Weekly Research Briefing: The Fed Takes Off

After a year of patience, the Federal Reserve finally mashed their main economic gas pedal into the floor. Seeing inflation on track into their targeted zone of 2%+, the FOMC jumped on assisting the economic part of their dual mandate. By doubling the anticipated Fed Funds rate cut to 50 basis points, the central bank is moving to incent employers into growing and hiring as well as to spur consumer spending activity. In past rate cut cycles, the Fed often had a crisis to deal with causing them to plunge rates lower quickly. This time, the Fed is acting from a position of strength and looking to help the jobs picture before it hits a mud patch on turn four.

The risk markets liked the 0.50% rate cut news and sent equities higher while also tightening credit spreads. Lower rates to help the job picture is good for consumer spending and hopefully will have an outsized impact on large ticket goods (homes, autos and things that take two-plus people to move). Lower rates will also help reduce recession risks which will lower future bank lending and credit quality concerns which is always a big left-tail worry. The steepening yield curve will assist the banking system to build capital which will also help narrow that same downside tail risk.

This will be a record week for Fed speak given last week's move and the efforts to explain their decision. Plenty of old economic data to pick through also as we wait for the new cut to move through future data streams. The big number will be Friday's PCE data which will help indicate how much room the Fed has for future rate cuts. The market is anticipating another near +0.1% m/m core figure. Have a great week.

The Fed went big last week. Here are some key comments from the FOMC statement and press conference to drive home the move...

"The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective."

"This decision reflects our growing confidence that with an appropriate recalibration of our policy stance, strength in the labor market can be maintained."

"We are committed to maintaining our economy’s strength."

“We don’t think we’re behind…. You can take this as a sign of our commitment not to get behind.”

"If the economy evolves as expected, the median participant projects that the appropriate level of the federal funds rate will be 4.4 percent at the end of this year and 3.4 percent at the end of 2025."

Claudia Sahm drives home the importance of the Fed's dual mandate...

Unlike many other central banks, however, the Fed has a mandate for maximum employment along with price stability, and the decision for a larger cut also signals that it is taking seriously recent signs of slowing in the labor market. That’s appropriate. Over the past two months, data has indicated that the labor market was not as strong as the Fed thought. Where things stand is largely fine — the unemployment rate is 4.2 percent, and monthly payroll gains are only somewhat below their strong pace before the pandemic — but the trend is worrisome. The labor market is cooling off.

The increase in the unemployment rate over the past year is in line with increases early in past recessions. While that indicator, the so-called Sahm rule (yes, I came up with it), has accurately forecast prior recessions, it and other economic rules of thumb are too simple for this complicated, post-pandemic time. The United States is not in a recession or even on the verge of one. G.D.P. is on track to grow about 3 percent for the second straight quarter.

Still, a larger rate cut now allows the Fed to reduce the risk. The level of the funds rate was too high given the progress on inflation and the cooling in the labor market. The Fed chair, Jerome Powell, referred to the cut as a “recalibration.”

The Fed's Christopher Waller's comments on Friday almost suggests that inflation is falling too quickly...

"50 bps was the right number; the economy is strong and inflation is coming down."

"I estimate that the August PCE will be very low."

"If you strip out housing services, core PCE would be running under 1% over the past four months."

"CPI and PPI reports flowing into PCE inflation were my considerations."

"In terms of 25 bps vs 50 bps, my speech two weeks ago suggested 25 bps was a good idea, but I was open to 50. The inflation data during the blackout period pushed me toward a 50 bps cut."

"We are at the point where the economy is strong, and we want to keep it that way; 50 bps was the right policy action to achieve that."

"If the labor market worsens and inflation data softens quicker, we could do more."

"We could even pause, depending on the data."

(@wallstengine)

The Fed’s Goolsbee also sees ‘many more’ rate cuts over the next year...

“As we’ve gained confidence that we are on the path back to 2%, it’s appropriate to increase our focus on the other side of the Fed’s mandate — to think about risks to employment,” Goolsbee outlined in talking points for a moderated Q&A event in Chicago Monday. “That likely means many more rate cuts over the next year.”

Goolsbee cautioned that when labor markets deteriorate, they do so more quickly than central bankers can deliver relief through rate cuts.

“It’s just not realistic to wait until problems show up,” he said. “If we want a soft landing, we can’t be behind the curve.”

The Bank of New York CFO explains why this is a very different type of easing cycle...

"And that if you think about it, it's the first time in 30 years where we're probably going into an easing cycle, which is kind of a classic one that for like maybe the economy is softening a bit, and the Federal Reserve just wants to get ahead of it as opposed to the last 30 years, it's been like from 5% to 0 in 24 hours because of bad stuff has happened whether it's 2008, '09, '11, COVID. So this is kind of a different type of easing cycle." – Bank of New York Mellon CFO Dermot McDonogh

Canada is ahead of the US in both inflation falling and central bank rate cutting...

