Weekly Research Briefing: The Road Converges

The fork in the road ends this week. After Tuesday, Americans will have selected their future government and the elected politicians will need to find ways to work together to make things better for its citizens. ANY certainty after the election will be a good thing as consumers, business owners and investors will be able to adjust planning for their futures. It is time for "election uncertainty" to disappear from all the business surveys. There are no more excuses. Business managers will need to refocus on work and find ways to outperform their competition or lose to them. Corner offices waiting to make that M&A offer or IPO filing can now hit the send button. (Qualcomm, you can start us off.) And investors wanting a look at the results can now trade on those portfolio adjustments. Time to upshift on the road ahead.

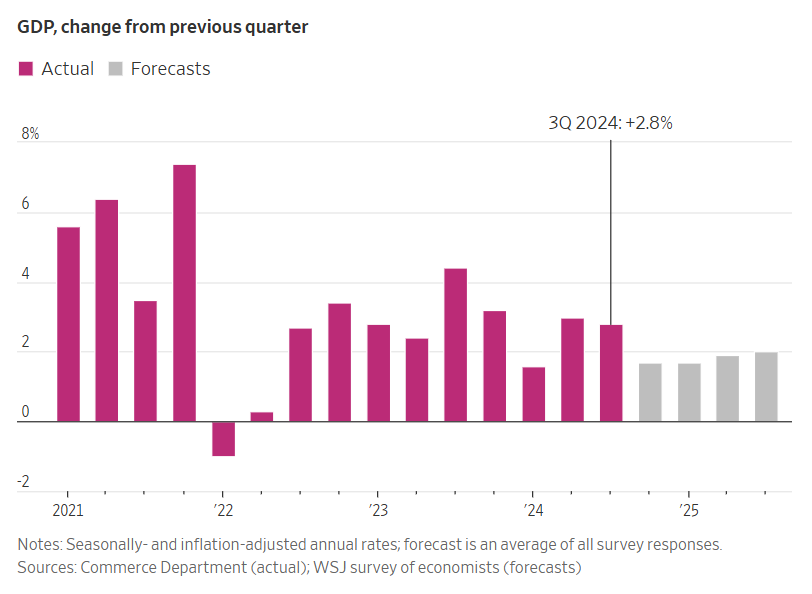

Last week was a busy one with almost half of the S&P 500 reporting. Pluses and minuses across the board, and among the giants, Amazon and Alphabet delivered while Apple and Microsoft disappointed. Cloud and AI remained a focus area for all once again this quarter as data center growth and spending continued higher. Another highlight was the U.S. GDP result for the Q3 which rose +2.8% behind strong consumer consumption and capex spending. Not a highlight was Friday's jobs data which was wrecked by the hurricanes and the ongoing Boeing strike. The +12,000 non-farm payroll addition for October was likely not reflective of the actual economy but it will take another month or two of data to determine the storm's full impact.

This week the Fed will hold its November FOMC meeting later than usual to miss the election date. Thursday's summary should include another 25 basis point cut in the Fed Funds rate reflecting the continued decline in inflation combined with a desire to be ahead of the slowing jobs picture. This has been well telegraphed by FOMC members in recent weeks. The focus will be on any indication of what the December meeting will bring and what indicators the Fed is most focused on. With almost three-quarters of the S&P 500 earnings reports on the tape for this Q3, the mic will be handed to the small and mid-caps to record their earnings this week. Still plenty of good data to be mined to help us with our investment portfolio mosaic. Enjoy the week, Tuesday's election results, and an end to political advertising for this cycle!

No matter what happens on Tuesday, remember that the U.S. economy is bigger than any single elected official...

With another solid performance in the third quarter, the U.S. has grown 2.7% over the past year. It is outrunning every other major developed economy, not to mention its own historical growth rate.

More impressive than the rate of growth is its quality. This growth didn’t come solely from using up finite supplies of labor and other resources, which could fuel inflation. Instead, it came from making people and businesses more productive...

Most leaders from around the world would trade their economies for the U.S.’s in a heartbeat. Through the second quarter, the U.S. grew 3%; none of the world’s next six largest advanced economies grew more than 1%. Even China is struggling.

Sometimes strong growth is a prelude to a recession because it comes from straining the economy’s capacity, generating inflation and forcing the Federal Reserve to raise rates.

Yet inflation has fallen in the past year, to 2.7% in the third quarter, using the Fed’s preferred underlying measure. That’s still above the Fed’s 2% target, but the progress was sufficient for the Fed to cut rates in September and pencil in more cuts—all without growth flagging.

