Weekly Research Briefing: The Dog Days are Over

The dog days are over

The dog days are done

Can you hear the horses?

'Cause here they come

(Dog Days Are Over, Florence + the Machine)

After 2.5 years and 500 basis points of Federal Funds rate increases, the Fed will now embark on a path of interest rate cuts starting at the September meeting. While the move toward easing has been predicted by many Wall Street participants, the greatest impacts moving forward will be felt on Main Street America. Fed fund rate cuts of 100 basis points into year-end 2024 will be soon felt by consumers and small businesses who revolve credit or need financing to buy large ticket items. Lower interest rates will also help businesses whose customers have been hurt by high rates or who need financing themselves. These small turns from less certainty toward more certainty should install confidence in employers and employees which will begin to improve the labor picture. As this economic flywheel speeds up, the credit and lending markets will cheer as the probability of a near term recession falls to zero. Lying dogs out, galloping horses in.

For the financial markets, much of the Fed's future actions have been anticipated. Public equity multiples are higher than average and credit spreads are tighter than normal. Investor cash levels seem a bit excessive currently, but there is probably still a delayed reaction to the thought of earning 4-5% on money at the bank. Watch cash hoards fall as greenbacks return to earning only 2-3% in 2025. So where will cash assets redeploy? Some will go into interest rate beneficiaries like real estate assets. Some will head overseas as falling rates weighing on the US$ will make foreign investing more attractive. Some will move into small company investing which should benefit from improved economic activity and lower borrowing costs. Just think back three years to all the charts and graphs we built for assets which would underperform from rising rates and now consider the opposite.

As we head into the summer's final holiday, this will be a good week for economic readings with GDP and core PCE headlining. Also important on Wednesday will be Nvidia's quarterly earnings which should provide many datapoints for AI and data center growth activity. The big numbers will be next week's August job data and will likely determine the size of cut by the FOMC at their September meeting. Monday is the Labor Day holiday and we will give our team a rest before the September's sprint. Have a great week and summer's end.

The Federal Reserve unveiled its pivot at Jackson Hole...

"The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks. We will do everything we can to support a strong labor market as we make further progress toward price stability. With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market." - Federal Reserve Chair Jerome Powell

“It was all inflation, inflation, inflation for a while Now we're starting to see things, the balance of risk, getting more equalized. So we do need to take more into account when it comes to the labor market, for sure....It means this September we need to start a process of moving rates down." - Philadelphia Fed Chief Patrick Harker

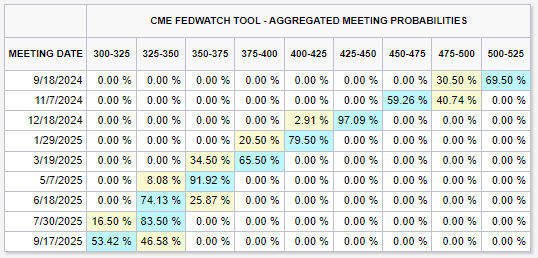

The market has anticipated the pivot and is leaning into 100 basis points of cuts through year end...

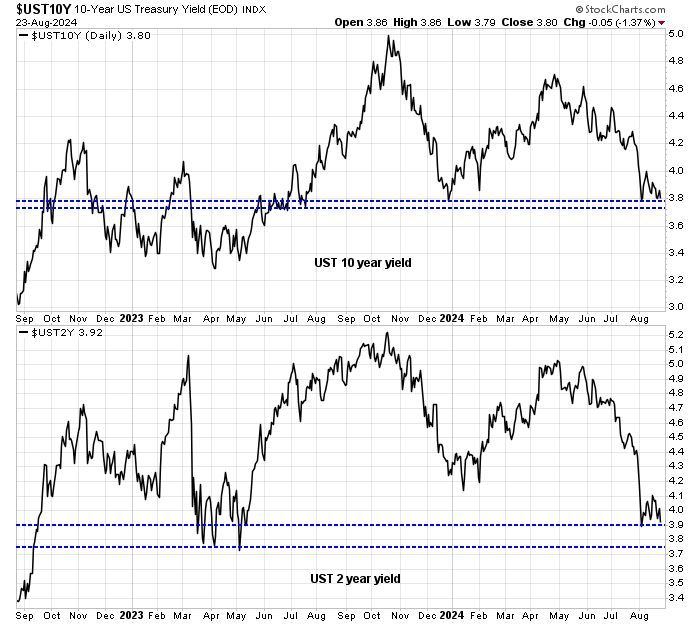

Two and ten year yields are now eyeing their 2023 lows...

