Weekly Research Briefing: Swim Time

It's the last week of July and this will be a busy one both for the markets and in the Olympic swimming pool of Paris La Defense Arena. The FOMC meeting, the monthly jobs data, and biggest week of the earnings season for the S&P 500 are on deck. While the outlook for investors might be getting clearer, there will still be no running allowed poolside. It only takes one missed number or unexpected comment to crush a stock price or send rates higher.

I would look for a more dovish Fed meeting as the FOMC sets the table for a September rate cut on Wednesday. The FOMC has plenty of room to ease with inflation falling as planned and job growth weakening. Lower rates will help both auto and housing sales in addition to the many manufacturers in the ISM surveys calling for interest rate relief. The commercial real estate industry will also welcome lower financing costs. The U.S. Treasury 2-years vs 20/30-year spreads have gone positive which is good news for financial stocks and could push banks to increase their lending.

Earnings are coming in swell and the beats are being rewarded. The fly in the suntan oil is that revenues are a bit on the light side. Margins have been helped by falling input costs and more stable wages. But these improvements will run out in future quarters. And so one more reason for the Fed to begin cutting rates. This is a big week for earnings with four of the giants reporting. With the Mag-7 currently oversold, any earnings comfort could bounce the stocks strongly. On the flipside, if the giants show that AI profits will take longer than expected, then the other 2,993 companies in the U.S. stock market will need to continue to do the heavy lifting. Speaking of weightlifting, those Olympic events do not start until next week. Have a great week.

First, a look at the Q2 earnings to date...

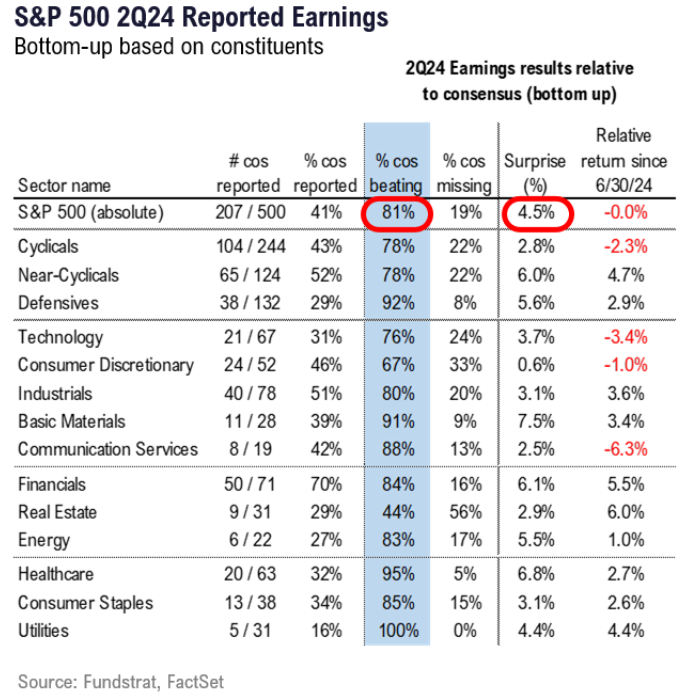

Of the 207 companies that have reported so far (41% of the S&P 500):

- Overall, 81% are beating estimates, and those that “beat” are beating by a median of 5%.

- Of the 19% missing, those are missing by a median of -5%.

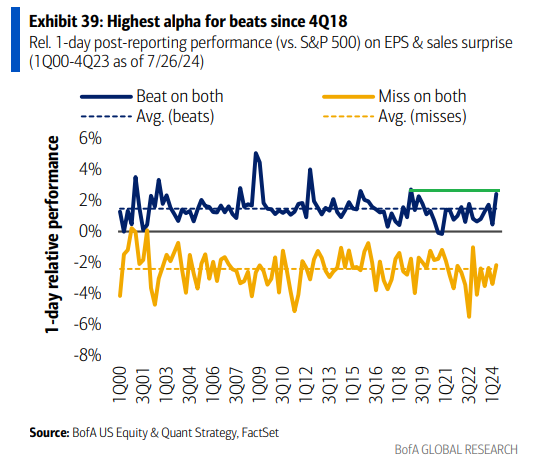

This is the best 'EPS beat' stock price performance in six years...