“That’s pretty impressive. That’s a bit of a Goldilocks outcome,” Robin Vince, chief executive of BNY, said in a recent interview. “A year, two years ago, very few commentators actually thought that was going to be possible.”

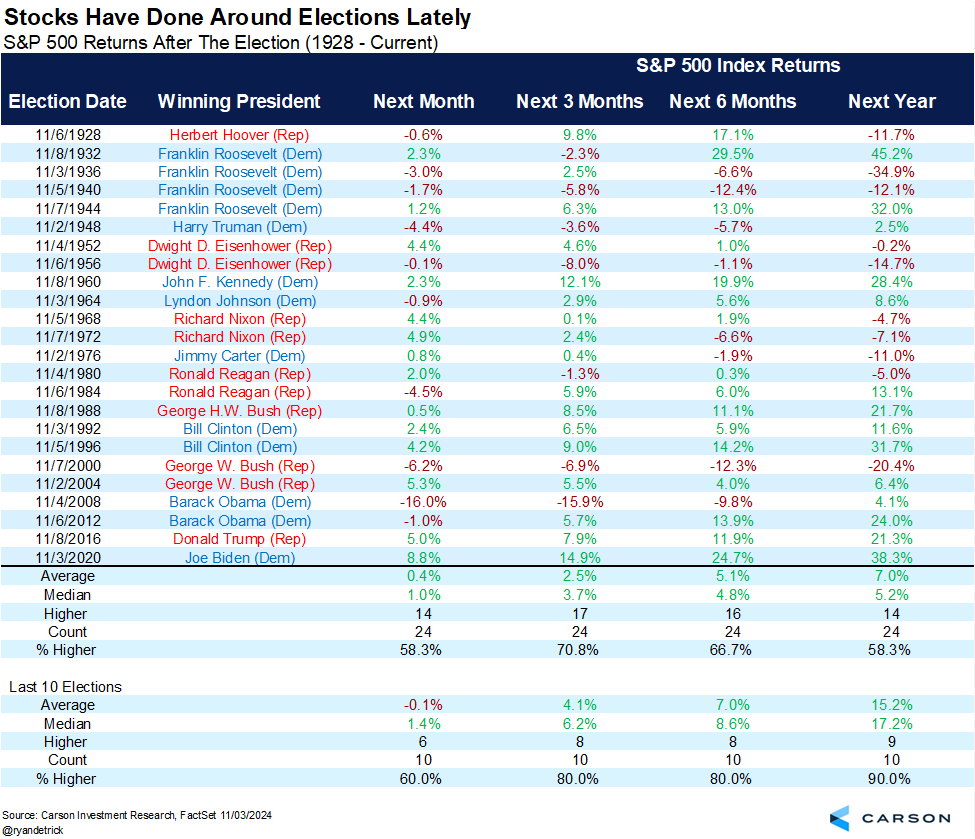

Elections come and go, but the stock market tends to keep marching higher...

@RyanDetrick: Here's how stocks have done after the past 24 elections. What really stands out is how well stocks have done after the 10 most recent elections. Higher a year later 9 times and up 15.2% on avg (median of 17.2%).

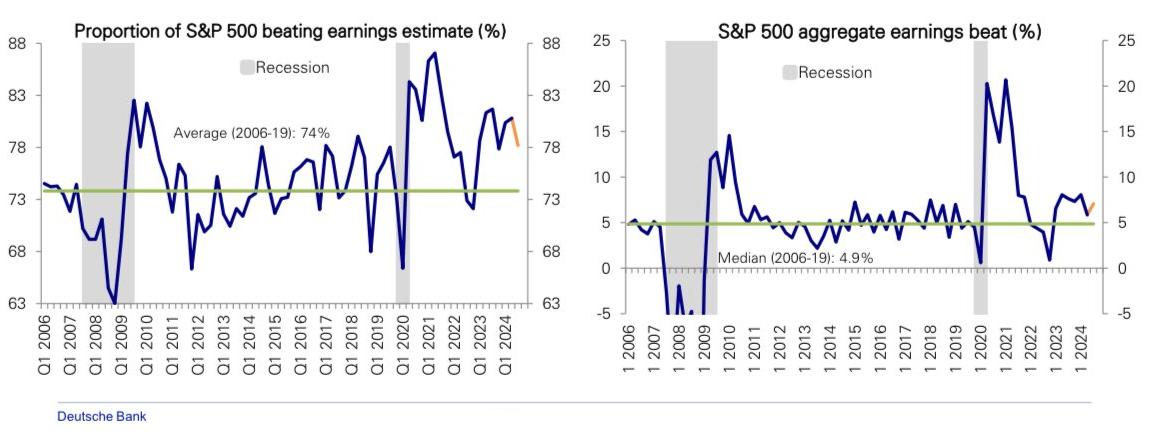

The Q3 reporting season continues to evolve in a positive direction...

