Weekly Research Briefing: Time to Cast

For economists, mid-August is a time to trade the wingtips for waders and a fishing pole because the Wyoming trout have been gorging all summer and are ready to play. They don't care about the carry trade in Japan or an inflation reading out to three significant digits. That is food on the hook for the rest of us. But not for the trout. It only wants that one perfect fly.

In between river wading sessions, there will be discussion groups and papers presented while all FOMC members take turns visiting TV cameras for their Fed-speak. The big event will be Friday when Fed Chair Powell takes the mic which the investing world will filter through every word looking for future rate cut clues. Last week's CPI report seemed to have given the Fed even more room to work with. Both of the headline and core CPI figures nearly rounded down which could have sent the markets into a feeding frenzy. Even under the hood, the shelter component amounted to almost 90% of the month over month. In other words, ex-housing costs, there is no inflation.

So good news was good news as inflation arrived weaker while retail sales and jobless claims showed up better than we thought. The markets continued their ascent as investors re-risked their portfolios and corporations re-engaged their quarterly stock repurchases. The markets continued to broaden out as shown by both the S&P 500 equal-weight index and Berkshire Hathaway moving up to all-time highs. And after ringing the mid 60's two weeks ago, the VIX has retreated to below 15. Looks like the credit markets were again correct.

A bit of a slow week with only retailer earnings, jobless claims and Jackson Hole in the spotlight. Hope that you find something more important to do than watch the tape. Have a great week.

Friday's jobs data gave the Fed all the ammo they need for a cut in rates...

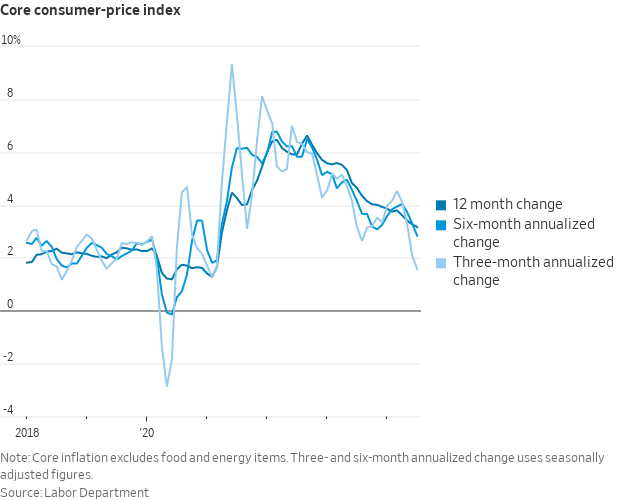

The July Core CPI came in at +0.17% MoM, a better than expected versus consensus of +0.19% MoM. This is now the 4th consecutive “soft” inflation report and solidifies the case for the Fed to start a rate cutting cycle starting in Sept.

The details of this report were very good:

– Core CPI MoM +0.17% (YoY fell to +3.17% vs +3.27% last month)

– the two largest contributors to inflation

– Shelter ex-hotels +0.17% CTG

– Auto insurance +0.04% CTG

– Ex-these two, Core CPI would be -0.04% MoM

The rolling 3/6/12 month change chart better shows the visual collapse in core consumer prices...

Rate cuts are coming...

@NickTimiraos: What the July CPI means for the Fed:

• The July CPI extends a run of much cooler inflation and makes a September rate cut from the Fed as close to a lock as these things get.

• This report makes it easier at the margin to avoid dissents on the first cut.

• This report doesn't resolve the debate over whether to start with 25 bps vs 50 bps. To get 50 bps, you'd probably need to see something bad in the labor market.

• A big question for the September FOMC will be how many rate cuts are penciled in for the rest of the year. (Remember, the September SEP is unusual. Because the SEP is calendar-based, it's basically guiding on the path of policy at the Nov+Dec meetings.) Mild inflation readings could make a three-cut baseline more likely

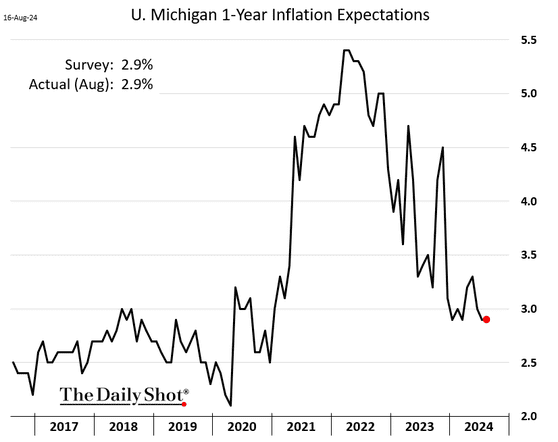

Even consumer's inflation expectations fell to lows on Friday...