(@HumbleStudent)

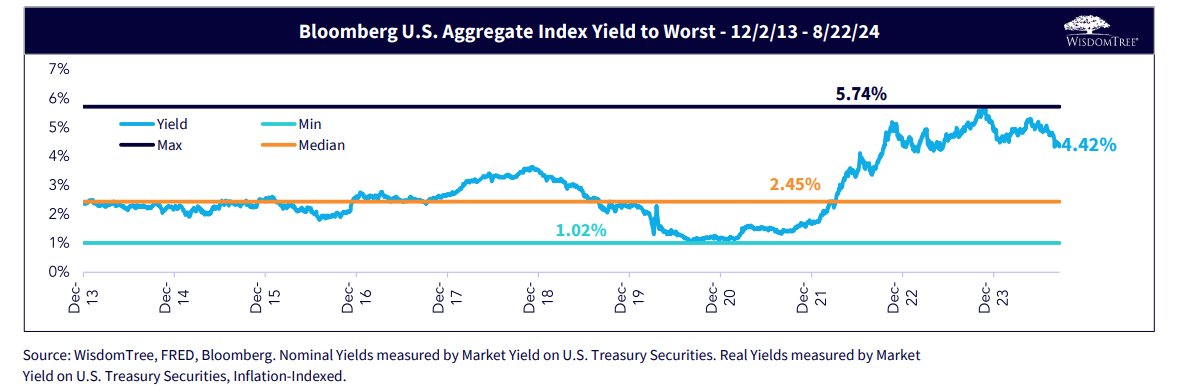

Corporate bond yields are also looking to take out the post-COVID lows...

Lower bond yields also being reflected in the falling yield of the major bond benchmark...

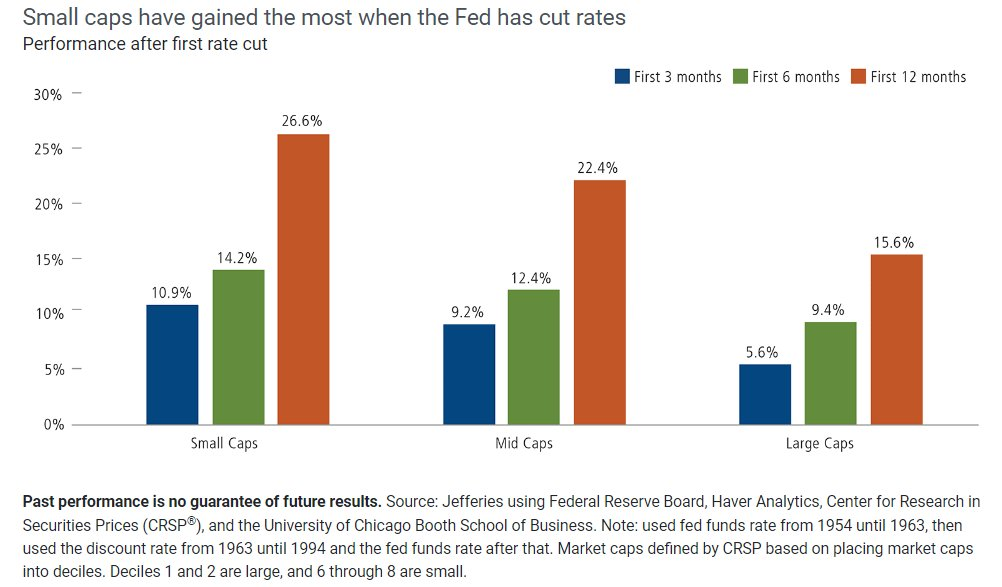

So, what should do better as interest rates fall?

History shows that small cap stocks outperform their larger cap siblings. This is typically due to smaller caps being more sensitive to improving economic activity while also having more leveraged balance sheets.

(@MikeZaccardi)

Real estate exposure could also be a winner as interest rates fall...

The cost of money is a major input into every real estate transaction. The broad REIT index lost 25% of its value as rates rose. As the economy improves, rates stabilize and borrowing costs fall, maybe there will be more here than what last year's buyers already anticipated.

(StockCharts)

"Be greedy only when others are fearful"...

Love to read these articles about distressed buyers going in where banks and insurance companies will avoid.