@carlquintanilla: DEUTSCHE: “.. Earnings beats running well above average. 78% of S&P 500 companies have beat on earnings, by an aggregate 7.1%, well above the historical average of 4.9%.”

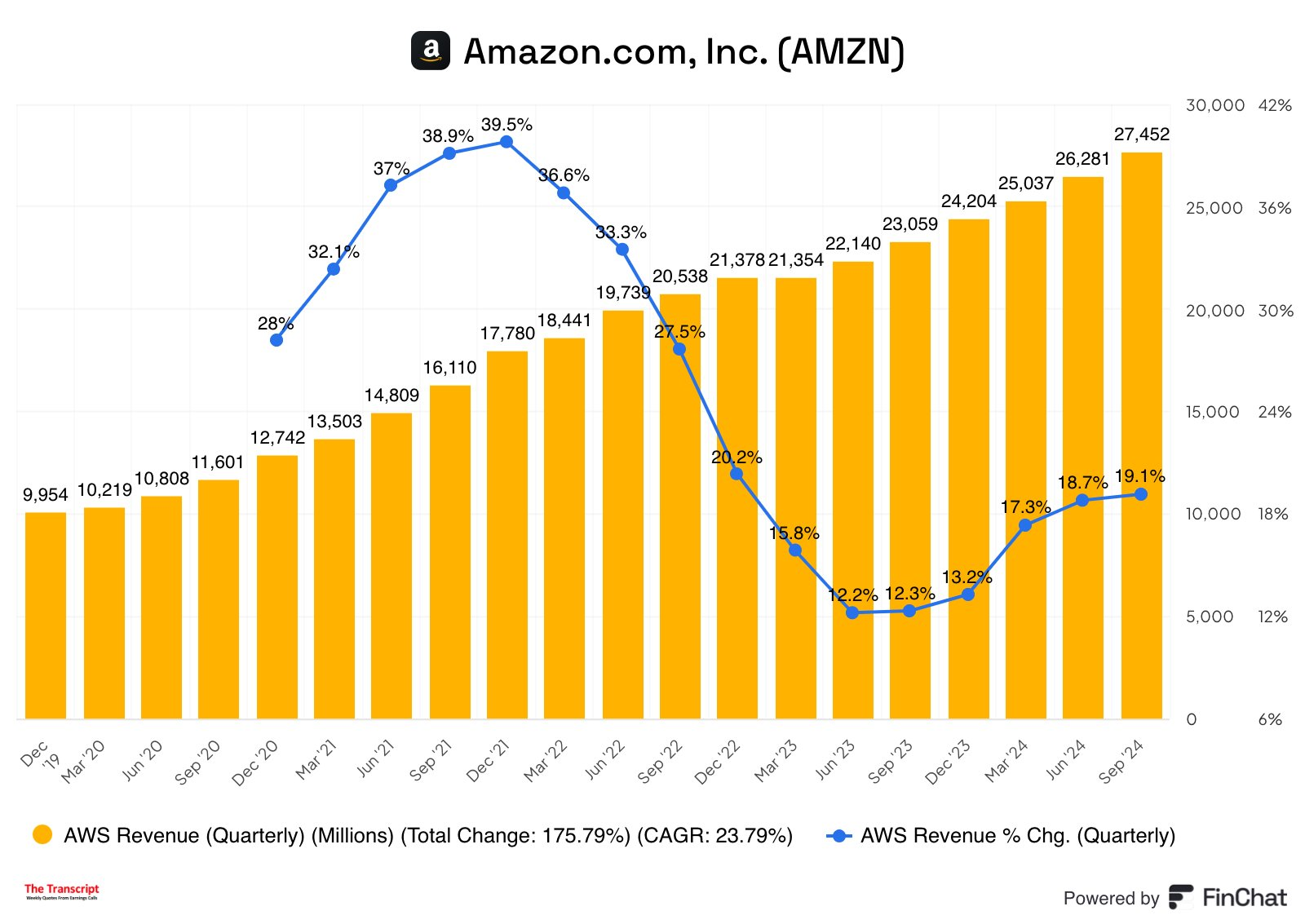

Amazon won the reporting season game last week helped by a continued acceleration of its cloud business...

