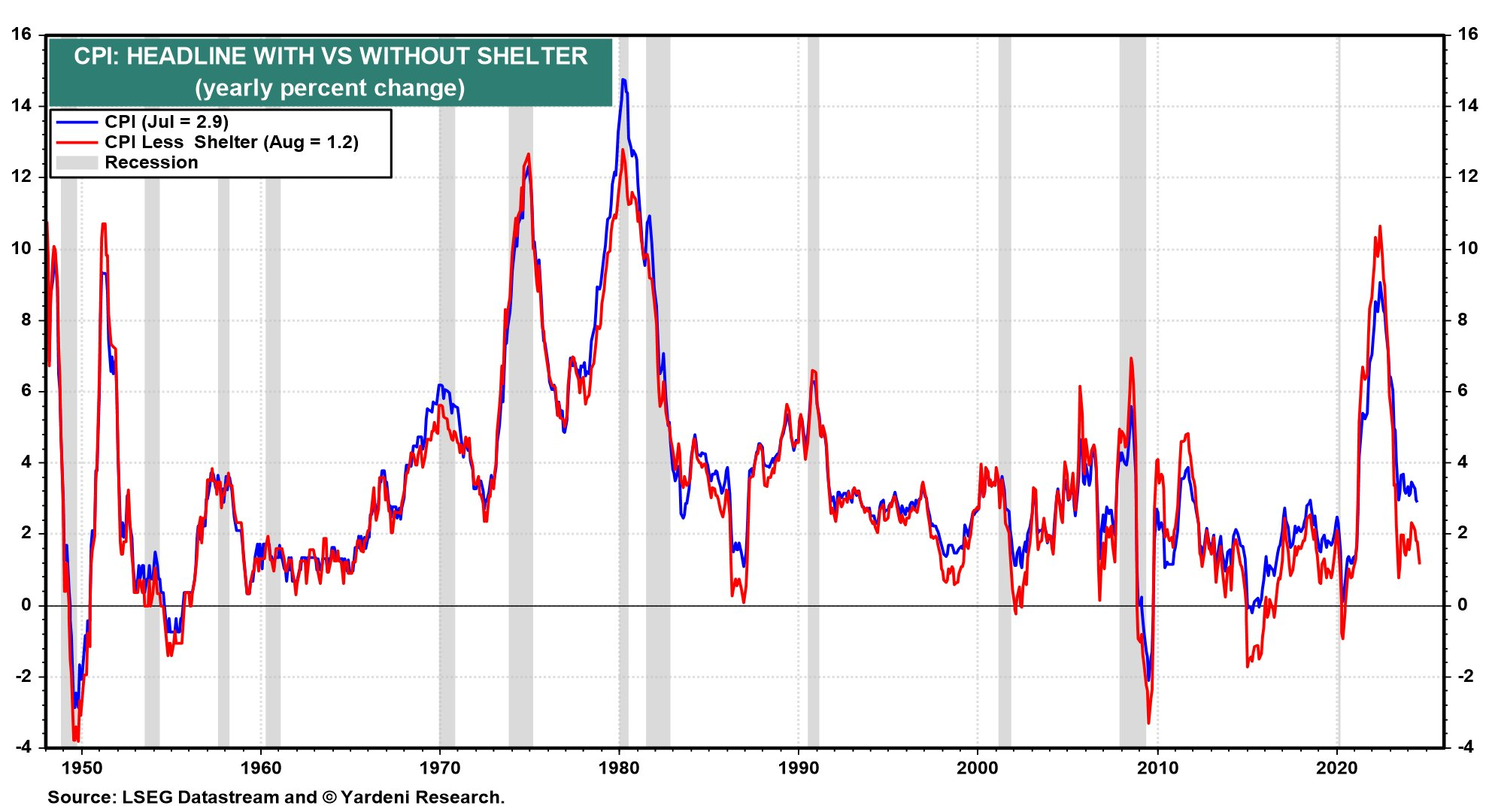

Last week's inflation reads put up another solid set of declines outside of shelter costs...

@ericwallerstein: CPI is now running at 1.2% y/y ex-shelter. Goods prices are deflating hard due to China & -10% y/y gas prices.