BofA Global

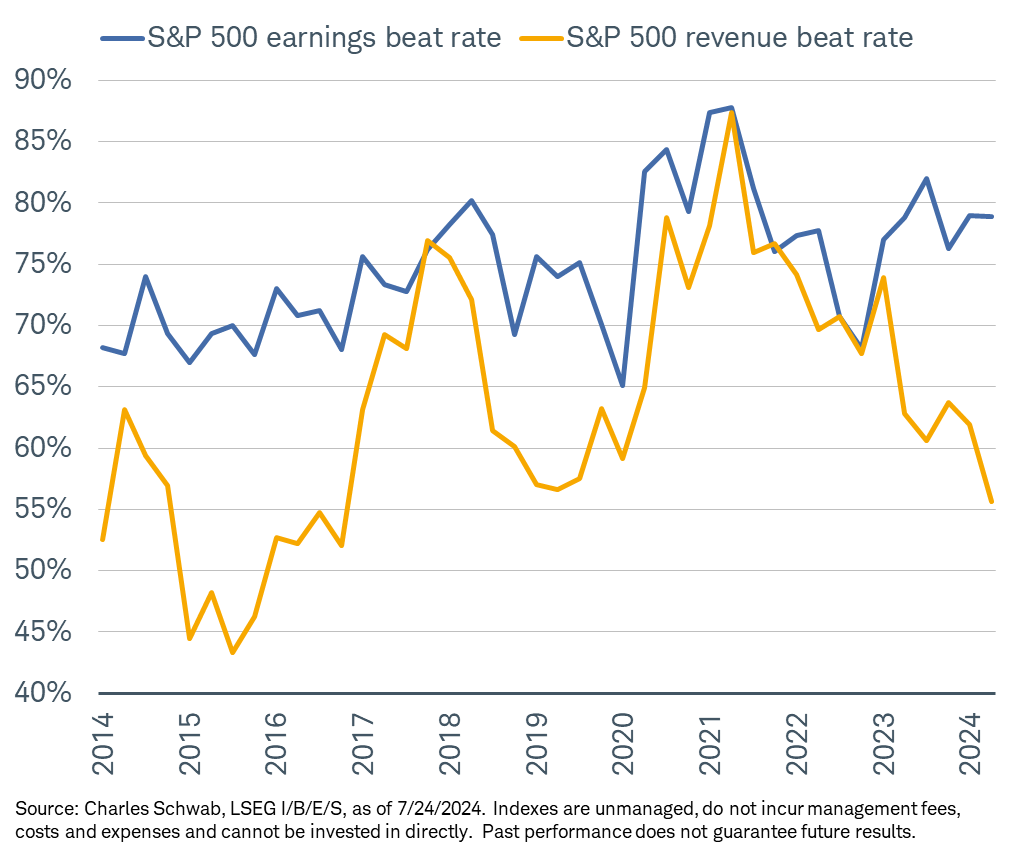

But while margins are saving the bottom line, revenues are coming up short...

@KevRGordon: S&P 500's earnings beat rate is still healthy at nearly 79%, but the revenue beat rate is currently at its lowest since the fourth quarter of 2016

Several companies have mentioned on their calls that they are looking forward to Fed easing...

“We’ve seen the downturn of consumer discretionary demand intensify since 2022 and existing home sales hit multi-decade lows in 2023 and 2024. There is no doubt that we have been and still are at a low point in the U.S. housing market. With interest rate reductions, this will ease at some point, and we are well positioned to benefit from improving demand” - Whirlpool CEO Marc Bitzer

"...the aspirational customers in the U.S., as we commented in the first quarter of the year is a little bit under pressure due to inflation and higher interest rates that are taking both the toll in terms of purchasing power, particularly in the U.S. and to a lesser extent in Europe. This is not nice." - LVMH CFO Jean-Jacques Guiony

"inflation is heading in the right direction now that residual seasonal factors are largely behind us. With the odds of a Fed rate cut this year now higher, we expect further improvement in the operating environment for both of our businesses." - Lazard CEO of Financial Advisory Peter R. Orszag

Expect the next FOMC meeting to have a more dovish tone...

Policymakers have for months pointed to the resilience of employment data as evidence that there’s no urgency to lower rates. But the message from rate-sensitive parts of corporate America this earnings season has been clear: demand is sagging and the main thing keeping layoffs at bay is confidence that rate cuts will begin soon and usher in a brighter outlook for 2025. The Fed now needs to deliver not just one but a series of reductions to maintain business confidence and ensure there’s no further deterioration in the labor market.

About a third of the way through second-quarter earnings season, the proportion of companies beating revenue expectations is the lowest since 2019, according to Bloomberg Intelligence. The slowdown is particularly apparent in parts of the economy tied to household borrowing and consumer credit. Squeezed budgets have resulted in a miserable quarter for the automobile industry where rising inventories have put downward pressure on prices, crimping profit margins. Similarly, existing home sales in June were back near the lowest levels in a decade, bad news for companies that depend on housing turnover such as Maytag owner Whirlpool Corp., which said that the recovery they expected in 2024 isn’t going to happen.