So maybe all political candidates can stop looking at issues in the rear view mirror and focus on the future instead? No more talk about Tic-Tacs or price controls at grocery stores. Let's fast-forward to hearing exactly how your party will create more jobs than the other party.

Important comments from Walmart and The Home Depot earnings last week give good insight into the current consumer mind...

"We did not see a step down and our outlook for the back half of the year is really for more of a continuation of what we've seen. Even in the first couple weeks of August here, things have been remarkably consistent. So I know everyone is looking for some piece of information that maybe indicates further weakness with our members and our customers, we're not seeing it...So far, we aren't experiencing a weaker consumer overall” — Walmart CFO John D. Rainey

"During the quarter, higher interest rates and greater macroeconomic uncertainty pressured consumer demand more broadly, resulting in weaker spend across home improvement projects...When we look at the performance in the first six months of the year, as well as continued uncertainty around underlying consumer demand, we believe a more cautious sales outlook is warranted for the year...we are now guiding to a comp sales decline of approximately 3% to 4% for fiscal 2024." — The Home Depot CEO Ted Decker

Speaking of consumers, the Consumer Staples index remains one of the best looking charts in the market right now...

Even with all the political inflation bashing, the manufacturers of our daily products and their retailers are breaking out to all-time highs. Thank you, Walmart.

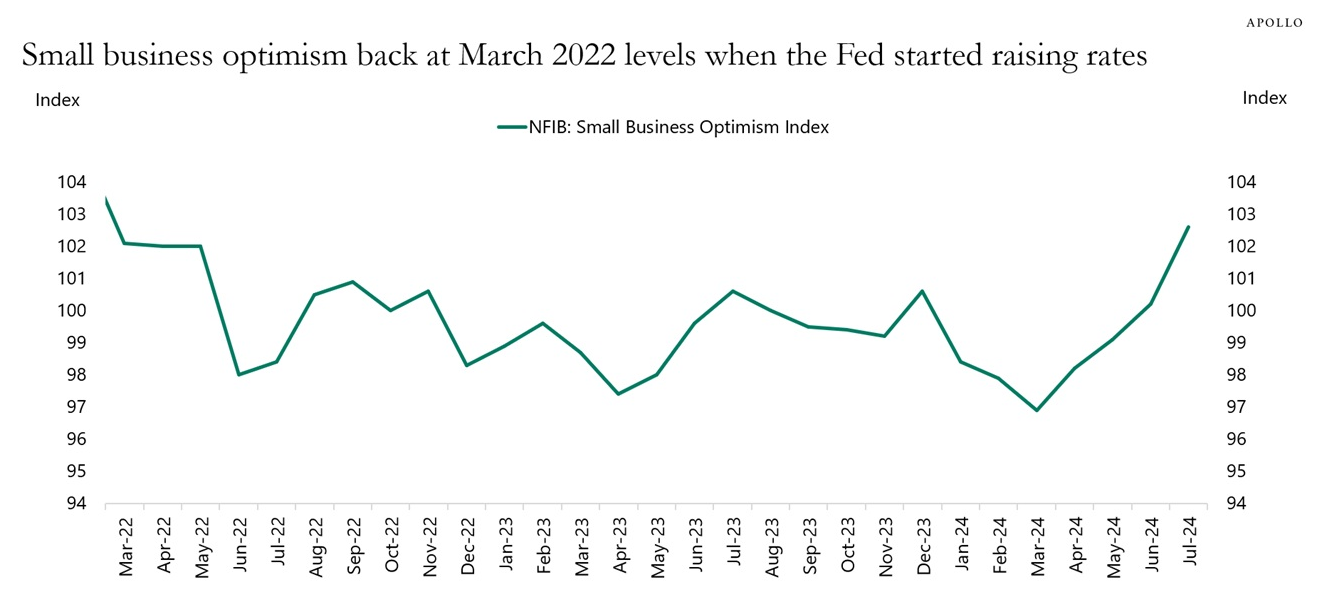

So now small business optimism is finally breaking higher...

Small business optimism is at the same level as when the Fed started raising interest rates in March 2022, see chart below. This is not a recession. If anything, this suggests the economy is reaccelerating.

With last week's CPI data, the Fed seems aligned toward future easing...