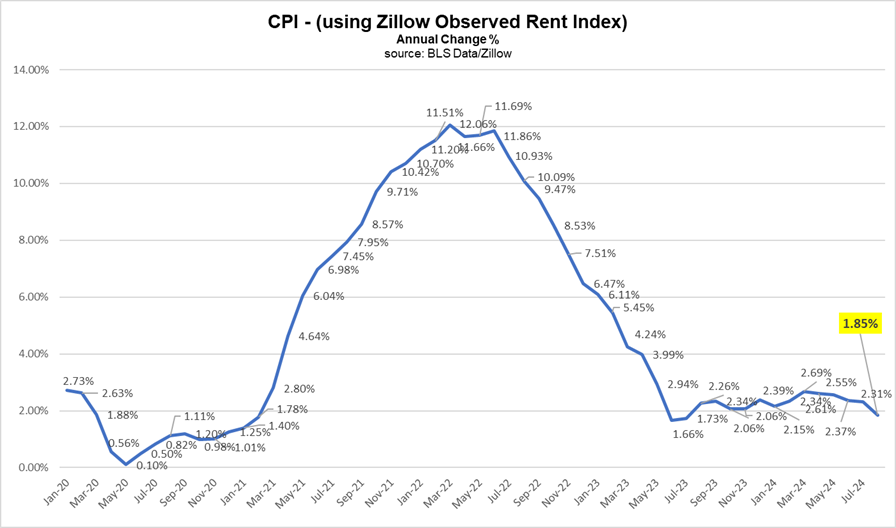

Swapping out lagged shelter costs for real-time shelter costs shows a CPI series below 2%...

@wabuffo: Inflation is now below 2% y-o-y in August if a private sector measure of shelter inflation (ZORI = 3.36%) is used instead of the BLS's measure (5.20%).

Good news for consumers as gasoline and mortgage rates race lower...

@bespokeinvest: There seems to be a race between gas prices and mortgage rates to see which one can go lower lately.

Back to Fed Funds rates, the market is hunting for 250 basis points of cuts through the end of 2025...

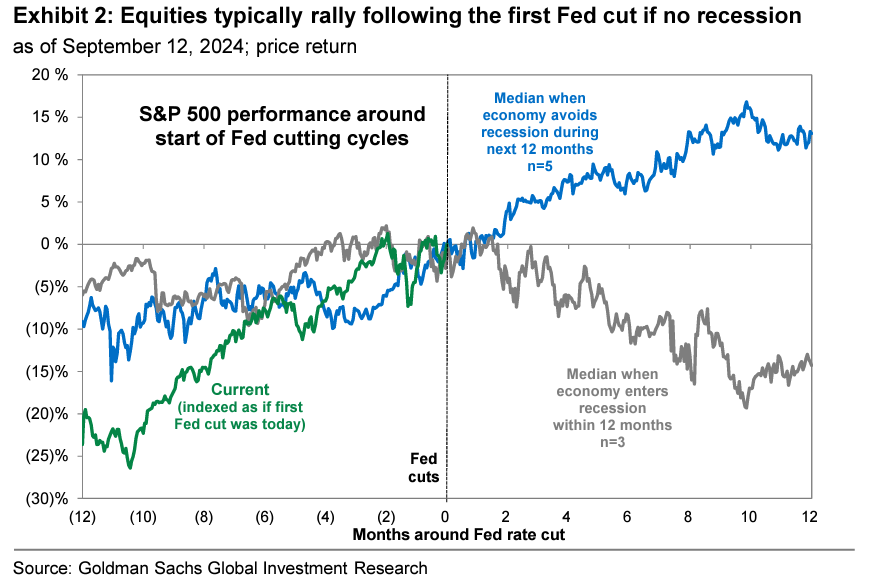

Public equities typically cheer the first rate cut when not accompanied by a recession...

(Goldman Sachs)

Looking through today's list of all-time new highs shows a broad sweep of the U.S. economy...

This broad group of stocks would not be marking new highs if a recession or even a significant slowdown was on deck.