The dynamics in these consumer-facing industries have contributed to a sustained rise in the unemployment rate, which last month reached its highest point in more than two years. In general, that’s the kind of environment that could quickly get out of hand, even if headline real gross domestic product numbers still look solid. In the fourth quarter of 2007, for instance, real GDP grew 2.5% right before the economy tipped into recession.

Commentary from many hard-hit companies, however, shows why we won’t repeat the downward spiral that the labor market experienced during the financial crisis — if the Fed acts quickly. Whirlpool said during its earnings call that it would stand to benefit once interest rate reductions ease pressure in the housing market. Brunswick Corp., the maker of recreational marine products, noted rate cuts beginning in September would provide a tailwind next year. (Yes, we’re now at the point where boat makers are tracking Fed expectations as closely as banks!) And Pool Corp., a distributor of swimming pool supplies, said that orders haven’t picked up yet, but increased inbound calls show customers are just waiting for confirmation on lower borrowing costs before making a decision.

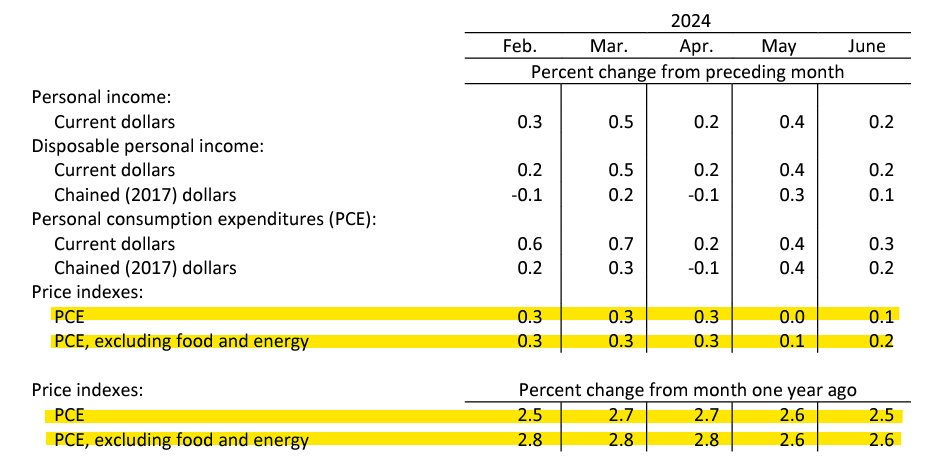

If the Fed needed more elbow room to begin cutting rates, they got it with last week's inflation reading...

@MMInvestor0: US June PCE price index increased 0.1% month over month. Excluding food and energy, core PCE price index increased 0.2% MoM. PCE came in at 2.5% YoY and Core PCE came in at 2.6% YoY.

Former FOMC teammate, Bill Dudley, also gave the Fed a reason to cut after shifting 180 degrees away from his 'higher for longer' stance...

I’ve long been in the “higher for longer” camp, insisting that the US Federal Reserve must hold short-term interest rates at the current level or higher to get inflation under control.

The facts have changed, so I’ve changed my mind. The Fed should cut, preferably at next week’s policy-making meeting.

For years, the persistent strength of the US economy suggested that the Fed wasn’t doing enough to slow things down. The government’s pandemic-era largesse left people and businesses with plenty of cash to spend. The Biden administration’s vast investments in infrastructure, semiconductors and the green transition boosted demand. Easing financial conditions — particularly a surging stock market — increased wealthier households’ propensity to consume. Containing the resulting inflation, it seemed, would require sustained monetary tightening from the Fed.

Now, the Fed’s efforts to cool the economy are having a visible effect. Granted, wealthy households are still consuming, thanks to buoyant asset prices and mortgages refinanced at historically low long-term rates. But the rest have generally depleted what they managed to save from the government’s huge fiscal transfers, and they’re feeling the impact of higher rates on their credit cards and auto loans. Housing construction has faltered, as elevated borrowing costs undermine the economics of building new apartment complexes. The momentum generated by Biden’s investment initiatives appears to be fading.