August marked the eighth straight month of headline rates running within the central bank’s target range.

“This is a milestone we’ve all been waiting for,” Andrew DiCapua, senior economist with the Canadian Chamber of Commerce, said in a statement. “With inflation slightly below the Bank of Canada’s expectations, they may now seriously consider cutting rates by a larger amount.”

Annual inflation slowed largely due to gasoline — gas prices fell outright and were also impacted by base effects, Statistics Canada said.

Prices declined in five of eight subsectors on a monthly basis, which could trigger worries about deflation among central bank officials if it becomes a trend. Macklem has recently said the bank cares as much about undershooting the 2% inflation target as it does overshooting it.

The Bank of Canada has already cut rates three times since June, bringing the benchmark overnight rate to 4.25%, and officials have signaled more to come. Economists see mounting weakness in the labor market, and some of them are calling on policymakers to start making bigger moves to bring down borrowing costs.

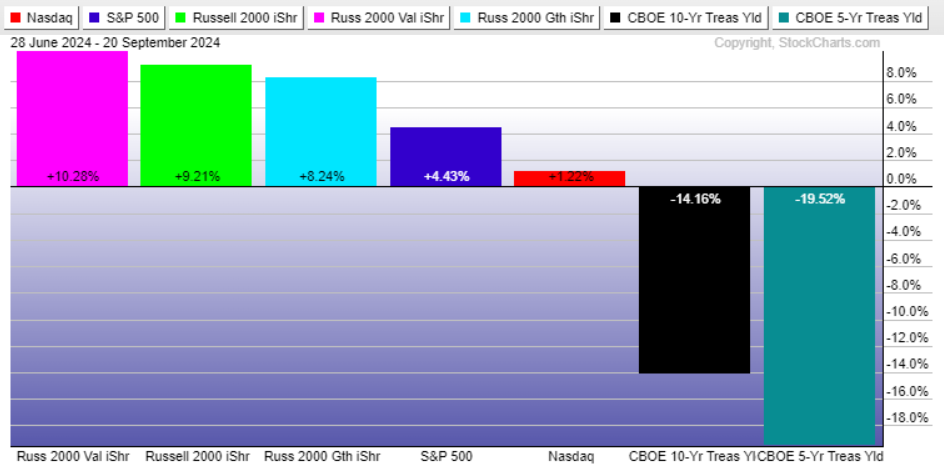

Small caps have outperformed in this Q3 as the Fed moved closer to their first rate cut...

As seen below, five and ten year yields have really collapsed the last three months as the market became convinced that the Fed would begin cutting rates. Since that time, the market leading Nasdaq has handed the performance baton to the smallest companies. And small caps positive reaction since Wednesday's news should be incremental positive news that this is an area where market investors want to be positioned. Interesting to note that the market wants anything small cap and is less concerned about growth or value.

(StockCharts)

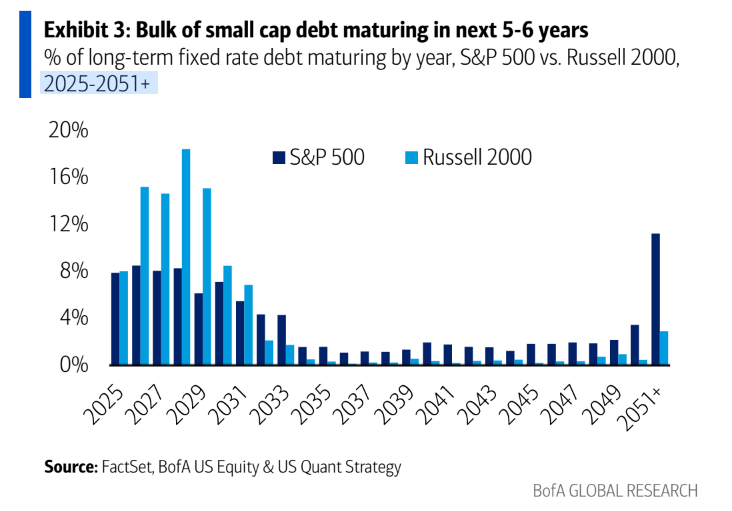

Falling rates and positive credit environments are a positive for small cap companies needing to refinance...

Small cap liabilities tend to be front end loaded to maturities happening in the next five years versus large cap companies who are able to spread their liabilities out over future decades.