Mary Daly, president of the San Francisco Fed, told the Financial Times that recent economic data have given her “more confidence” that inflation is under control. It is time to consider adjusting borrowing costs from their current range of 5.25 per cent to 5.5 per cent, she said.

Her call for a “prudent” approach pushed back on economists’ concerns that the world’s largest economy is heading for a sharp slowdown that warrants rapid cuts in interest rates...

Daly, who votes on the Federal Open Market Committee, played down the need for a dramatic response to signs of a weakening labour market, saying the US economy was showing little evidence of heading for a deep downturn. The economy was “not in an urgent place”, she said.

“Gradualism is not weak, it’s not slow, it’s not behind, it’s just prudent,” she said, adding the that labour market — while slowing — was “not weak”.

Even the hawkish Fed's Bostic is now open to a September cut after the CPI report confirmed weakening inflation...

"I’m open to something happening in terms of us moving before the fourth quarter...Now that inflation is coming into range, we have to look at the other side of the mandate, and there, we’ve seen the unemployment rate rise considerably off of its lows...We’ve been saying for a long time that we want to see the numbers come in to give us more confidence that we’re sustainably on the path to 2 percent and I have to say, the numbers that have come in in the last several months have given me greater confidence that we’re sustainably on that path." — Atlanta Fed President Raphael Bostic

The newest Fed member is on board with easier monetary policy...

@NickTimiraos: St. Louis Fed President Alberto Musalem becomes the latest Fed speaker to signal he can support a rate cut.

Key points from his remarks on Thursday morning:

• The U.S. labor market "is no longer overheated"

• The labor markets "no longer pose a clear upside risk to inflation"

• Recent data has bolstered my confidence that inflation will return to target

• Absent new shocks, risks of inflation rising has declined, while risks to unemployment to increase

• "The time may be nearing when an adjustment to policy may be appropriate"

Neel Kashkari doesn't have a vote this year at the FOMC but he still has an influential voice...

“The balance of risks has shifted, so the debate about potentially cutting rates in September is an appropriate one to have,” Kashkari said in an interview.

In June, Kashkari had said he thought a rate cut might not be warranted until the end of the year. But the rise in the unemployment rate, to 4.3% in July from 3.7% at the start of the year, points to greater risks of an undesirable slowdown.

“If we were not seeing evidence that the labor market was weakening, if the unemployment rate was still in the 3.7% to 3.8% range, I don’t think I would be even debating, ‘Hey, is now the time to cut rates?’” said Kashkari. Instead, he said, the conversation has shifted because “inflation is making progress and the labor market is showing some concerning signs.”

If you are looking for confirmation that U.S. interest rates are headed lower, just look to the growing weakness in the U.S. Dollar index which traded below 102 today...

@KevRGordon

Goldman Sachs takes back 1/2 of its recession bet increase from 2 weeks ago...

There’s now just a 20% chance that the U.S. suffers a recession over the next 12 months, according to Goldman Sachs.

“The data released since Aug. 2—including retail sales and jobless claims this week—shows no sign of recession,” a team of economists led by Jan Hatzius said in a note to clients on Saturday. Figures published on Thursday showed that spending rose at a faster clip than expected last month and that the number of people filing for unemployment insurance fell from the previous week.

Goldman raised its recession probability to 25% earlier this month, citing weaker-than-expected July jobs numbers. Before that, the economists had been pegging the chances of an economic slump at 15% for nearly a year.

Hatzius and Co. said they’d probably cut their odds back down to 15% if the August jobs report, set to be published on Sept. 6, “looks reasonably good.”

Barrons

Difficult to dial up any recession odds with high yield bonds continuing to move to new highs...

Stockcharts

In fact, S&P Global is considering dialing down its default rate expectations for 2025...

@carlquintanilla: S&P: "The Speculative-Grade Corporate Default Rate In The U.S. Could Fall To 3.75% By June 2025." Our report "identifies several factors 3that we expect will contribute to a lower default rate for these issuers: strong refinancing and repricing activity, resilient earnings, and resilient consumer spending." (@SPGlobalRatings)

As S&P Global noted, weak companies have more options to fix their balance sheets and survive when yields are the lowest in two years...

@lisaabramowicz1: Yields on US junk bonds have fallen to the lowest in more than two years.

Say goodbye to a single letter ticker S&P 500 component as summer M&A activity grows...