(Barchart)

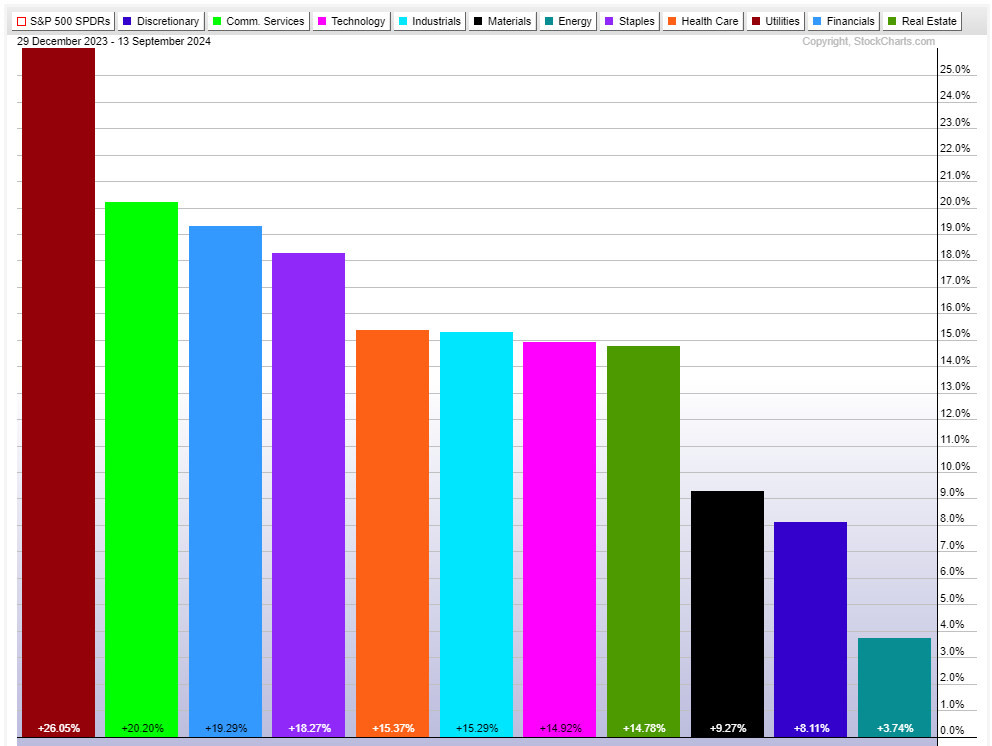

Who had Utilities, Communications and Financials for their 2024 market sector trifecta?

More importantly, take note that every sector is higher this year.

(StockCharts)

Who would have thought that a doubling in mortgage rates could produce such a return?

@GunjanJS: One of the largest home-building ETFs, ITB, is up 88% since the Fed's first interest-rate increase in March 2022. Over that time frame, mortgage rates surged from ~3% to 7.8%, touching a two-decade high.

