Weekly Research Briefing: Smiley Faces

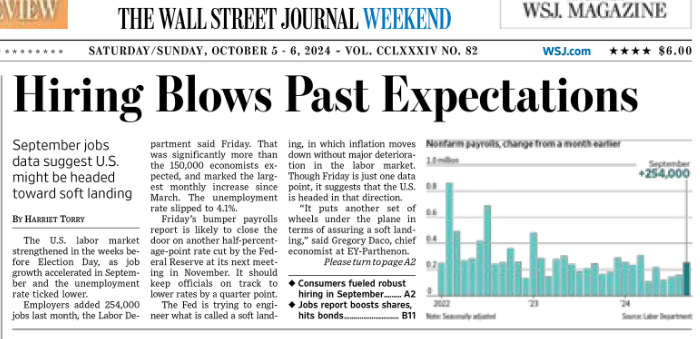

Nothing like a positively surprising set of economic numbers to put everyone in a good mood. The 4.05% unemployment rate combined with a +100k beat in the non-farm payroll figure is going to put the Fed's dour year end jobs projections in jeopardy. Say goodbye to any thoughts of a 50 basis point rate cut in November. It wasn't a perfect report, and it was only one number, but if you are a consumer centric business manager looking toward the holidays, then Friday's report got your attention. Maybe time to find some more inventory and a few more employees to bet on a consumer pickup?

With the consumer responsible for generating two-thirds of the U.S. economy, the stronger than expected jobs data should lift GDP and corporate earnings forecasts. This would be expected to flow through to improved company valuations and higher equity and credit prices. The next potential bump in the road would be if the rebound in economic strength was enough to reverse the downward trend in inflation. This week's CPI & PPI numbers will give us a look at all the new price trends, but for now, wages are continuing to grow faster than the prices of most goods.

Also this week, the third quarter earning season will begin starting with the big financials on Friday. Meetings at Nvidia, AMD and Tesla could also move technology stocks around. And another storm in the Gulf headed for Florida looks certain to disrupt many daily lives once again. Be safe everyone.

The Saturday morning headline that created millions of smiles this weekend...