Privately held Mars Inc. is going to grab a very big basket of snacks via one of the biggest M&A deals of 2024. Not a lot of overlap in the snack items and this will help Mars move away from its chocolate concentration. Price is mid-teens times EBITDA before any synergies. The big unknown is how big the GLP-1 speedbump ahead is.

Mars unveiled a nearly $30 billion deal for foodmaker Kellanova on Wednesday, a sign that big food companies are willing to pay up to increase their snacking portfolios.

The privately held Mars said it has agreed to pay $83.50 a share for Kellanova in the all-cash deal, confirming an earlier report from The Wall Street Journal.

Kellanova shares closed on Tuesday at $74.50 and had been trading in the high $50s before the company reported better-than-expected earnings and news of the deal talks surfaced earlier this month...

Acquiring Kellanova would push Mars, known for M&M’s and Skittles, into supermarkets’ chips and crackers aisles, giving it a bigger share of the snacking pie when consumers are eating fewer sit-down meals and more snacks throughout the day.

AMD will spend $5 billion in cash and stock to acquire privately held ZT Systems...

Advanced Micro Devices agreed to pay nearly $5 billion to buy ZT Systems, a designer of data-center equipment for cloud computing and artificial intelligence, bolstering the chip maker’s attack on dominance in AI computation.

The deal, among AMD’s largest, is part of a push to offer a broader menu of chips, software and system designs to big data-center customers such as Microsoft and Facebook owner Meta Platforms, promising better performance through tight linkages between those products.

Secaucus, N.J.-based ZT Systems, which isn’t publicly traded, was founded in 1994. It designs and makes servers, server racks and other infrastructure that house and connect chips in the giant data centers that power artificial-intelligence systems such as ChatGPT.

$11.5 billion market cap food service company expands in the southeast with a $2 billion cash deal...

Performance Food Group Company said on Wednesday it would acquire privately held foodservice distributor Cheney Bros for $2.1 billion in cash, bolstering its presence in Southeastern U.S. Florida-based Cheney, owned by the Cheney family and private equity firm Clayton Dubilier & Rice (CD&R), generates annual sales of more than $3 billion. The move will help Performance Food expand into states such as Florida, Georgia, North Carolina and South Carolina.

Baxter continues to move the puzzle pieces around by selling Vantive into the private market...

Buyout firm Carlyle Group struck a deal to acquire Baxter’s kidney-care unit Vantive for $3.8 billion, the companies said on Tuesday. The proceeds from the deal, which is expected to close by early 2025, will help medical-device maker Baxter reduce its debt pile. Baxter, which paid down about $2.8 billion of debt last year after divesting its biopharma unit, had long-term debt of $13.8 billion at the end of 2023. In 2022, Baxter started exploring options for its kidney-care units after completing its $10.5-billion takeover of medical-equipment maker Hill-Rom. It began the process of carving out Vantive early in 2023.

Leading HVAC company Carrier also moves a puzzle piece into the private market...

Carrier to sell Commercial & Residential Fire unit to Lone Star Funds for $3B; Expects to redeploy the estimated $2.2B in net proceeds from the transaction towards share repurchases. Entered into a definitive agreement today to sell its Commercial and Residential Fire business to an affiliate of Lone Star Funds for an enterprise value of $3B. As a result of significant de-leveraging this year, and consistent with prior messaging, Carrier expects to redeploy the estimated $2.2B in net proceeds from the transaction towards share repurchases.

TradeTheNews

And a large Japanese Insurer adds to its U.S. holdings with a $2 billion deal...

Japan's Meiji Yasuda Life Insurance will acquire American Heritage Life Insurance for roughly $2 billion, Nikkei has learned, looking to expand the group policy business in the growing U.S. market.

Meiji Yasuda will buy all American Heritage shares from parent Allstate, the U.S. insurance heavyweight. The transaction will be done through Meiji Yasuda's U.S. subsidiary StanCorp Financial Group...

American Heritage, headquartered in the state of Florida, is a midsize life insurance provider that specializes in voluntary employee group policies. For 2023, the company took in about $1 billion in insurance premiums, and the pretax profit that year was approximately $120 million.

$50b market cap Roper Tech spends $1.5 billion to add ID software and hardware into its mix...

Roper to acquire campus technology and payment solutions co Transact Campus for $1.5B; expects acq to deliver long-term high single-digit organic revenue growth (update) - ROP entered into a definitive agreement to acquire Transact Campus, Inc. (“Transact”) for a net purchase price of $1.5 billion, including a $100 million tax benefit resulting from the transaction. The net purchase price represents approximately 14 times expected 2025 EBITDA. Transact is an award-winning provider of innovative campus technology and payment solutions, offering a comprehensive suite of services, including campus ID software and secure access, tuition and fees software and payment processing, as well as point-of-sale campus commerce solutions.