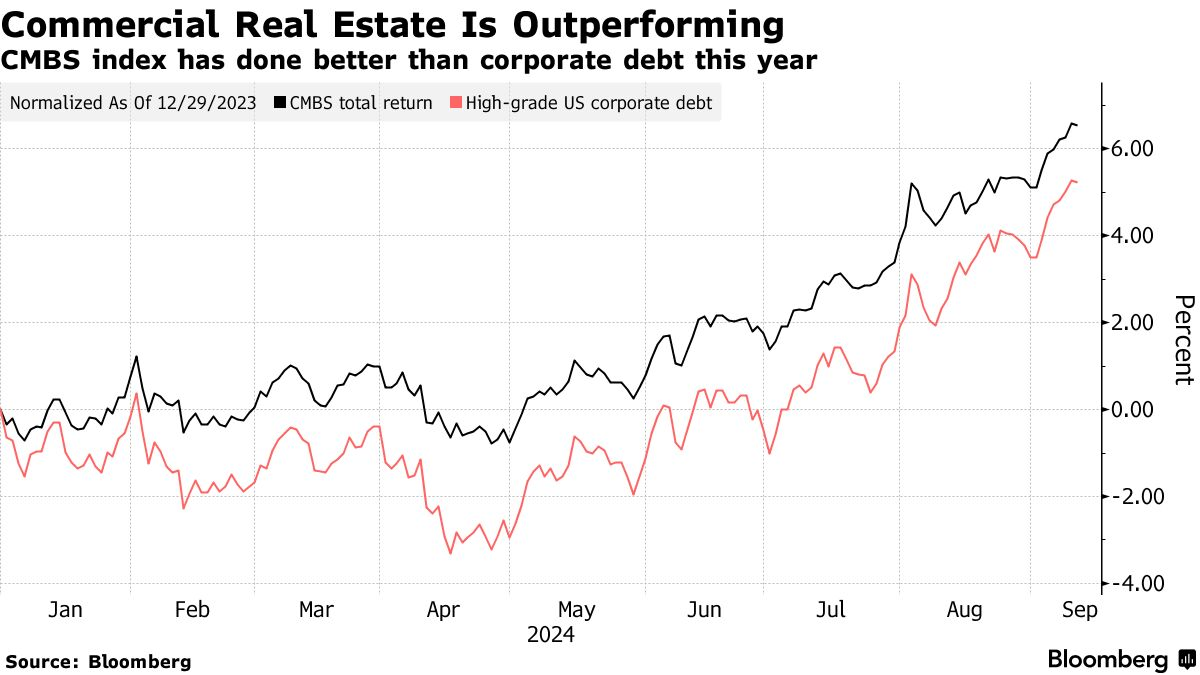

Not only is residential real estate outperforming...

Remember when they told you that Commercial Real Estate would take the economy into a recession? Yeah, that didn't happen. I hope that you tucked some RE exposure into your portfolio when the bear growls were loudest.

Yes, the average U.S. household is better off financially today than it was four years ago...

@BobOnMarkets: Are you better off now than four years ago? The Fed just reported that US household net worth rose to a new record as of June 30, to $163.8 TRILLION, up 37.7% from four years earlier. That exceeds the 26% gain between mid-2016 and mid-2020

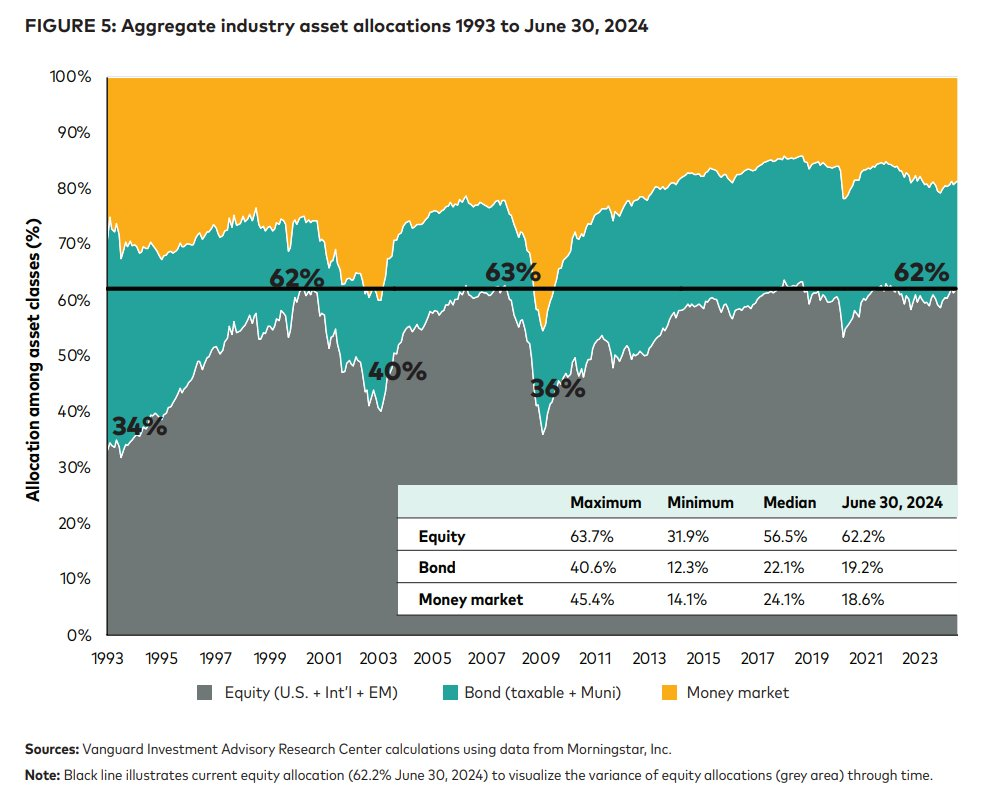

If you are a qualified investor, then you know that this chart is missing a fourth color...