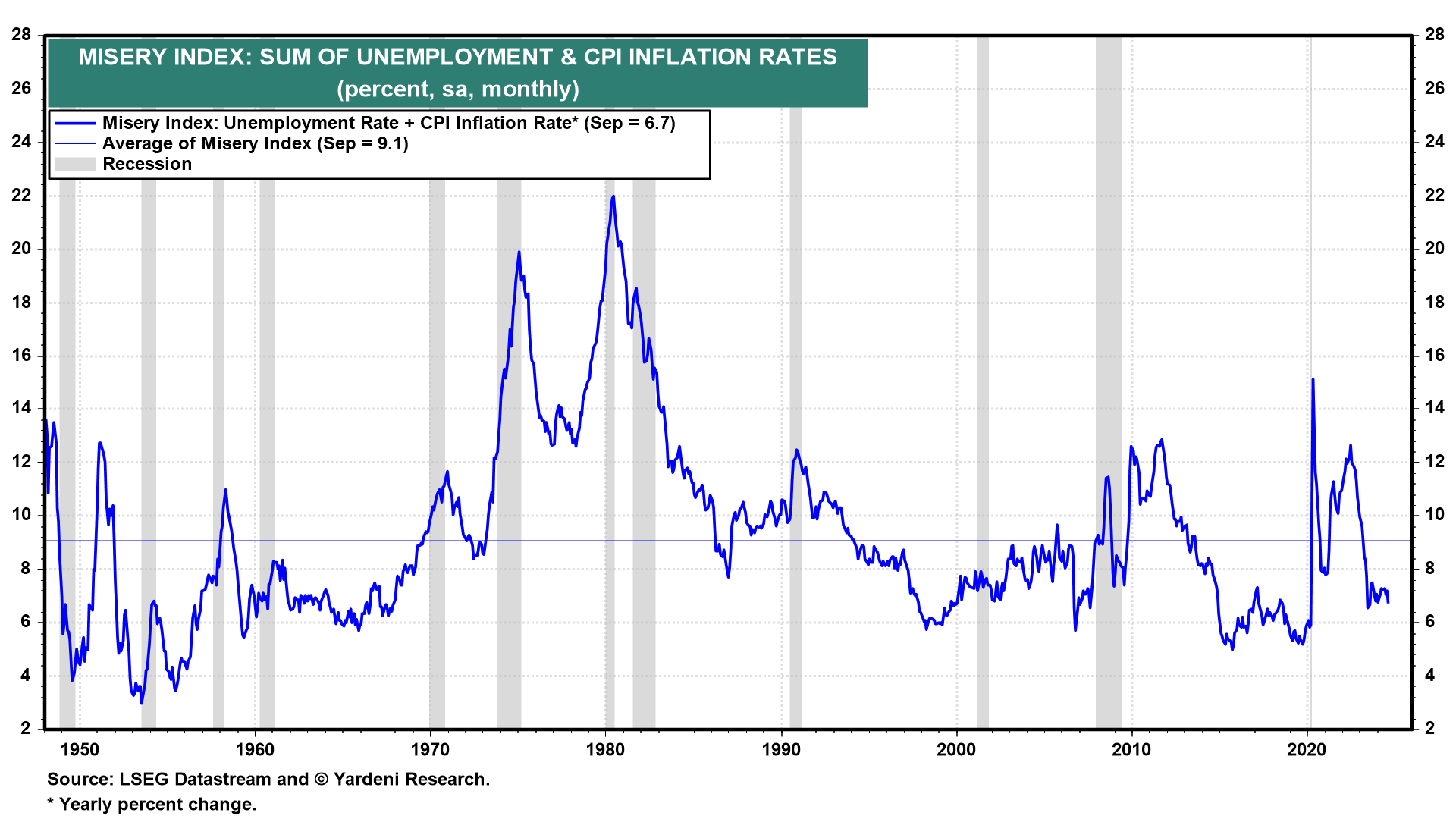

As for the "misery index", there is very little...

@carlquintanilla: JPMORGAN’s David Kelly, on @CNBC: The so-called “misery index” (inflation + unemployment rate) is expected to be ~6.4 points after next week’s #CPI. “That’s lower than it’s been 89% of the time in the last 50 years.”

(Yardeni Research)

Let's not get ahead of ourselves on the September job statistics...

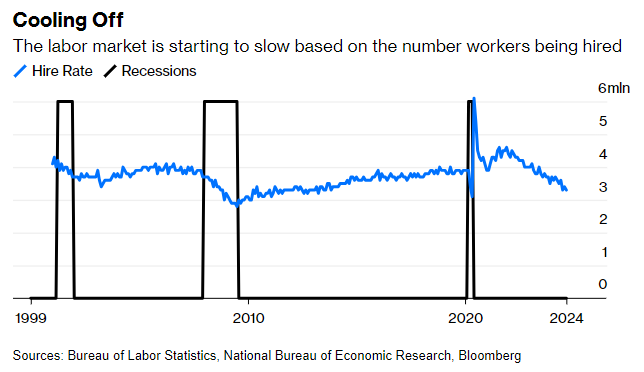

Great news that layoffs are slowing, but we still want to see employers increase their hiring.

The strong gain of 254,000 jobs in September was a welcome surprise after months of cooling in the labor market and reinforced other signs of strength in the US economy. However, one month does not make a trend, and even with the Federal Reserve cutting interest rates, a sustained turnaround in hiring will take time.

In the latest figures from August, the rate of new hires — that is, new workers as a percentage of total employment — fell to 3.3%. This is comparable to what it was in 2013, when the unemployment rate was more than 7% (It is currently 4.1%) Yet, layoffs remain low.

This suggests a cooling but complex labor market: Companies aren’t so worried that they’re letting a lot of people go, but they’re not so confident that they’re hiring a lot of people. This situation is unlikely to change until there is less uncertainty about the economy — and that, in turn, depends on what happens not only with the Federal Reserve and interest rates, but also with the elections next month.

Great news for the credit and lending industry: The 'left' tails are getting cut...