@MikeZaccardi

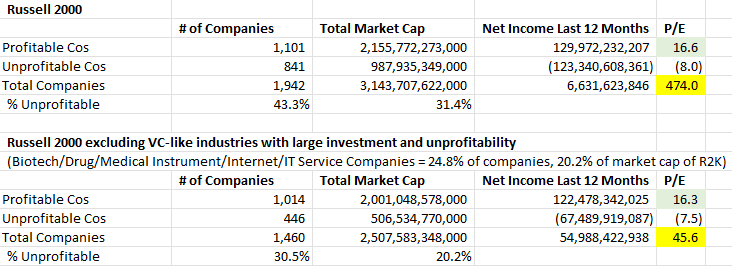

With the increased focus on small caps, I reran the trailing valuation metrics for the Russell 2000 index thru last week's earnings...

The all-together trailing P/E amounts continue to grow to be a ridiculous 474x earnings. But stripping out the most venture capital like sub-sectors like biotech and internet service companies, pulls the trailing multiple down to 45.6x. And if you toss out all the money losing companies, the trailing P/E falls to 16x. This compares to about 24.5x the S&P 500 trailing P/E.

(Barchart)

The market tends to applaud Fed easing when done from a position of strength...

@wallstengine: JPMorgan: "Over the past 40 years, the U.S. Fed has cut rates 12 times when the S&P 500 $SPY was within 1% of an all-time high. The market was higher a year later all 12 times, with an average return of around 15%."

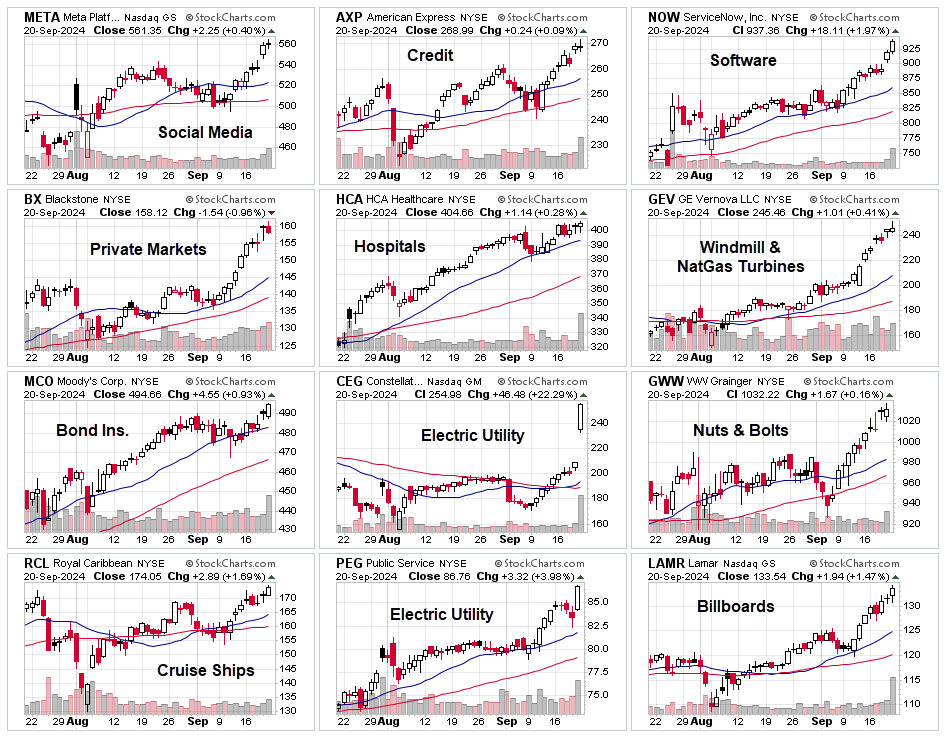

The S&P 500 performance has broadened out...

@KevRGordon: Both the cap-weighted and equal-weighted S&P 500 indexes are at new all-time highs

A look at some of last week's new all-time highs shows just how many different companies are participating...

Your "AI is an existential need for all businesses" quote of the week...

"It's driving new levels of productivity that haven't been seen since probably the industrial revolution. There's not many gifts of 20% and 30% productivity that I can think of is certainly in my working lifetime. And as a result, this is a conversation every boardroom. It's going to change the basis and is changing the basis of competition. And if you don't have a strategy here, it's an existential threat. You will be out of business. That's why this is different." – Dell Technologies Vice Chairman and COO Jeff Clarke

For those that do believe, the capital needs of building AI are massive. Here is one way to raise $100 billion to build it...

BlackRock is preparing to launch a more than $30bn artificial intelligence investment fund with technology giant Microsoft to build data centres and energy projects to meet growing demands stemming from AI.