Many top advisors that I know have 20-50% allocated into the private market asset class. And those advisors often are the ones that are growing their book of client assets.

(@AndrewThrasher)

Speaking of private equity, Mastercard creates a big win in buying the largest threat intelligence for $2.65 billion...

Mastercard said it would acquire cybersecurity company Recorded Future in a $2.65 billion deal, as intelligence on cyberattacks takes on greater importance amid growing threats from hackers.

The financial services giant said it would incorporate Recorded Future’s technology, including artificial intelligence, into its fraud prevention, identity and cybersecurity services. It expects to close the acquisition by the first quarter of 2025.

Recorded Future, based in Somerville, Mass., is being sold by private-equity firm Insight Partners. It provides threat intelligence to help clients assess cyber and geopolitical risk, and can monitor them for vulnerability to attack from unpatched technology and known hacker tactics.

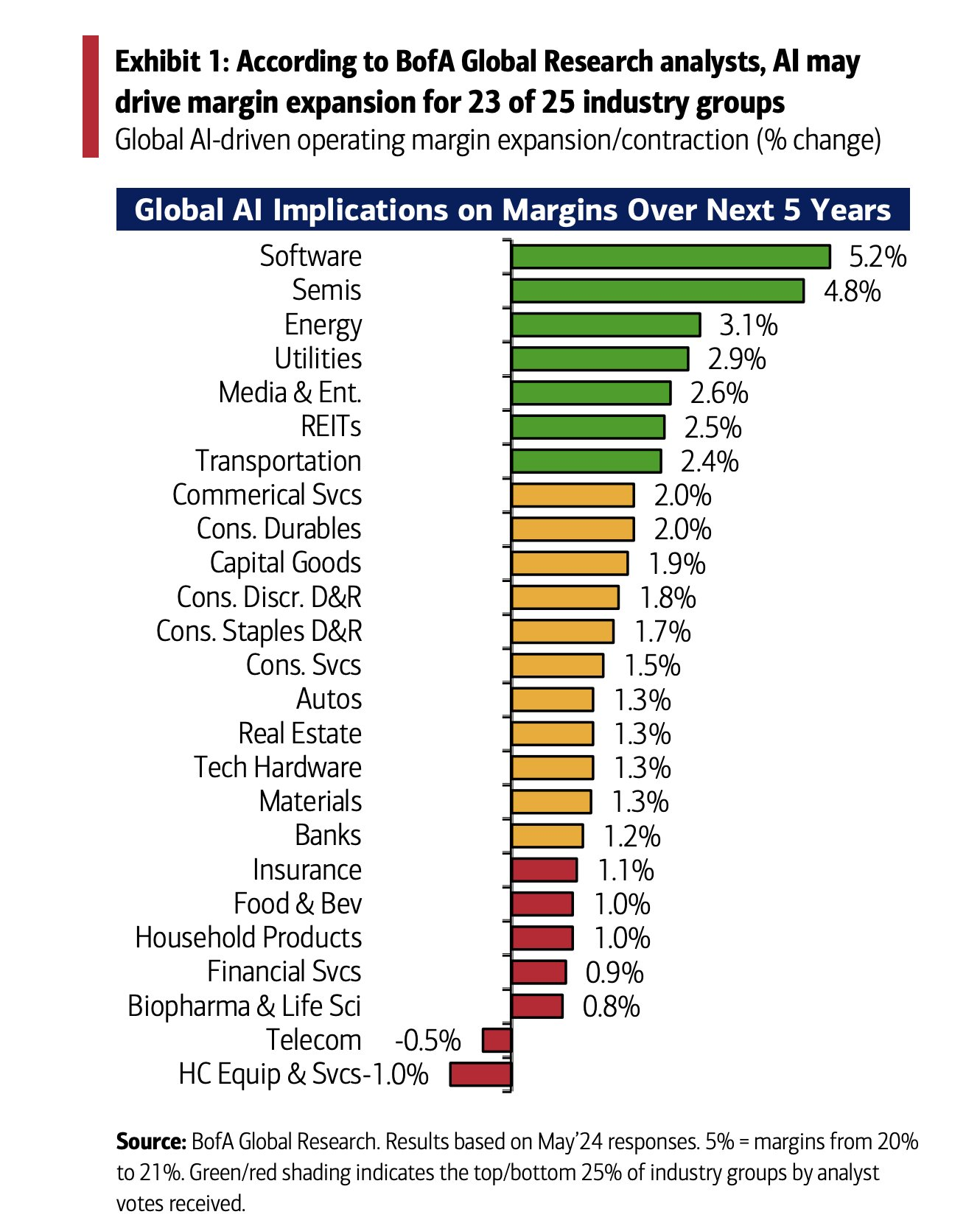

Yes, operating margins will continue expanding...