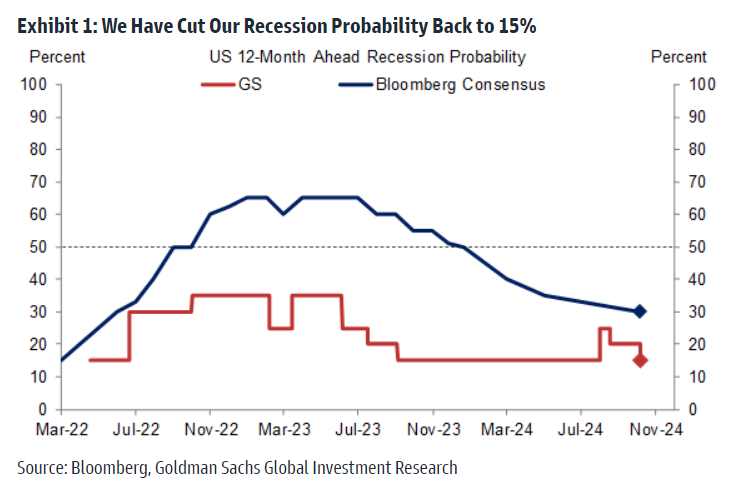

We have cut our 12-month US recession probability back to the unconditional long-term average of 15%, where it stood before the jump in the unemployment rate from 4.054% in June to 4.253% in July. The most important reason is that the unemployment rate fell to 4.051% in September, marginally below both the June level and the threshold that activates the “Sahm rule.” Moreover, with nonfarm payroll growth of 254k surprising sharply to the upside, prior months revised higher, and household employment also solid, we now estimate an underlying jobs trend of 196k, well above our pre-payrolls estimate of 140k and modestly above our estimated “breakeven rate” of 150-180k.

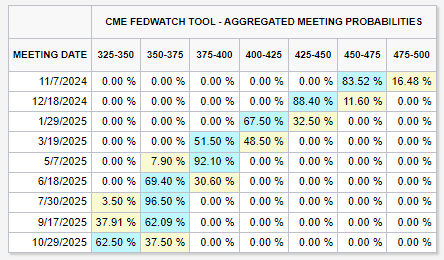

Hope that you are content with only a 25 basis point cut in November...

ISM Manufacturing continued to stink, but the ISM Services figures more than made up for them...

@Trade_The_News: *(US) SEPT ISM SERVICES INDEX: 54.9 V 51.7E;

- Business Activity Index: 59.9 v 53.3 prior

- New Orders Index: 59.4 v 52.5e (increase more than 6ppts m/m)

- Prices Paid: 59.4 v 56.0e

- Backlog of orders 48.3 v 43.7 prior

- Employment: 48.1 v 50.0e

- "Twelve industries reported growth in September, up two from the 10 industries reporting growth in August. The Services PMI® has expanded in 19 of the last 21 months dating back to January 2023, and the September reading is well above its average for 2024."

The Citi Financial Conditions Index has been rising...

Summer economic weakness led to forecasts becoming too conservative. And those new forecasts are now being positively surprised.

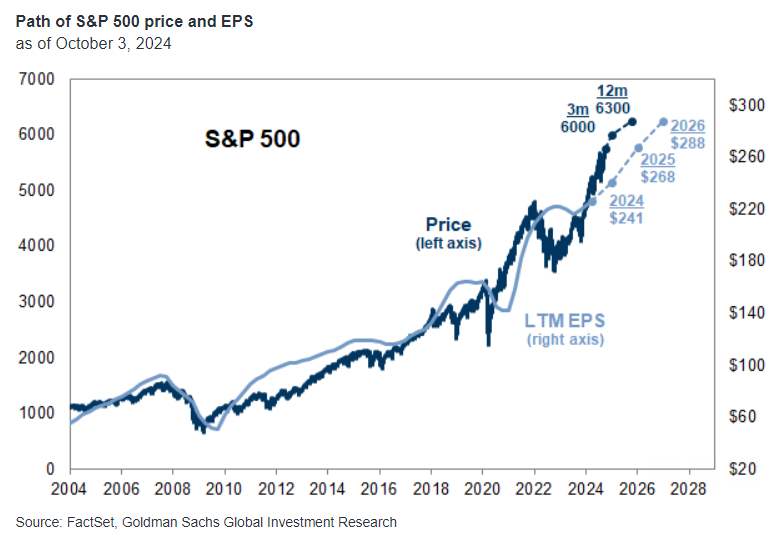

A recovery in the semiconductor cycle plus faster growth in mega-cap tech earnings has pushed Goldman Sachs to raise their 2025/2026 S&P 500 earnings and price targets...

Ahead of 3Q 2024 earnings season, we raise our 2025 S&P 500 EPS forecast to $268 (+11% year/year) from $256 (+6%) and introduce a 2026 EPS estimate of $288 (+7%). We maintain our long-held full-year 2024 EPS forecast of $241 (+8%).

Today’s P/E multiple of 22x is in line with our macro model of fair value. We forecast the P/E will be unchanged at year-end 2024 and lift our index target to 6000 (from 5600) and our 12-month target to 6300 (from 6000), implying 4% and 10% upside, respectively.