@TheTranscript_: $AMZN CEO: "We've seen significant re-acceleration of AWS growth for the last four quarters..."

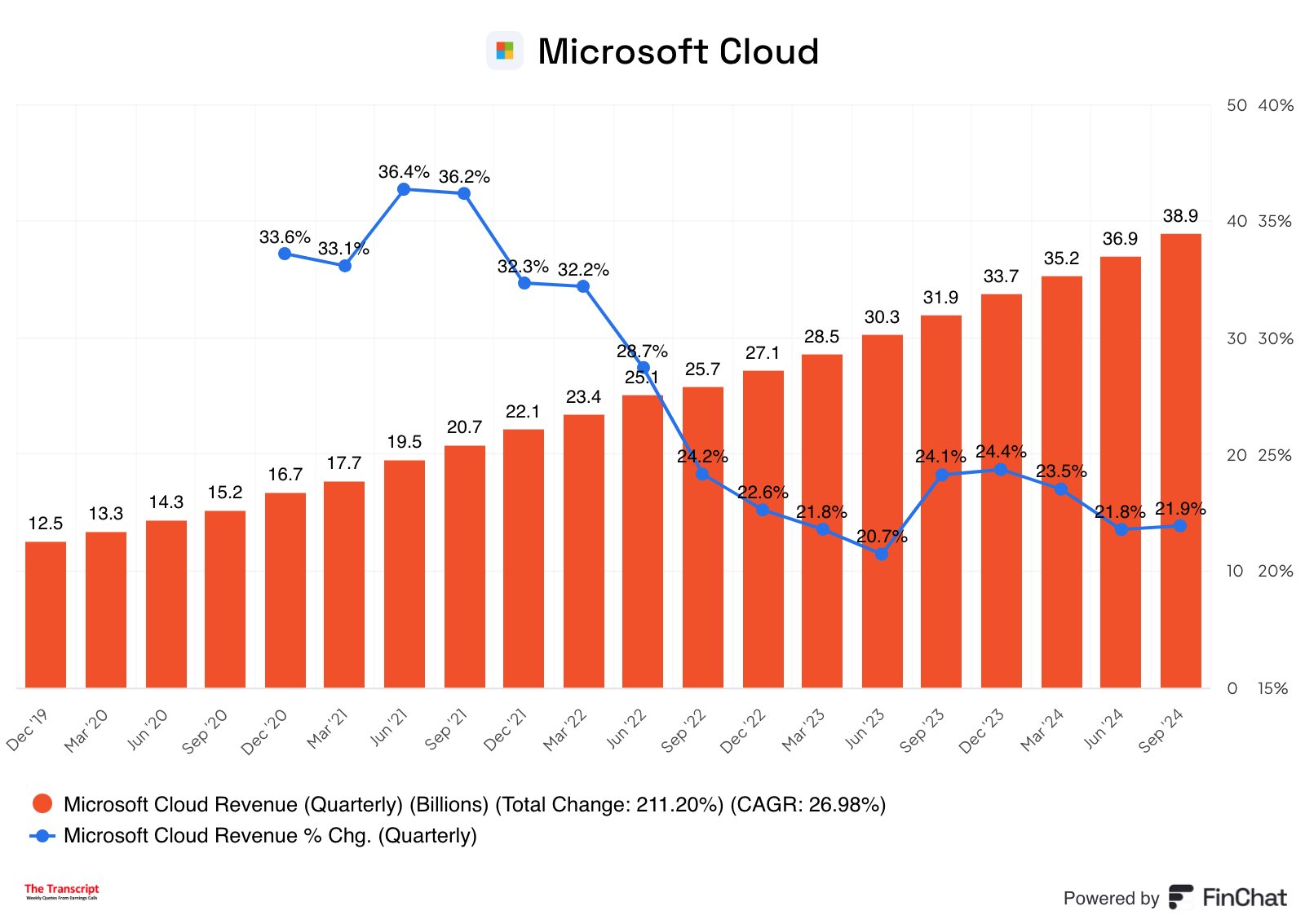

Not to be ignored is the size of Microsoft's cloud business which is still growing 20%+ off of a tougher comparable...