@SamRo: "According to BofA Global Research analysts, AI may drive margin expansion for 23 of 25 industry groups" - BofA

If you haven't watched this video from the Oracle analyst meeting last week, go find it...

If you or your clients are new to infrastructure, our team has put together a great piece to introduce this newer asset class that we will all be hearing much more about going forward. And infrastructure investing doesn't just mean the potential for long duration assets with high yields. There can also be opportunities to invest in infrastructure deals that are closer to early development of the asset and generally have much higher risk and historically had better return opportunities. Something for everyone. Click below to learn more.

@TheTranscript_: $ORCL CTO Larry Ellison: "I went to dinner with @elonmusk, Jensen Huang..& I would describe the dinner as Oracle & me & Elon begging Jensen for GPUs. Please take our money....No, no, take more of it. You're not taking out enough. We need you to take more of our money, please"

As a long time Nike stock and product fan, this was a tough long read. Hopefully this story goes into overtime...

Like Apple Inc., Nike was masterful at making product breakthroughs and engineering cultural movements along with them. Nike hired Donahoe to transform its selling machinery for the modern age, cutting out middlemen so it could get better margins from each sale. He led a corporate culling on a global scale, ending relationships with more than half of his retail partners, terminating hundreds of agreements and downsizing sales teams in markets around the world. As Nike directed customers to its own stores and websites, it halted the flow of sneakers to retailers including Amazon, Zappos, Dillard’s and Urban Outfitters, and even curtailed goods at its closest partner in the US, Foot Locker.

Donahoe’s strategy seemed to be working, until it didn’t. That recently abandoned shelf space was quickly filled by all of Nike’s top competitors: Adidas, New Balance, Puma, even Ugg. A flurry of running shoe brands, many of them upstarts such as Brooks, Hoka, On and Salomon, suddenly found themselves with more exposure, and they ate away at Nike’s market share in one of its most important categories. Meanwhile, at the company’s headquarters, the pace of product development slowed as Donahoe took fewer risks on performance-oriented shoe lines across sports. By mid-2023, it was becoming apparent that Dunks and the other reliable lifestyle winners were losing their allure, and Nike had nothing to replace them.

In December the company slashed its revenue forecast and Donahoe shifted into Bain mode, admitting on a conference call with analysts that “we know we must be faster, increasing the pace of innovation.” He unveiled a plan to cut $2 billion in costs, which included getting rid of 2% of the workforce. In interviews with more than 50 current and former Nike corporate employees—including many executives and senior managers who spoke on the condition of anonymity because they still work for Nike or elsewhere in the industry and worry about career repercussions—the moves were characterized as sapping their remaining faith in Donahoe’s regime. “He’s lost the community at Nike,” says Travis Gonzolez, Nike’s former director of client relationship and communication, who was laid off by the company in May.

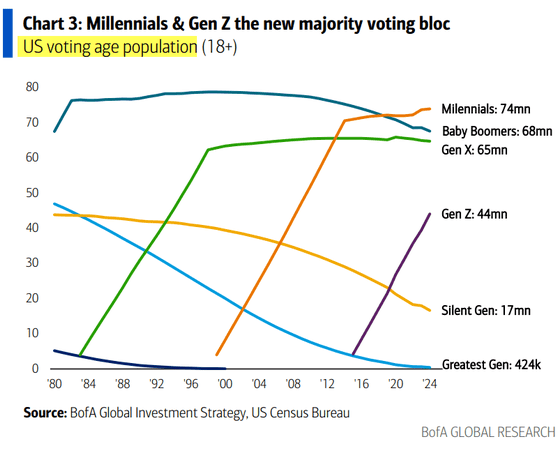

Easy to see why courting pop culture has been a higher priority during this election cycle...

Those born after 1980 will now make up 118 million or 44% of potential voters this November.

(BofA Global Research)

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.