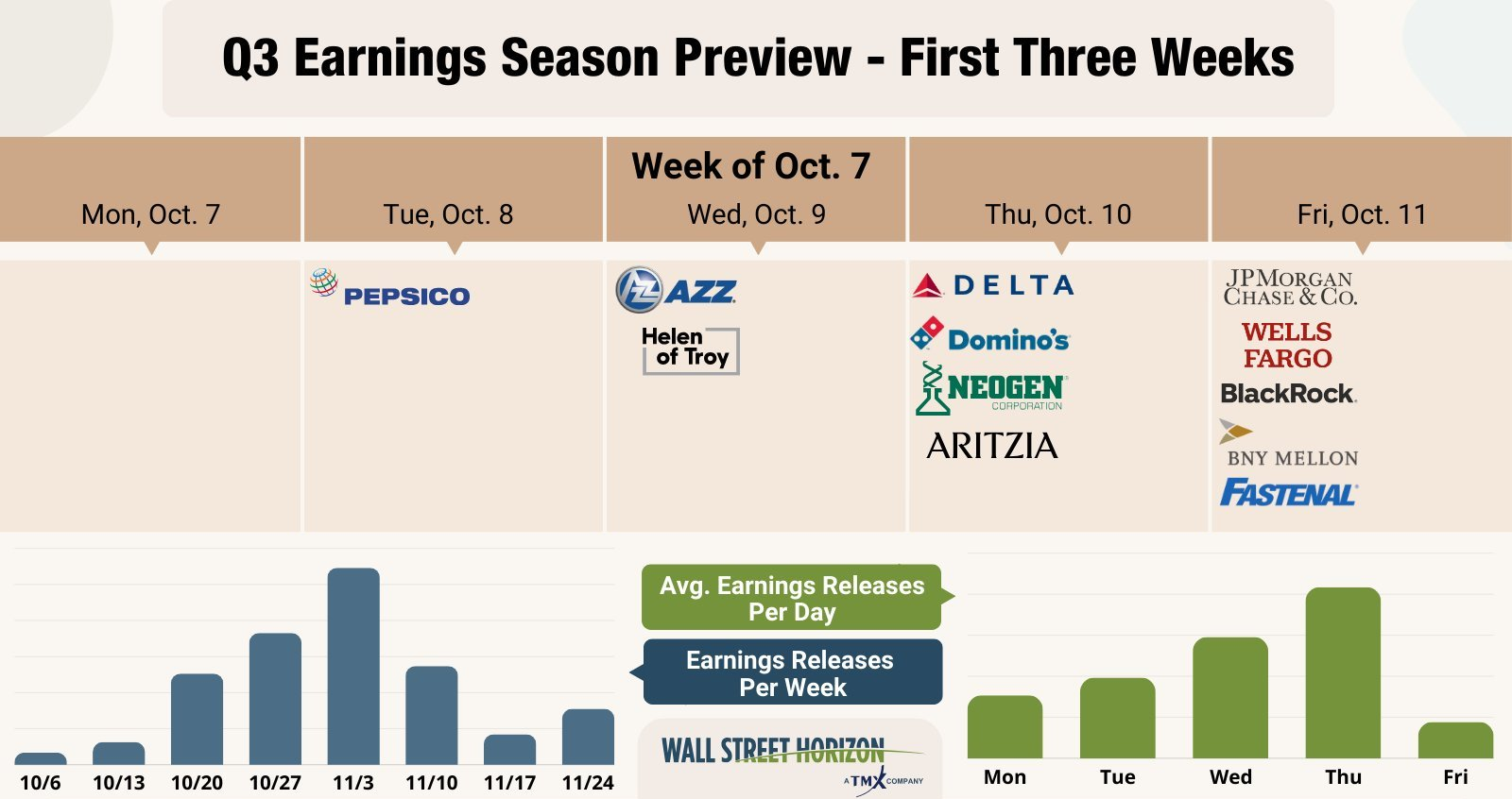

Speaking of earnings, it is now 'go' time...

Q3 numbers begin to flow this week with the big financials dropping on Friday.

