Weekly Research Briefing: The Market's Drums Beat Louder

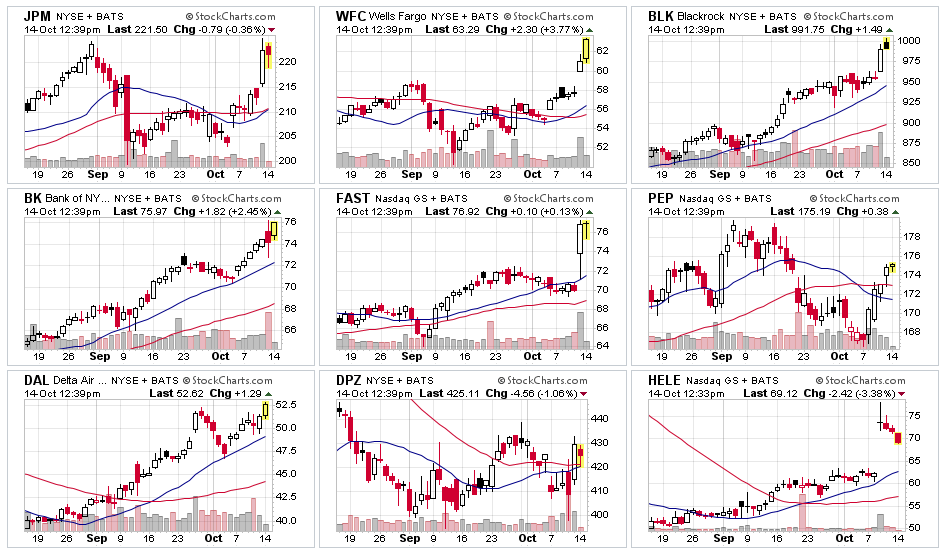

The good news for financial risk taking grew louder last week as better than expected earnings, a pickup in M&A activity, and the successful launch of several IPOs hit the market. While it was only week one of the Q3 earning season, most all of the reporting names have a higher stock price today than before the report. The big banks delivered as did Delta Airlines and Pepsi. Even Fastenal who posted a marginally better quarter along with their always conservative tone gained fans sending its shares 10% higher. The market is a healthy one when you can get paid in both earnings beats and earnings non-beats. Maybe the earnings bar was just set too low at only a +4-6% y/y growth rate? We know that the economic data outlook was very negative going into September's FOMC meeting. It is easy to see where Q3 earnings estimates could have been influenced by the negativity, so maybe beats will continue to be plentiful as the reporting season continues.

Meanwhile, merger and acquisition activity and IPO filings are now flooding my news tape. It looks like buyers and sellers have finally come together on prices and deals are being struck. This should result in a growing wave of cash liquidity going back to public and private equity shareholders. The IPO markets have also opened up rewarding recent sellers and even IPO buyers to strong gains. At the same time, credit spreads have continued to collapse giving companies one more reason to borrow near all time low credit spreads for whatever purpose they might have for the new funds.