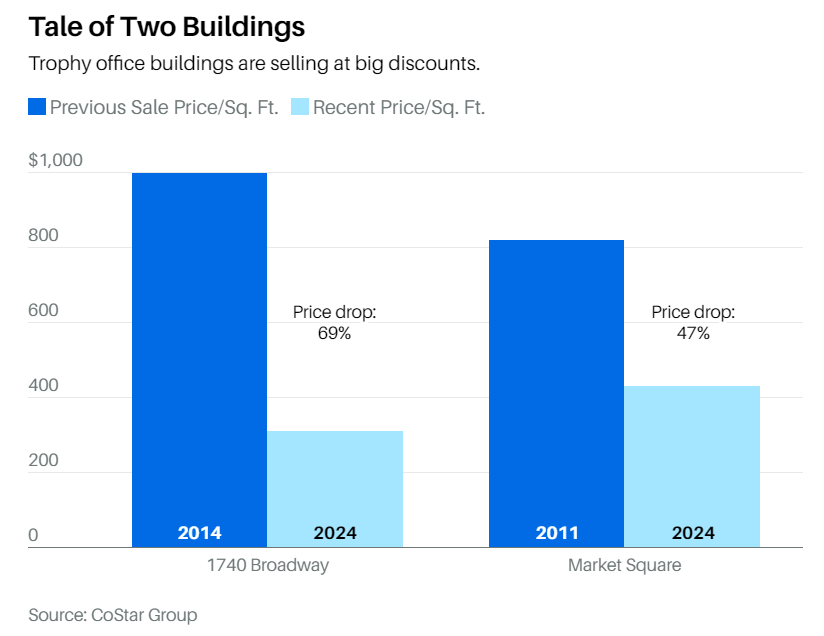

There’s too much office space in every city, says Paul Dougherty. That didn’t stop him from buying a pair of Washington, D.C., office buildings in March for $323 million. It’s one of the largest office deals this year.

Burdened by a stack of debt, the sellers had written the Market Square office complex down to zero. But it sits on Pennsylvania Avenue between the White House and Capitol, so it is popular with lawyers and lobbyists. Paying half what the sellers paid a dozen years earlier, Dougherty’s firm can now charge competitive rents.

“We can buy an amazing piece of real estate at 40% of replacement cost,” says Dougherty. “It’s a classic example of a great asset that had a bad capital stack but a good leasing story.”

Dougherty and other bottom-fishers are betting that if they can snap up office buildings cheaply enough, it won’t matter if the sector continues to decline. Because their purchase prices are so low, they say they will be able to charge cheaper rents than competitors and have the money to spiff up the spaces to lure clients...

In April, Isaac Hera’s Yellowstone Real Estate Investments bought the Deco-style tower at 1740 Broadway and 56th Street in Manhattan—once known as the MONY building—for $185 million.

Blackstone’s EQ Office had paid $600 million in 2014 for the 75-year-old office tower. The Covid pandemic foiled Blackstone’s plans to raise rents after renovating the building. In 2022, it defaulted on its $300 million loan.

“In today’s market, sellers are selling their properties because they have to, rather than because they want to,” Hera tells Barron’s. “Some are facing redemption requests, others are dealing with regulatory issues, and some have concentration problems.”

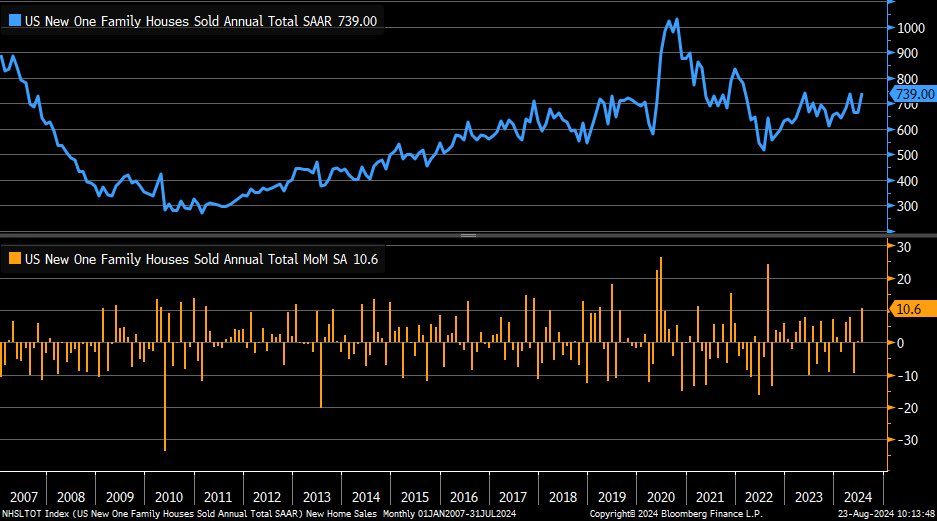

Lower mortgage rates will also help the housing food chain which showed some strength in July...