@TheTranscript_: $MSFT CFO: "Microsoft Cloud revenue was $38.9B and grew 22% roughly in line with expectations.

The number of earnings releases will grow this week, but the composition will be oriented toward smaller capitalization companies...

(@WallStHorizon)

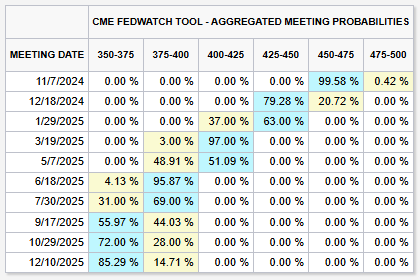

On Thursday, the FOMC will announce its decision on Fed Funds rates...

The market sees a 99%+ certainty that it will lower rates by 0.25%. Let the guesses for December begin.

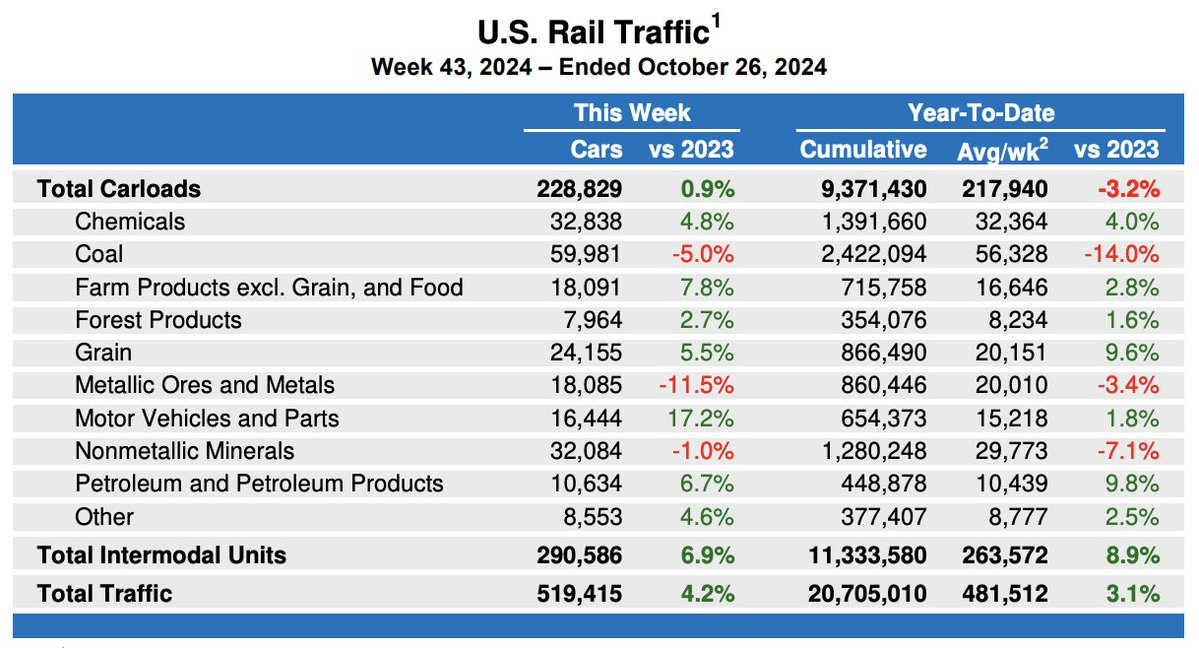

Continued strength in U.S. rail traffic (and especially intermodal) might argue for no more rate cuts...

Although companies in the more commodity oriented industries could make the opposite case.

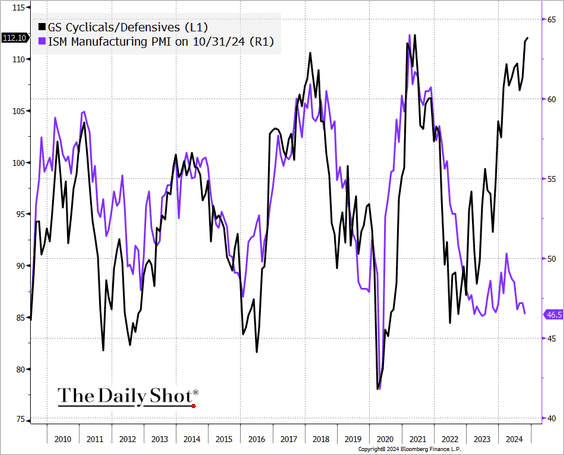

Stock prices continue to suggest an acceleration of the U.S. economy versus what we read in the manufacturing surveys...