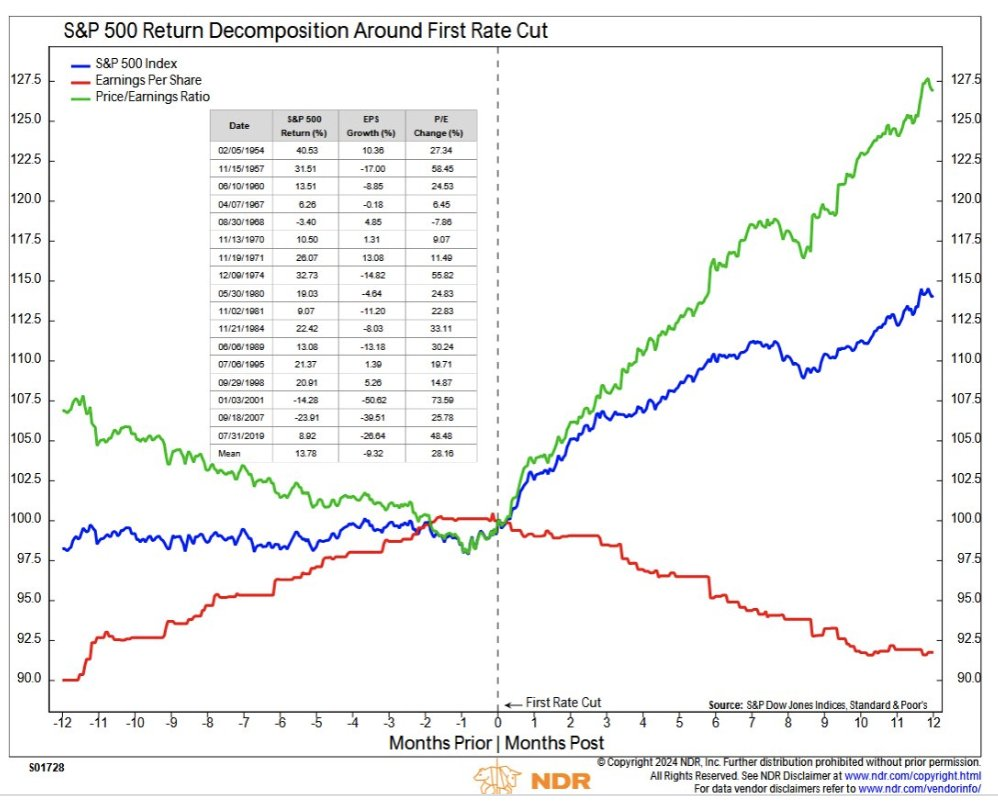

History shows that the S&P 500 return transitions from EPS growth to multiple expansion after the Fed's first rate cut...

Could this happen again even as S&P 500 earnings have begun to accelerate? This next observation period will be interesting.

@NDR_Research

The homebuilder construction ETF is screaming interest rate cuts and is one of the best-looking charts in the market right now...

@hmeisler

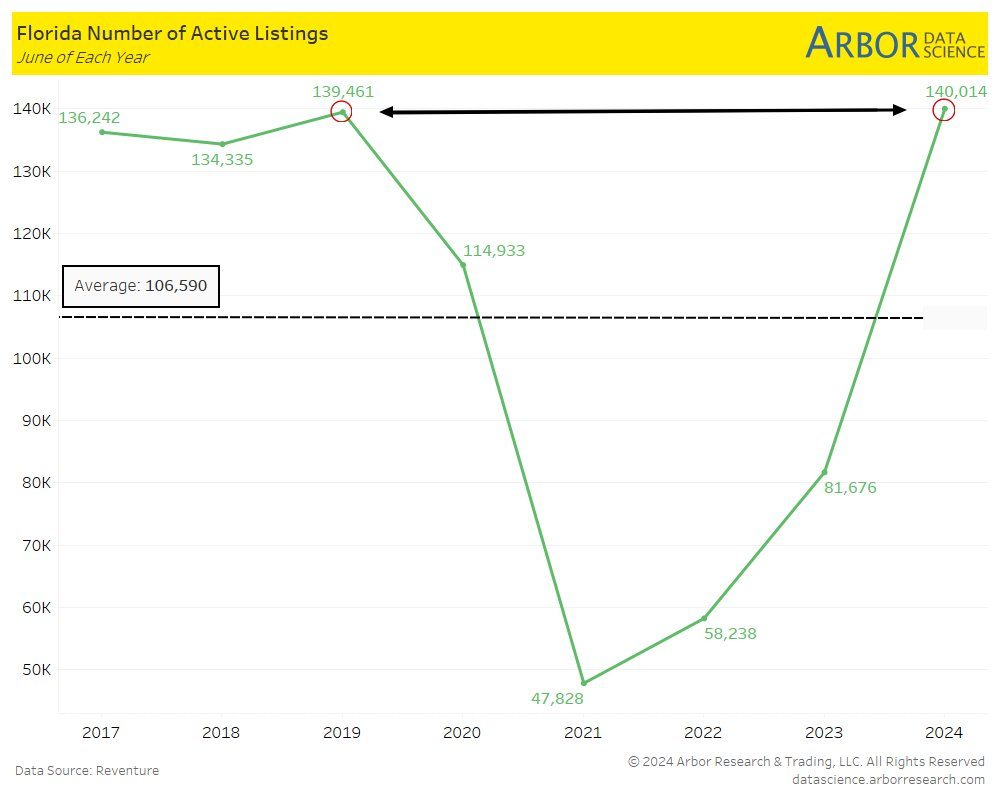

Homeowners in Florida will soon be the FOMC's biggest fan base...