@LizAnnSonders: July new home sales +10.6% month/month vs. +1% est. & +0.3% prior (rev up from -0.6%) … median sale price of new home in July fell by 1.4% to $429,800

With the Fed now on a path to lower rates, the U.S. Dollar could be put on the defensive...

The US$ index is showing a 5-6% pullback off its 2024 highs today but risk seeking investors could get emboldened to allocate more into the foreign markets if the dollar takes out the 2023 lows.

(StockCharts)

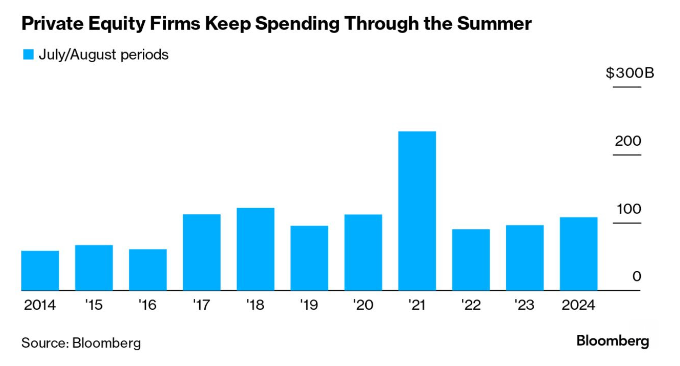

Private equity M&A was already picking up. How much will lower rates accelerate activity?

It’s been a hot summer of spending for private equity dealmakers. The value of acquisitions by buyout firms stands at roughly $103 billion for July and August. That’s up 15% on the same period last year and could yet be the third-highest tally for these two months in a decade, Bloomberg-compiled data show...

PE firms have cash to burn. The seven biggest publicly traded alternative asset managers, including the likes of KKR, Carlyle and Blackstone, were sitting on $722 billion at the end of June and investors have been eager for them to start putting their money to work.

“Pressure was building on these funds to sell assets in older funds and to deploy new capital into new companies,” said Emily Anderson, head of sponsor coverage at Union Square Advisors.

A long-awaited interest cut by the Fed next month is widely expected to provide a further boost to dealmaking, especially by debt-hungry buyout firms, during the back end of 2024.

“Grow or die, that’s what I believed, no matter the situation” (Phil Knight, Shoe Dog)

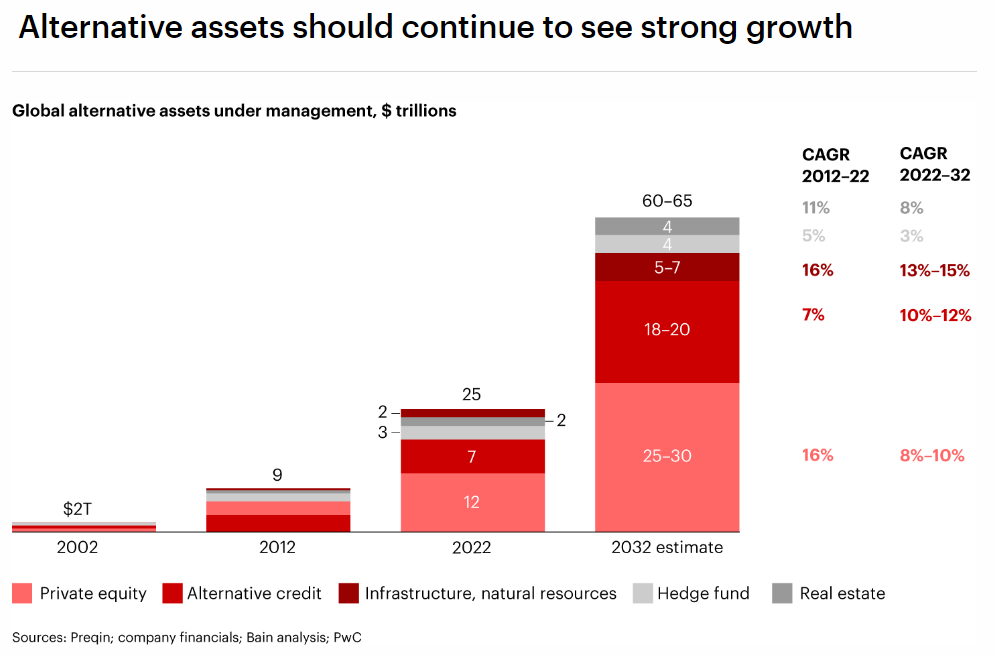

This new Bain & Company report illustrates why the public investment centric asset management industry will continue to move into private market assets. Slow unit growth, falling prices and shrinking margins for ETF and Mutual Fund companies hunting in a shrinking (and concentrated) pool of public companies has led them to look for another investment asset class to expand into. Expect every major asset management firm to have a private market unit and '40 Act' evergreen funds by the end of this decade.