The outperformance of cyclicals over defensives has diverged from the ISM Manufacturing PMI.

The oldest equity index gets another makeover...

Nvidia will replace Intel in the Dow Jones Industrial Average next week, a swap that reflects their reversal of fortunes within the tech industry. Sherwin-Williams will replace Dow Inc. as well.

S&P Dow Jones Indices, which manages the 30-stock benchmark, said the changes were made to ensure a more representative exposure to the semiconductors industry and the materials sector. They are effective prior to the open of trading on Nov. 8...

Unlike the S&P 500 and the Nasdaq Composite, the blue-chip index is weighted by share price, not by market capitalization. It is calculated by adding the prices of the 30 stocks and dividing by a factor that accounts for changes such as stock splits and index entrants. That means that companies with a higher share price have a greater effect on index moves, regardless of their total market value.

With a share price of $23.20, Intel was by far the least influential stock in the benchmark, while Dow Inc. was No. 28. At $135.40, Nvidia would rank 22nd—it executed a 10-for-1 stock split in June that analysts said made its inclusion in the Dow more likely. Sherwin-Williams closed Friday at $357.97, which would give it the sixth-highest share price in the index.

The Dow has lagged behind the S&P 500 and Nasdaq in recent years because it is less oriented toward technology stocks. It is up 12% this year, while the other indexes have climbed more than 20%. The Dow’s last shake-up came in February, when online retail powerhouse Amazon.com replaced Walgreens Boots Alliance.

As the private markets continue to outraise the public markets, more entities are lining up to price and trade private equity securities...

Nasdaq Private Market LLC is publicly launching a proprietary pricing product for private companies, joining an increasingly competitive space for data on potential IPO candidates.

For the past month, privately-held NPM has been showing off a product called Tape D to its own investors – Wall Street’s biggest banks. Now, the firm is unveiling its offering more broadly with a public launch on Thursday.

With companies like SpaceX and Stripe able to achieve eye-popping valuations without selling a single share in the public markets, providers like NPM and its rivals are competing to establish their products as the go-to reference.

“It’s already a $3.5 trillion asset class. There’s already more capital raised each year in the Reg D than in the public markets,” NPM Chief Executive Officer Tom Callahan said, referencing the US Securities and Exchange Commission’s regulation that allows private companies to sell shares without registering. Tape D is meant to empower investors and “decrease the information asymmetry” that persists in the private market, Callahan said in an interview...

Since NPM’s inception in 2013, the firm has executed more than $55 billion in transactions, Callahan said. Hence the opportunity for Tape D. “What do the capital markets look like a decade from now? We’re going to have far fewer public companies and we’re going to have more unicorns,” he said.