@DataArbor: Florida’s Housing inventory Surpasses 2019 levels

The last big flood of S&P 500 earnings reports this week with four of the Mag-7 reporting...

Next week the SMid-caps will take over the earnings tape. Will there be more interest in the smaller company earnings reports with the Russell 2000 index's recent outperformance?

@WallStHorizon

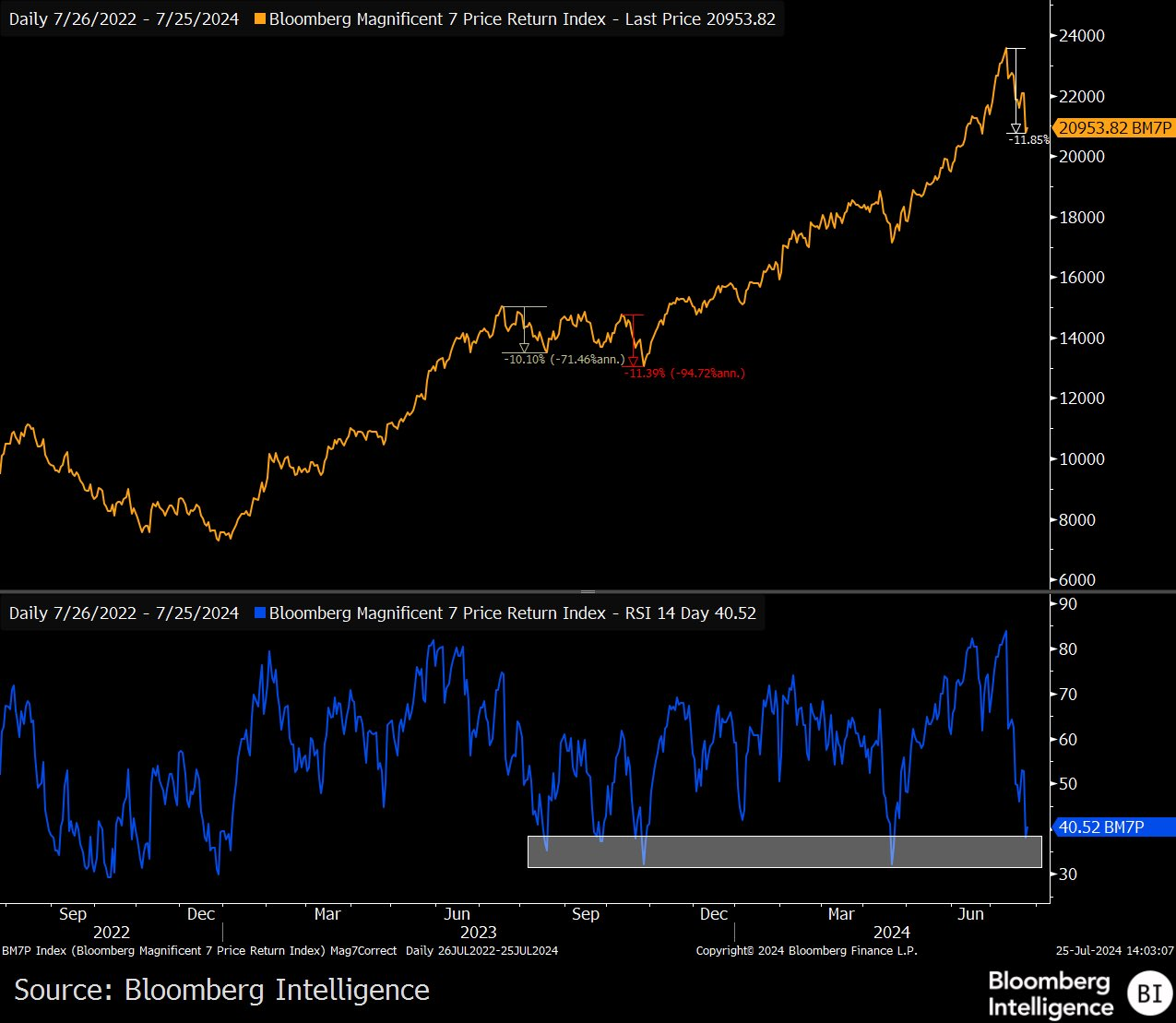

This is the week for the Mag-7 to choose: are you a Tennis ball or a Cannonball?

@GinaMartinAdams: This 3Q has been unkind to the Magnificent 7 stocks, which have experienced their worst drawdown yet of the 2023-24 bull market. Yet the group is nearing oversold levels just as key earnings reports from Microsoft, Meta, Apple and Amazon are due next week.