(@WallStHorizon)

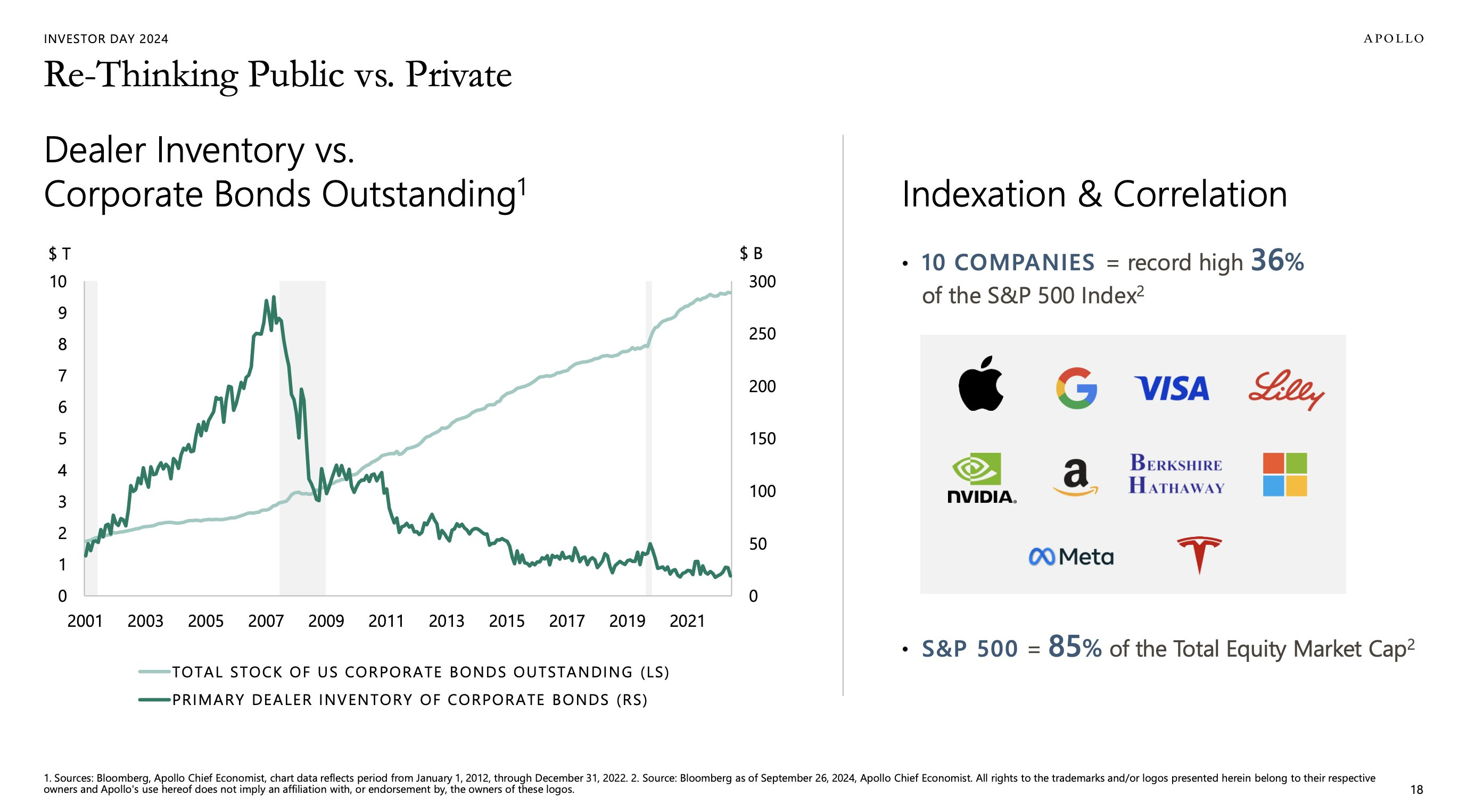

Apollo should not apologize for highlighting the seismic shift that is occurring right now from the public equity to the private equity markets...

Go ask any leader at any investment firm or bank how their investor flows are evolving, and how their client companies are getting access to financing. These leaders know where the world will be in ten years and they are running toward it. The stock price valuations of the private market players versus the mutual fund/ETF players are also telling you where the business is headed.

“I know there's some public equity folks in the room, so I want to be careful not to offend, but most people that we talk to, it's not a hard argument to win when we talk about how the public equity markets are simply put broken, right? You've got almost 60% of public equity markets being indexed. You've seen active management fail to perform over the last 20 years, as Marc said, not because people suddenly didn't get good at their jobs because simply put the structure of markets has changed and made doing that job so fundamentally difficult. But the products haven't changed. The products haven't changed yet everyone that we talk to recognizes a need for retirees, for pensions, for endowments to get diversified equity exposure and they're simply put not getting it. They're investing in 7 companies that are 1/3 of the index, and they're not getting the exposure they want” - Apollo Global Management Co-Head of Private Equity in New York David Sambur

Nir Kaissar's writes in Bloomberg what investors in the private equity markets already know...