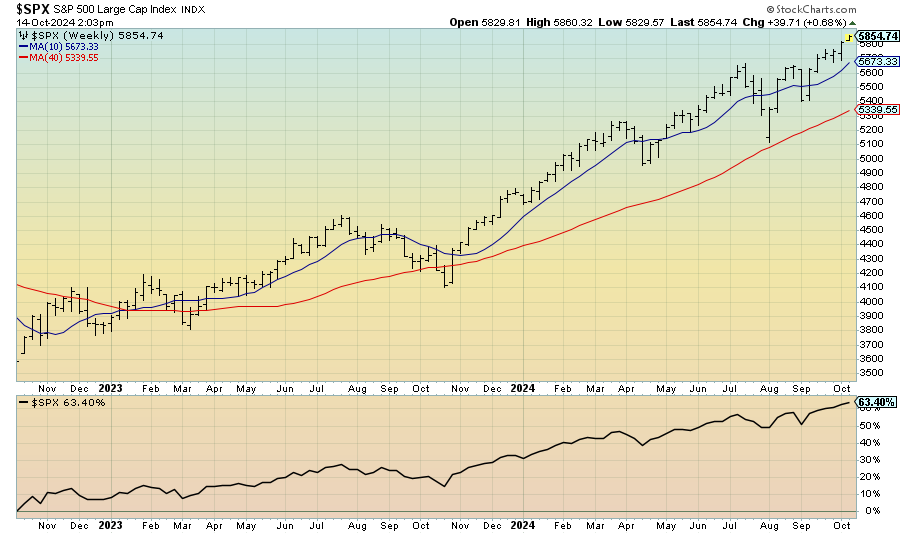

The equity bull market turned two-years old over the weekend and now sports a +64% gain over its run. The S&P 500 VIX sees a potential speed bump in three weeks, but besides the election and the ongoing geopolitical concerns, the news flow looks to be positive for risk taking. Last week's core CPI was a bit warm at +0.31% m/m for September, but the good news was the big slowdown in the shelter inflation component to +0.2% m/m. This week will be mostly about earnings but with a healthy dose of economic data from the retail, manufacturing and housing sectors. Enjoy the charts and have a great week.

Now this was a good way to start off the Q3 earning season...

No clunkers here. Stocks all higher today than they were before the numbers.

(StockCharts)

This week we have a very expanded list of reporting companies from many more industries...

(eWhispers)

The bull market turns 2-years old...

Congrats to everyone who bought the 50-day over 200-day crossover.

(StockCharts)

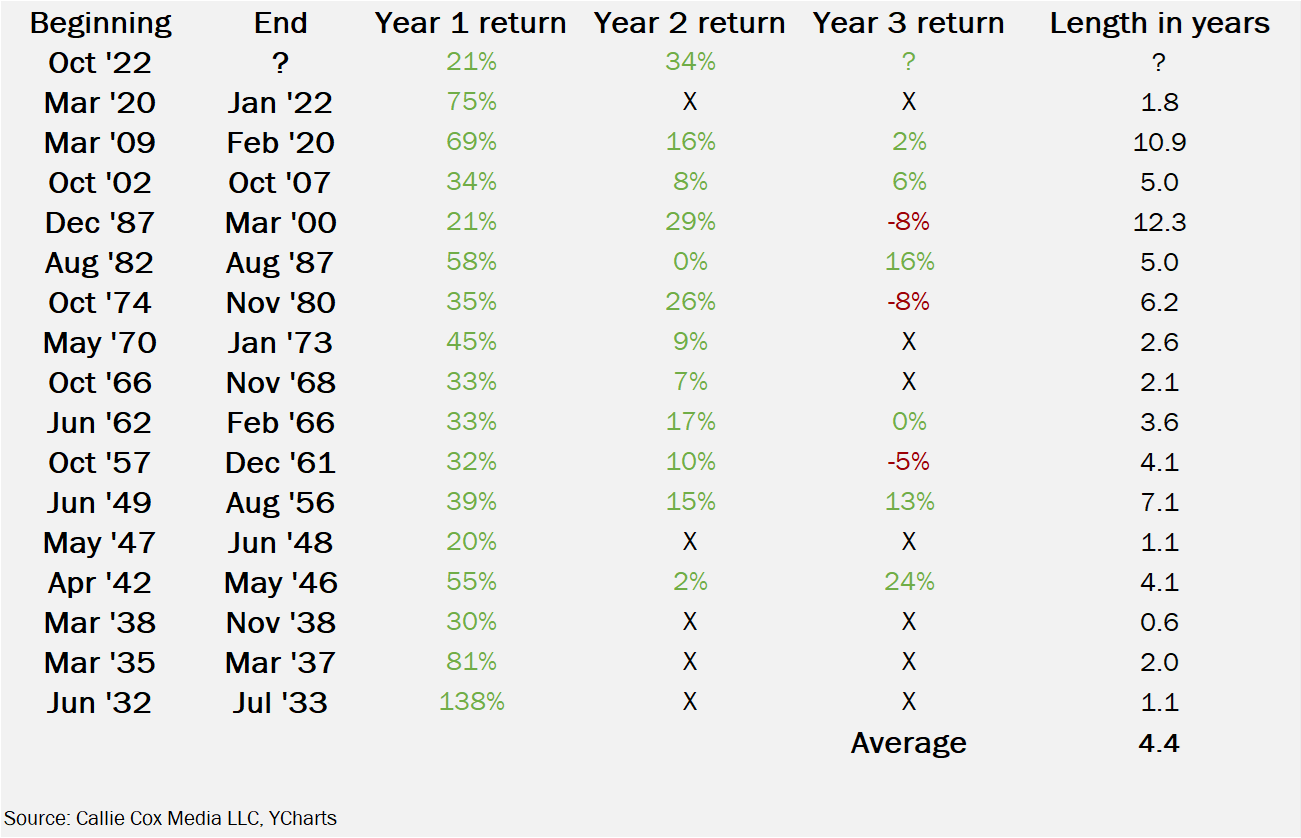

If you want to know how long the average bull market lasts....