The rotation in public markets is good for private equity and M&A...

A top M&A advisor notes how the broadening of equity valuations will improve transaction activity.

"I'll say with the rotation going on in valuation in the public market, the rotation away from all this value, all the gains in public valuation going really 7 or 8 large-cap stocks. And really in the last 2 or 3 weeks, you've seen a tremendous rotation into the Russell 2000 in the middle market, that's much more of a comp for sponsor valuations. As I said, very few of our companies, sponsor companies comp to the MAG 7. They mostly comped to other $5 billion, $10 billion companies in the market and as that value parameter swings, and it swung a lot in the last 2 or 3 weeks, I think that's a very good sign for activity in sponsor land." - Moelis CEO Kenneth Moelis

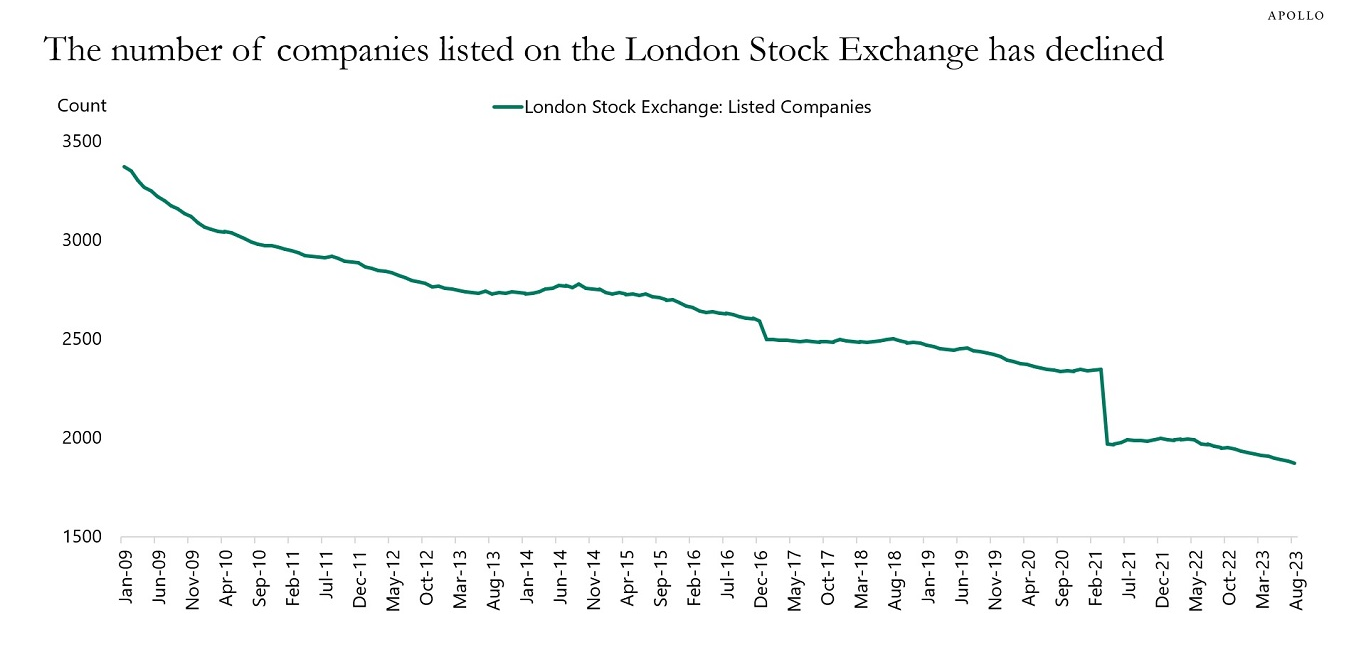

The shrinking public markets are not just a U.S. phenomenon. Here is the U.K...

And if you own a passive index mutual fund or ETF whose primary criteria for inclusion is market capitalization, then prepare to own some junk...

A little over two years ago, millions of investors found themselves owning a stake in Enochian Biosciences, a money-losing drug development company few had heard of.

Even fewer would have bought it on purpose. The man listed as its “scientific founder” and largest shareholder had just been arrested for murder. It turned out that he wasn’t a doctor as claimed, or even a college graduate, and that he was wanted for selling bogus cures in his native Turkey. Despite that much of that was public information already, a large number of the company’s shares were bought automatically by funds that track the Russell 2000 index, the most closely followed gauge of America’s small companies.

Several weeks earlier, on what is called “Rank Day” in the small-cap stock-investing world, Enochian had gained entry by being worth at least $240.1 million—that year’s cutoff. Its stock had doubled in the previous year to $7 a share. On the day that index funds were forced to buy it while simultaneously selling companies booted from the benchmark, they still paid as much as $3.70 a share. Over the ensuing 12 months, the stock lost another 85% and then saw another flurry—this time, of forced selling—locking in a loss.