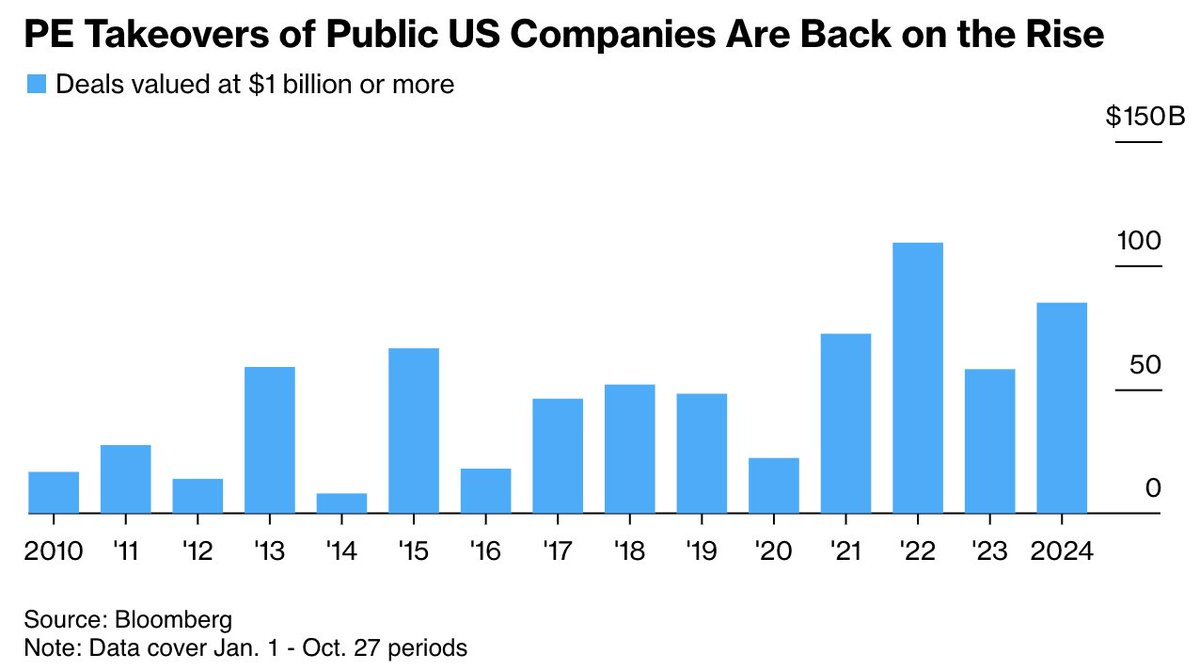

Public companies going private continues to see an acceleration...

@dailychartbook: Private equity firms "have struck almost $85 billion in deals this year involving listed US targets... That’s up by roughly half on the same point in 2023 and the second-highest year-to-date tally since 2010."

Here is a Russell Small Cap is going private via a leading infrastructure/real asset general partner...

Stonepeak is paying about 3.5x ebitda and 20x trailing earnings. Amazon is a top customer and owns 20% of the company. Important to highlight that this is a capital intensive business. So, Air Transport deciding to shed its public equity vehicle tells you that it is not going to be capital constrained in becoming a 100% private company.

AIR TRANSPORT SERVICES GROUP, INC. is a leading provider of air cargo transportation and related services to domestic and foreign air carriers and other companies that outsource their air cargo lift requirements. The company is the largest provider of passenger charter service to the United States Department of Defense and other governmental agencies. Besides the Department of Defense, major customers of the company include Amazon.com, DHL and United Parcel Service. The company also offers a wide range of air-transportation-related services to its customers including aircraft maintenance and modification, ground handling and crew training.

(Barchart)

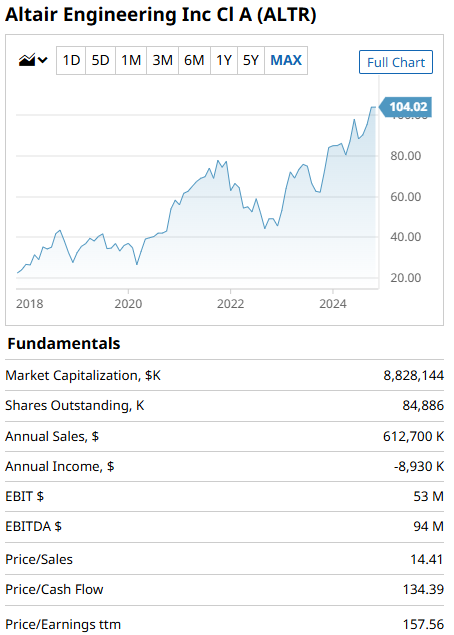

Software simulation company Altair Engineering is leaving the world of publicly traded Mid Caps in a deal with global giant Siemens...

Siemens is acquiring Altair Engineering in an equity deal that values the software and technology company at about $10.6 billion.

The German industrial giant said Altair shareholders will receive $113 per share in cash, representing a 19% premium to the closing price of Altair’s common stock on Oct. 21, the last trading day prior to media reports about a potential deal. The price represents a 13% premium to Altair’s unaffected all-time high closing price, Siemens said Wednesday...

The acquisition would help Siemens add growth of about 8% to its digital business revenue, or 600 million euros ($649.2 million) when compared to the EUR7.3 billion reported in fiscal 2023.