Private assets constitute a much larger market than public assets and offer potentially higher yields, diversification, and in cases such as real estate, a hedge against inflation. Fewer companies have been going public in recent years, with global initial public offerings falling 45% from 2021 to 2023 due to increased regulation and higher costs. By contrast, we estimate that private market assets under management (AUM) will grow by a 9% to 10% compound annual growth rate (CAGR), reaching $60 to $65 trillion by 2032, more than twice the rate of public market AUM (see Figure 3). By 2032, we expect private market assets to account for 30% of all AUM.

In parallel, fee revenue for private market investments, at $0.9 trillion in 2022, should double to $2 trillion by 2032. Private equity and venture capital will continue to be the largest categories, with private credit and infrastructure investments expanding into sizable asset classes.

Alternative credit has already grown at a 7% CAGR from 2012 through 2022, and we expect it to expand at a 10% to 12% CAGR by 2032. This accelerated pace largely reflects banks issuing fewer loans.

Robust infrastructure growth―at a 16% CAGR over the past decade―will maintain a 13% to 15% CAGR pace over the next decade. Growth here stems from a shortage of public funds as government deficits widen.

Guilty as CHARGED...

It just happened. We weren't planning on an EV but the exact ICE that we wanted wasn't available anywhere. We would have been on a list for months waiting for one with a bench seat for the big dog. So, we drove the EV just to make sure that we were not missing anything. And it was fun. And powerful. And the incentives to take it home that night were unreal. So now I am no longer driving the fastest and most fun car in our garage.

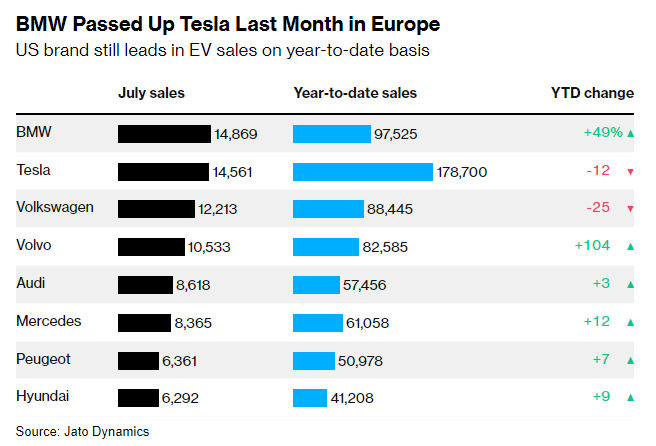

BMW AG pulled ahead of Tesla Inc. and led Europe’s electric-vehicle market for the first time last month, extending the German carmaker’s strong run of growth as other manufacturers struggle.

Sales of fully electric BMWs in the bloc jumped by more than a third to 14,869 units in July, according to data compiled by consultants Jato Dynamics. Tesla’s registrations declined 16% to 14,561 units.

While Tesla still holds a commanding lead in EV sales on a year-to-date basis, it’s ceding market share in Europe to the likes of BMW and Volvo Car AB. European auto buyers registered a total of 139,300 new EVs last month, down about 6% from a year ago.

And gas prices moved to a six-month low last week on my household savings of $2,500 per year...

(@gasbuddy)

How Costco Hacked the American Shopping Psyche...

A great read on one of my long-time favorite companies.

Ostensibly, Costco is a discount store, a place to save money and stretch your grocery dollar, but it is also an aspirational shopping experience, feeding that most American of appetites: conspicuous consumption.

Few companies have greater influence over what we eat (or wear, or fuel our cars with, or use for personal hygiene). Costco dominates multiple categories of the food supply — beef, poultry, organic produce, even fine wine from Bordeaux, which it sells more of than any retailer in the world. It is the arbiter of survival for millions of producers, including more than a million cashew farmers in Africa alone. (Costco sells half the world’s cashews.) Its private label, Kirkland, generates more revenue than towering brands like Nike and Coca-Cola.

For all its success, the company is not well understood. The top brass are insular and secretive. And beyond quarterly reports, Costco rarely discloses anything of its inner workings.

But to Charlie Munger, the billionaire investor and Warren Buffett’s right hand at Berkshire Hathaway, the balance sheet speaks for itself. In one of his last interviews before he died last year, he was succinct: “It is a perfect damn company.”

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: Costco Wholesale Corp.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.