Investors who embrace passive investing pay too little attention to how stock indexes are built. Companies gaming the system, or just being of low quality, create an imperceptible drag that has cost investors hundreds of percentage points of gains over the years.

Close to $11 trillion of investor money follows various Russell indexes, and its leading ones are based on market value alone, slicing the market into about 1,000 large-capitalization stocks, 2,000 small-capitalization ones and microcaps below that.

Capital market activity continues even as we head into the big vacation month of August...

- Russell 2000 small cap insurance component goes private...

An investor group led by Sixth Street agreed to buy property and casualty insurer Enstar Group Ltd. for $5.1 billion, in the second-largest private equity backed insurance deal of the year... Enstar, formed in 1993, helps other insurance providers manage their risks by acquiring or re-insuring legacy blocks of business, often accident-related policies written several years before. The company makes money by carefully managing the liabilities as they run off while investing proceeds in investments and new acquisition opportunities, according to its annual report. (Bloomberg) - $3.5 billion private equity to private equity deal...

Private equity investor Advent International said on Thursday that it has agreed to sell UK parcel delivery firm Evri to funds managed by affiliates of Apollo. The deal values Evri at 2.70 billion pounds ($3.47 billion), two sources familiar with the matter told Reuters. In January, Reuters had reported citing sources that Advent was considering options, including a potential sale, for Evri, which delivers over 12 million parcels a week to UK e-commerce shoppers.(Reuters) - Russell 1000 and S&P 400 component spends $1.2b to further roll-up the convenience store industry...

Casey’s General Stores (CASY) is expanding its footprint across the South with an all-cash $1.2 billion deal that includes nearly 200 outlets and a dealer network. The stock jumped 6.9% on Friday’s announcement. Casey’s, a chain of convenience stores mostly in the Midwest, will acquire Fikes Wholesale, owner of Cefco Convenience Stores. Included in the sale are 198 stores and a dealer network throughout Texas, Alabama, Florida and Mississippi. Of the stores, 148 are in the Lone Star State... The deal, expected to close in the fourth quarter, will expand Casey’s operation to nearly 2,900 stores. (Barron's) - And another profitable Russell 2000 component exits the stock listings...

Apollo Global Management is raising its bet on the gaming market. The New York private equity firm is buying Everi Holdings and the gambling and slot machine business of International Game Technology IGT in a deal valued at about $6.3 billion. The transaction replaces a previous deal in which IGT said it would spin out its gaming arm and merge it with Everi to build a company generating about $2.7 billion in annual revenue... The move would bring together a broad portfolio of assets spanning gaming, online wagering and sports betting under Apollo, which has pushed deeper into gaming with a number of acquisitions in recent years. (WSJ) - Penn Mutual Life sells JMS to private equity...

Private equity firm KKR is acquiring wealth manager Janney Montgomery Scott, the companies revealed on Tuesday. The transaction is expected to close in the fourth quarter of 2024. Specific financial terms of the deal were not disclosed. KKR is acquiring Janney primarily through its North America Fund XIII, the firm said. Janney has been owned by The Penn Mutual Life Insurance Company since 1982 and currently has $150bn in assets under administration. Based in Philadelphia, the firm has over 900 financial advisors across 135 offices. (RIA Insider) - Private equity owned AI cloud play goes public and leaps over the small cap stock universe in its first week...

OneStream Inc. and a group of shareholders including KKR & Co. raised about $490 million in a US initial public offering, pricing its shares above a marketed range. The software company and its shareholders sold 24.5 million shares Tuesday for $20 apiece, according to a statement confirming an earlier report by Bloomberg News. OneStream had marketed the shares for $17 to $19 each. OneStream, which offers a cloud-based platform with more than 90 applications including accounting and budgeting, was marketing 18.1 million shares, and the shareholders were selling 6.4 million shares. At the IPO price, OneStream has a market value of around $4.6 billion based on the outstanding shares listed in its filings with the US Securities and Exchange Commission. (Bloomberg)

Various news sources

The largest U.S. IPO of 2024 is a cold storage logistics roll-up. And it just fired up the financial markets...

IPO's at $78. Now trading at $85 for a $20 billion valuation. Which private equity roll-up wants to go public next?

Fresh lobster from Maine. Bags of frozen peas. Racks of ribs, shrink-wrapped in plastic. Americans have come to expect that with a click of a button, almost any item, perishable or not, can be delivered to their homes the next day. The company that makes this all possible is a logistics operator most of us have never heard of but all of us depend on daily.