TradeTheNews

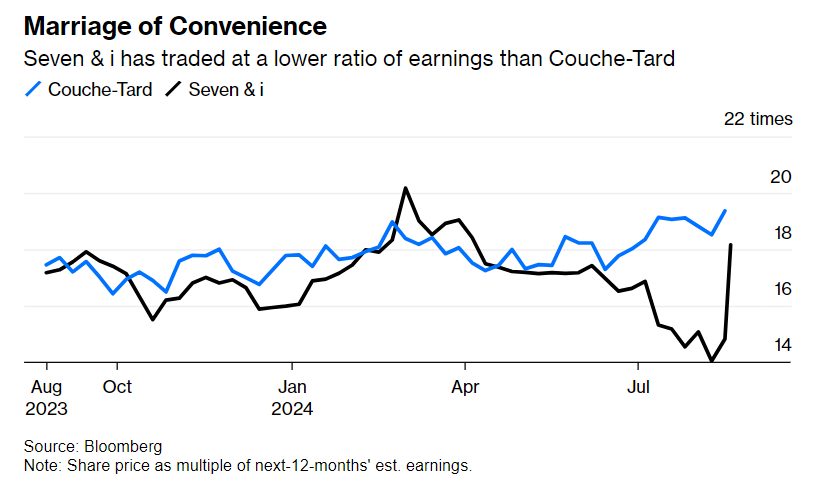

The 7-Eleven plus Circle-K deal could make for the largest Japanese acquisition ever...

Barely weeks after the Japanese stock market’s stunning roller-coaster ride, here comes a hugely ambitious takeover approach for a target whose defenses were already weak — iconic convenience store operator Seven & i Holdings Co.

Suitor Alimentation Couche-Tard Inc. is clearly being opportunistic here. But at the same time, the Canadian bidder is spying an acquisition that’s more logical than its failed tilt at France’s Carrefour SA three years ago.

Couche-Tard, operator of Circle K, has transparent ambitions to grow in leaps and expand its international reach. That makes sense. Retail is a scale game. With size comes greater buying power with global suppliers. A purchase of Seven & i, owner of 7-Eleven, would bring some eastern geographical diversification too.

Such a deal won’t come easily by any means. Seven & i’s market capitalization was 4.6 trillion yen ($31 billion) on Friday, the last trading day before bid interest became public. Add a standard 30% takeover premium and assumed net debt and the total capital outlay would be closer to $60 billion. Apply a peer group valuation multiple to forecast profit and Seven & i would be worth $86 billion, says Bloomberg Intelligence.

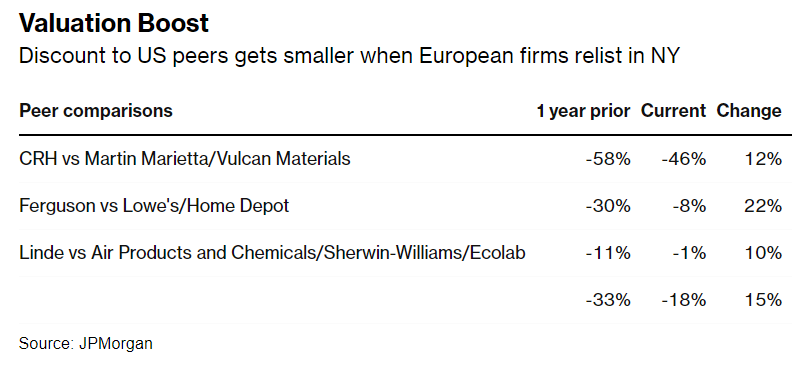

Same company, different exchange, better multiple...

Pfffst. Want a higher valuation? Ditch your Euro stock exchange for a U.S. one and you will have lines of passive investors waiting to buy your stock. Efficient markets are for losers.

European companies that relist in New York tend to see improved valuations, in part due to the prevalence of passive investing in the US, according to an analysis by JPMorgan Chase & Co.

Building materials firm CRH Plc, infrastructure company Ferguson Enterprises Inc. and industrial gas firm Linde Plc have seen their discount to US rivals narrow by 15%, on average, since one year before completing their listing changes, the bank said in a note to clients.