- "It’s time to consider the real possibility that the stock market has become a dumping ground for businesses too weak to attract capital in private markets."

- "The challenge for ordinary investors is more immediate: Most of them are confined to the stock market because financial regulation bars them from investing in private markets. Unfortunately, the quality of small public companies — those similar in market value to the businesses that predominate private markets — has deteriorated significantly." what the sellers paid a dozen years earlier, Dougherty’s firm can now charge competitive rents.

- "I also expect that the stay-private trend will accelerate — to the stock market’s detriment and to the growing exclusion of retail investors — unless policymakers intervene. They can start by removing the gates that prevent ordinary investors from participating in private markets."

Are the public equity markets overvalued by 33%, or are the private equity markets undervalued by 50%?

If you need an excellent public vs private market valuation benchmark, you can easily point to the recent StandardAero Inc. IPO. StandardAero is a high- quality aircraft engine maintenance service company with an excellent customer list, highly predictable recurring revenues and solid cash flow generation. It is a perfect private equity company which is why Carlyle/GIC bought it in 2019. Carlyle was looking to sell 20% of it to pay down debt and probably start the monetization process for it's investment to their five year old PE fund holders.

It is well known that Carlyle went thru the due diligence process with many PE firms looking at the asset. With other deals in the industry occurring in the 10-12x EBITDA, it was expected that StandardAero should easily be able to fetch the top side of that range. But rather than take a 12x EBITDA valuation, Carlyle decided to try the public IPO process (which is very desperate for high quality companies).

In the end, the House of Morgan (J.P. & Stanley) was able to find public market investors and the IPO priced at $24 last week. With the stock now trading around $32.50, this puts the public market valuation currently at 17.5x the 2025 PF EBITDA or 45% higher than the 12x that the company was expected to fetch in a competitive private equity sales process.

While there may be reasons to have exposure to the public equity markets, there are few reasons to not have exposure to the private equity market if it is one-third cheaper on an apples to apples basis. Here is the StandardAero Inc. S-1 if you want to run your own set of numbers.

CEOs are hungry to make deals—and there are more to come...

A better economic outlook combined with strong financial markets is injecting M&A confidence into the corner office.

Mergers and acquisitions worldwide are expected to climb 6% this year, on pace to hit almost $3.1 trillion, according to the London Stock Exchange Group. The bump comes after a rough 2023: Deals totaled about $2.9 trillion, nearly half of 2021’s post-pandemic peak of close to $6 trillion...

Companies are putting more money to work and they’ll probably keep buying, based on a forecast for growing earnings in 2025 and projections for more rate cuts this year and next.

“This bodes very well for M&A activity to ramp up again as we head toward year-end and into 2025,” writes Carole Streicher, head of deal advisory and strategy at KPMG U.S.

To that point, hundreds of chief executives want to make buys, a new survey from KPMG shows. Almost nine out of 10 CEOs—88%—said their companies have moderate to high appetites for acquisitions.

And for those CEO's who need M&A financing, the banking markets are sprinting in your direction...

Investment banks, forced to take big writedowns on risky merger and acquisitions loans after a global surge in interest rates, are now jumping back into leveraged buyouts — one of the most lucrative areas in finance.

Traditional lenders and private credit managers are telling private equity firms, known as sponsors, that they can provide more than $15 billion of debt on a single junk-rated deal. That’s about 50% more than last year, according to some market participants, when a number of loans were stuck on lenders’ balance sheets after central banks aggressively hiked rates to tame inflation...

Investment bankers are touting all-in packages of senior loans, bonds and junior debt for deals, people with knowledge of the matter said, asking not to be identified because the discussions are private. The competition is already impacting margins, with senior loans for well-regarded single B rated European companies pricing at about 350 basis points over the benchmark, about 100 basis points lower than last year, the people said.

Lenders can provide leverage “levels of 7.0x and in excess of that, something that wouldn’t have been conceivable 12-18 months ago,” said Roxana Mirica, head of capital markets in Europe at private equity firm Apax Partners LLP. That puts them back at levels that were common before the hung debt saga.

Speaking of deals, the Russell 2000 company Vista Outdoor finally picks not one, but two suitors...