The world’s biggest cold-storage operator by capacity, Lineage, is so deeply embedded in the U.S. economy that when it listed its stock on the Nasdaq exchange this past week, it was the largest initial public offering in the U.S. so far this year. At $78 a share, the IPO raised $4.4 billion and valued Lineage at more than $18 billion.

Cold storage is a centuries-old industry, but Lineage’s own lineage is young. It was founded in 2008 by two former Morgan Stanley investment bankers, Adam Forste and Kevin Marchetti. Since then, the duo has amassed an empire that today operates nearly a third of the temperature-controlled warehouse space in the U.S.

The Novi, Mich.-based company, which counts Kraft Heinz, Darden Restaurants and Walmart among its clients, operates more than 480 temperature-controlled warehouses around the world. The business handles logistics operations such as storing, picking and packing items and offers e-commerce fulfillment, transportation and customs-brokerage services.

The success of Lineage is a function not just of fortuitous timing, but also a savvy recognition that the businesses storing and transporting the perishable items Americans have come to rely on could be rolled up and streamlined.

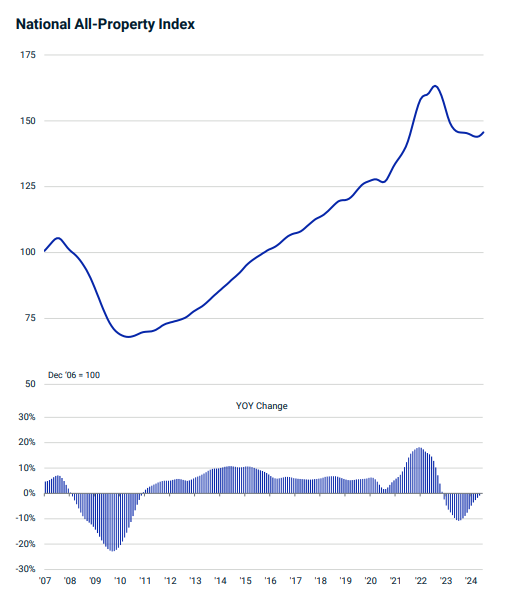

Well look what also unfroze this month...

@tracyalloway: US commercial real estate prices ticked *up* for the first time in a year and a half, according to MSCI data.

The size of these drug sales numbers are staggering to think about...

@wallstengine: $LLY $NVO | UBS: GLP-1 Obesity Market to Reach $90B by 2029

"We project the GLP-1 obesity market will grow to $90B by 2029, with the combined obesity and diabetes market hitting $150B, reflecting a 33% CAGR from 2023-2029."

"Key drivers include the expansion in obesity treatments, with 28M GLP-1 patients expected by 2029, representing 9% penetration of non-T2D obese patients."

"We believe the market is underestimating orforglipron's potential, raising our sales forecast to $17B by 2029. Despite ongoing pricing discussions, we don't foresee significant near-term headwinds while the market remains constrained."

"We predict a duopoly between Eli Lilly and Novo Nordisk will persist, with new entrants capturing less than 10% market share by 2029."

Public equity and private equity investors have more in common than you may think…

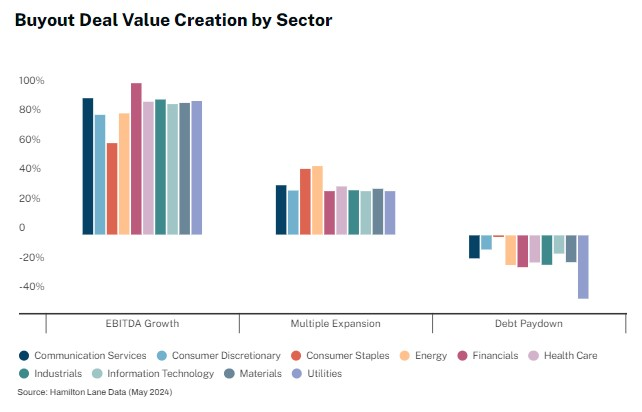

As a former stock picker, my goal was to find a company with growing cash flows that would increase the value of the entity for the benefit of investors. If I was fortunate in my selection, other investors would follow, and the multiple would expand thereby providing an additional return. The chart below breaks out the value creation by sector across 6,000 buyout deals. Easy to see that the bulk of the value creation is coming from the increased cash flow generation of the invested buyout companies. Buyout investing also tends to get a bit of icing on its cake from the EBITDA multiple expansion between the buyout date and sale date. Just like public stock investing.

Debt paydown is the difference in net debt between the exit and acquisition period, which can shed light on a company’s debt management practices. Contrary to buyout critics, this data demonstrates that GPs focus on enhancing fundamentals rather than relying on obscure financial engineering or gutting companies to extract value.

Definitions: Corporate Finance/Buyout: Any PM fund that generally takes control position by buying a company.

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.