The financial partnership, which BlackRock is launching with its new infrastructure investment unit, Global Infrastructure Partners, would be one of the biggest investment vehicles ever raised on Wall Street. Microsoft and MGX, the Abu Dhabi-backed investment company, are general partners in the fund. Nvidia, the fast-growing chipmaker, will advise on factory design and integration.

The investment vehicle is aimed at addressing the staggering power and digital infrastructure demands of building AI products that are expected to face severe capacity bottlenecks in coming years. The computing power of AI requires far more energy than previous technological innovations and has strained existing energy infrastructure.

Dubbed the Global AI Investment Partnership, the effort seeks to raise up to $30bn in equity investments and leverage to support up to an additional $70bn in debt financing.

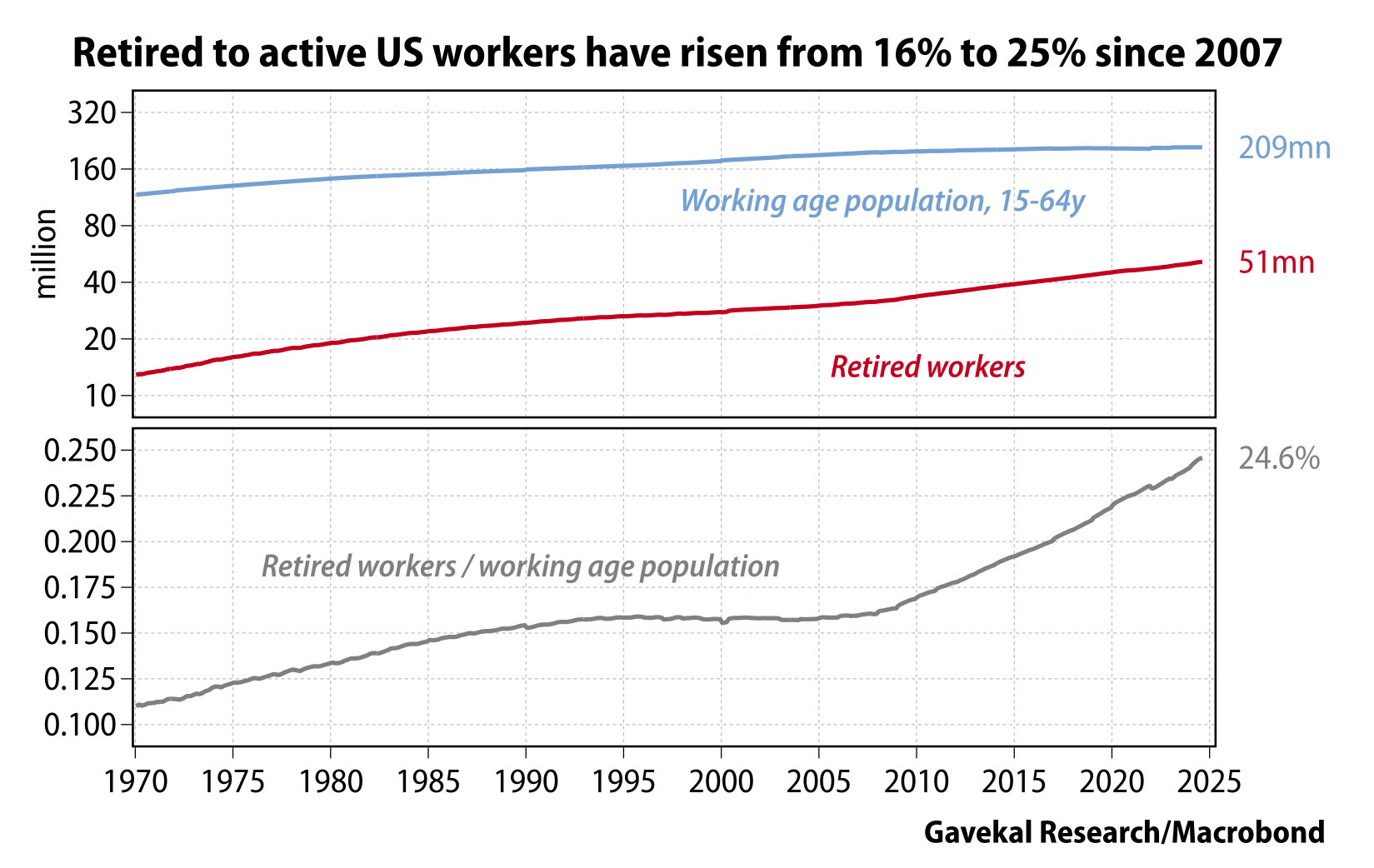

I think Scott Galloway did a TED talk that addressed this...

In other words, 9 workers for each retiree in 1970. Today the math is 4 workers for each retiree.

(@Gavekal)

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.