Vista Outdoor on Friday agreed to sell itself in parts to two separate buyers for a total of $3.35 billion, including debt, after fending off a hostile suitor that pursued the sporting goods and ammunitions maker for months. Vista struck a deal to sell its sporting goods unit Revelyst to investment firm Strategic Value Partners for $1.1 billion, according to a statement seen by Reuters. It has also agreed to revise the terms of a previously agreed deal to sell its ammunitions business Kinetic to Prague-based defense contractor Czechoslovak Group (CSG). CSG has raised its offer for Kinetic by $75 million to $2.2 billion. The company, which had initially also agreed to buy a 7.5% stake in Revelyst for $150 million, will no longer do so. Taken together, the two deals value Vista at $45 per share, topping a rival $43 per share offer from MNC Capital, an investment firm led by former Vista board member Mark Gottfredson. MNC has repeatedly attempted to acquire Vista this year.

(Barchart)

And this single stock ticker Russell 2000 company decides to go private after almost forty years in the public markets...

Barnes Group has agreed to be acquired and taken private by Apollo Global Management in an all-cash deal that values the company at $3.6 billion. The industrial- and aerospace-components manufacturer Monday said Apollo would pay $47.50 a share in cash, a 4.9% premium to Friday’s closing price of $45.26... If the deal is completed, Barnes would be delisted from the New York Stock Exchange and become a privately held company that continues to operate under the Barnes Group brand.

(Barchart)

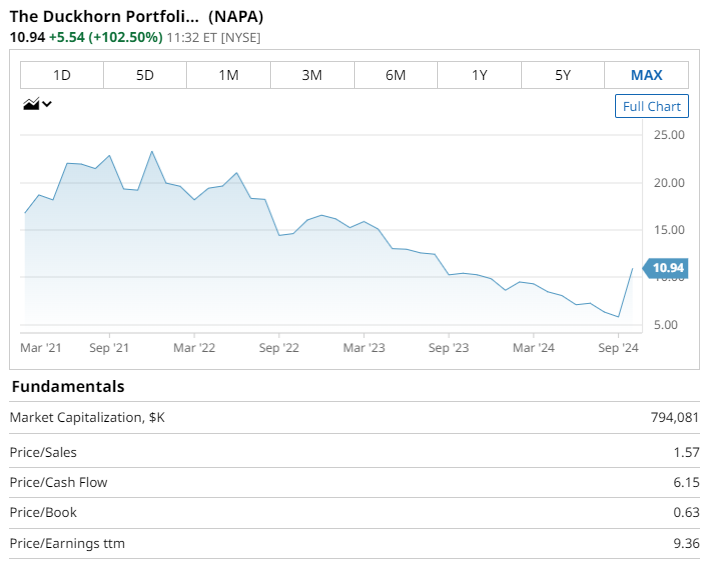

Another Russell 2000 small cap pops the cork on returning to the world of being private...

Duckhorn Portfolio NAPA 103.24% increase; green up pointing triangle has agreed to be taken private by Butterfly Equity in an all-cash deal that values the winemaker at $1.95 billion.

The California-based producer of premium wines said Monday that the private-equity firm has offered to buy the company for $11.10 a share, more than double its $5.40 closing share price last week.

(Barchart)

In the world of activists, Starboard is looking to land a very big fish...

Activist investor Starboard Value has taken a roughly $1 billion stake in Pfizer and wants the struggling drugmaker to make changes to turn its performance around, according to people familiar with the matter.

Pfizer had a market value of about $162 billion as of Friday. Its shares have been roughly cut in half from a record high notched in late 2021 after the company delivered the world’s first Covid-19 vaccine. They are little changed so far this year, compared with a 21% rise in the S&P 500.

Starboard has approached two former Pfizer executives, Ian Read and Frank D’Amelio, to aid in its efforts, and they have expressed interest in helping, the people familiar with the matter said. Read was Pfizer’s chief executive officer from 2010 to 2018 and handpicked current CEO Albert Bourla as his successor. D’Amelio was its chief financial officer from 2007 to 2021.

And Mantle Ridge is going after Air Products which could find plenty of banking and private market financing for this high quality asset...

Activist investor Mantle Ridge has built a more than $1 billion stake in Air Products and plans to push for improvements at the industrial gas manufacturer, according to people familiar with the matter.

Mantle Ridge has been building its position in Air Products since March, the people said.

Air Products, based in Allentown, Pa., had a market value of around $63 billion as of Friday. Its shares are up about 4% so far this year, compared with a 20% rise in the S&P 500.

Mantle Ridge, run by Paul Hilal, plans to push Air Products executives on succession planning for Chief Executive Seifi Ghasemi as well as on improvements to the company’s strategy and capital allocation, the people said. The firm believes Air Products is trading at a discount to its peers, they added.

There has been a record surge in new business formation since 2020...