(Barchart)

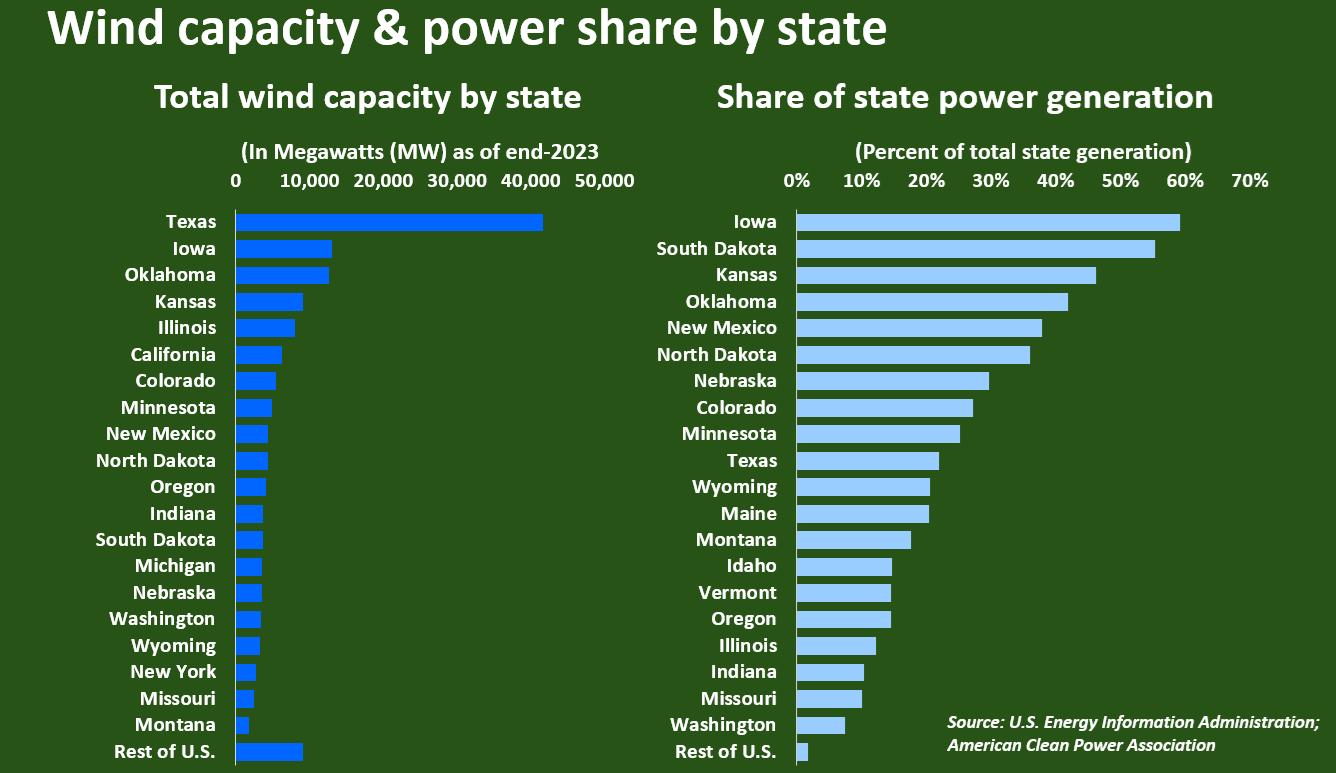

Iowa truly enjoys all the hot air being blown its way...

LITTLETON, Colorado, Oct 31 (Reuters) - Wind farms have generated a record share of U.S. electricity production so far in 2024, and are the second largest source of clean power behind nuclear plants in the U.S. generation system...

In terms of wind power's share of the power generated in each state, Iowa has the largest wind share of nearly 60%. South Dakota (55%), Kansas (46%), Oklahoma (42%) and New Mexico (38%) round out the top five. Texas generates 22% of its state power from wind. At the system level, the Southwest Power Pool - which covers 14 states stretching from Oklahoma to North Dakota - generates around 37% of its power from wind farms. The Electric Reliability Council of Texas (ERCOT) system has the next largest wind share of 24%, followed by the Midcontinent Independent System Operator (MISO) system, with 14%.

Now who can convince the NYSE and Nasdaq to move to a four-day a week schedule?

Iceland’s economy is outperforming most European peers after the nationwide introduction of a shorter working week with no loss in pay, according to research released Friday.

Between 2020 and 2022, 51% of workers in the country had accepted the offer of shorter working hours, including a four-day week, two think tanks found, saying the figure is likely to be even higher today.

Last year, Iceland logged faster economic growth than most European countries and its unemployment rate is one of the lowest in Europe, noted the Autonomy Institute in the United Kingdom and Iceland’s Association for Sustainability and Democracy (Alda).

“This study shows a real success story: shorter working hours have become widespread in Iceland… and the economy is strong across a number of indicators,” Gudmundur D. Haraldsson, a researcher at Alda, said in a statement.

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: Nvidia Corp., Amazon.com Inc. and Apple Inc.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.