“Commonly cited reasons for international companies choosing to list in the US include the benefit from greater market depth, and a broader investor base,” said the team led by Mislav Matejka. “Another advantage is that US companies enjoy a higher level of passive investment capital due to the popularity of ETFs and index funds,” they wrote.

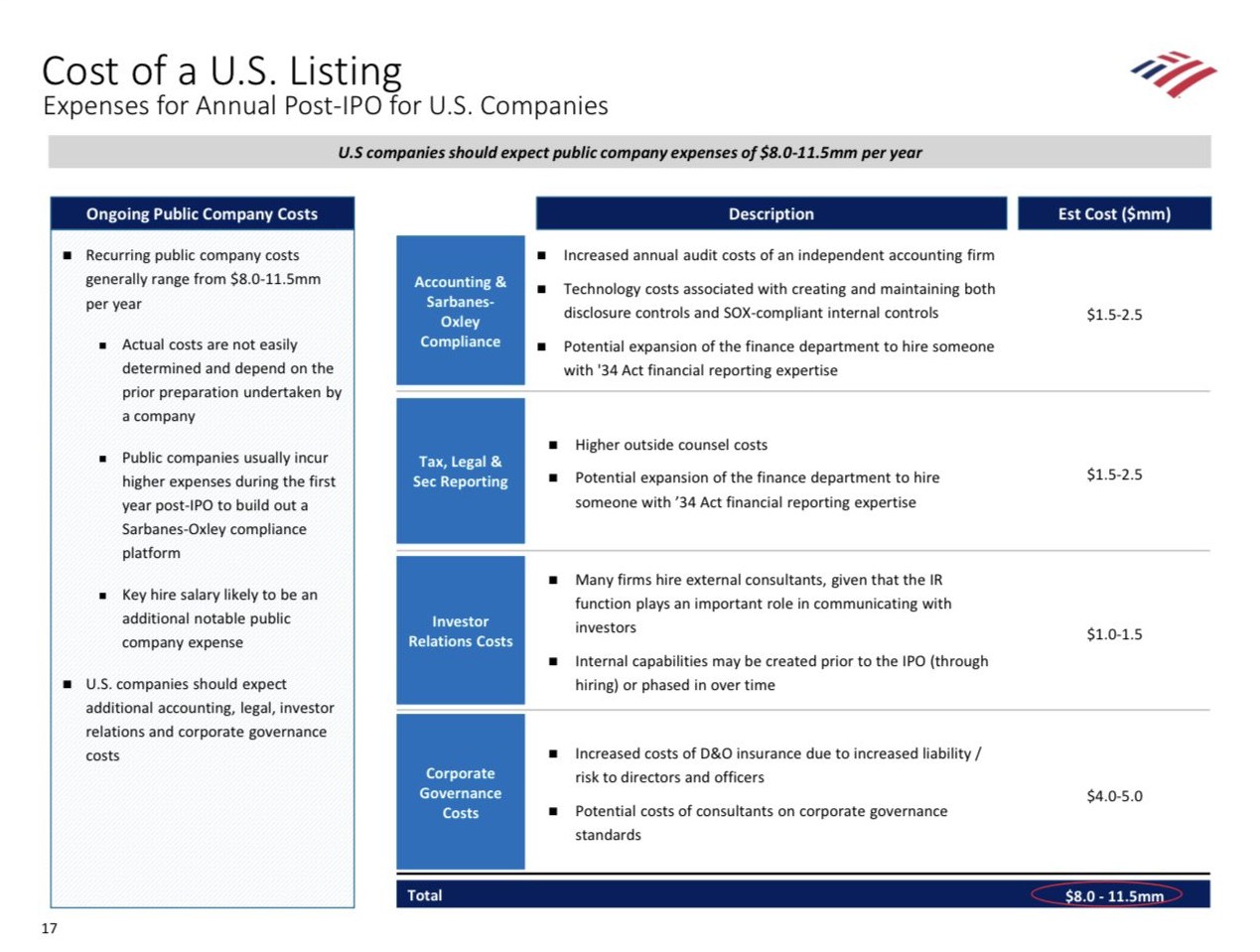

BofA sees public companies spending $8 to $11.5 million per year by going public...

And this is just for a small company. Think of how much Kellanova will save by ending many functions as it folds into Mars Inc. But besides the dollars in savings, there are enormous time savings for the CEO, CFO and many other members of the executive team dealing with investors focused on a daily moving stock price.

@jrichlive

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: Home Depot Inc. and Advanced Micro Devices Inc.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.