Mr. Xu, 30, is part of what may be one of the pandemic’s most unexpected economic legacies: an entrepreneurial boom. Stuck at home with time — and, in many cases, cash — to burn, Americans started businesses at the fastest rate in decades.

What happened next might be even less expected: Those businesses thrived, overcoming supply chain disruptions, labor shortages, rapid inflation and the highest interest rates in decades.

Businesses formed from 2020 to 2022 had created 7.4 million jobs by the end of 2022, according to data released by the Census Bureau last month, contributing to the strong rebound in the broader labor market. More timely but less comprehensive data suggests that these businesses have continued to add jobs in the past two years.

That resilience, combined with the high rate of start-up activity even after the pandemic ended, has made researchers increasingly optimistic that the U.S. economy might be emerging from what had been a decades-long entrepreneurial slump. If they are right, it could have lasting implications: Historically, new businesses have played a crucial role not just in job growth but also in innovation, making the economy more productive and adaptable...

New data from the Census Bureau shows that the businesses created in 2020 were smaller on average than those created in the years before the pandemic. But there were far more of them, and they grew as fast as their pre-Covid counterparts, if not faster.

In a brief research note last month, Mr. Haltiwanger, the University of Maryland economist, and a co-author wrote that the new data provided “overwhelming evidence that the pandemic and its aftermath featured a surge in genuine entrepreneurial employer business creation.”

Data from Gusto, which handles payroll and related needs for small businesses, tells a similar story. Economists there found that businesses created during the pandemic era were roughly as likely to experience rapid growth as those founded before the pandemic. And those “high-growth” businesses grew even faster than their prepandemic peers, resulting in hundreds of thousands of additional jobs.

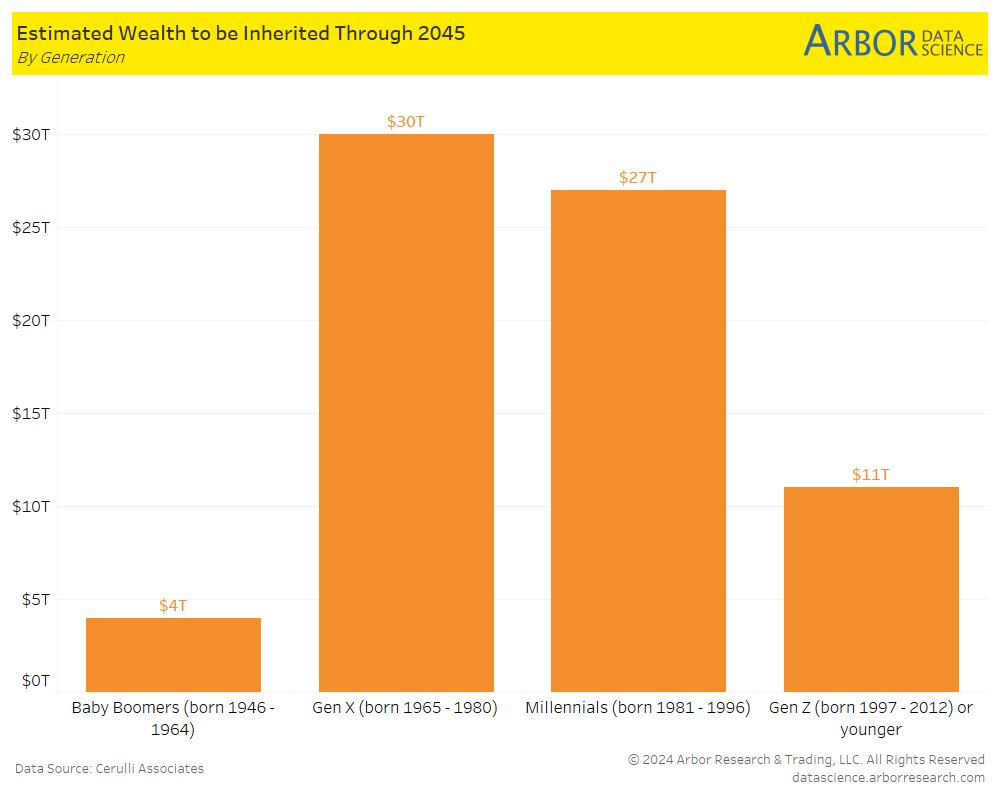

That is a very big number...

Cerulli Associates calculates $84 trillion moving to younger generations over the next 20 years...

(@DataArbor)

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: Costco Wholesale Corp.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.