@callieabost: Happy birthday to the bull market. This bull market began two years ago in the midst of 8% inflation. It grew despite a chorus of recession calls. Two years and a 63% rally later, it's finally getting a chance to breathe through lower rates. Here's to year 3.

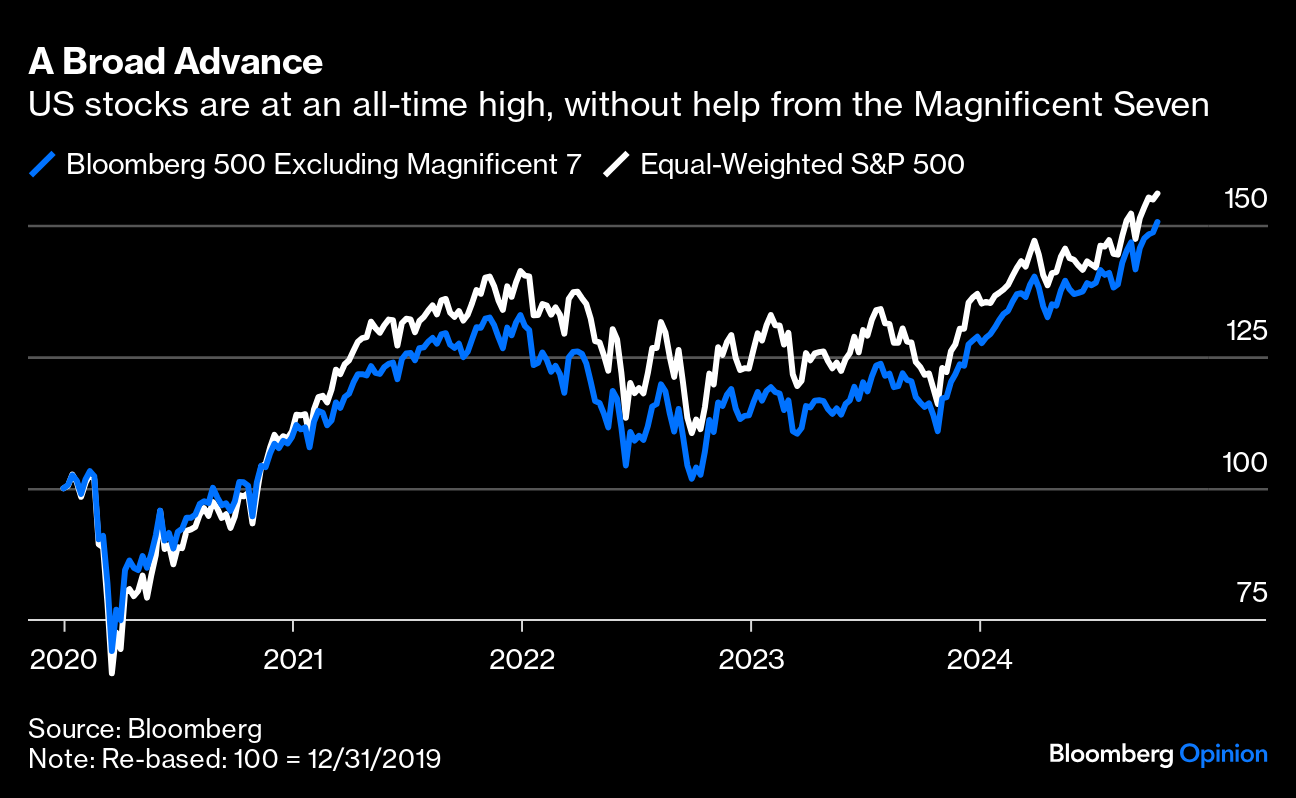

Best part about the current market is that it is no longer just about the Mag-7...

The S&P 500 finished last week at yet another all-time high. It did this without relying on the Magnificent Seven tech platform companies. Take the equal-weighted version of the S&P 500, in which every company counts for 0.2% regardless of their size, or Bloomberg’s index of the “other 493” large-cap stocks excluding the Mag 7 altogether, and the market is at a record.

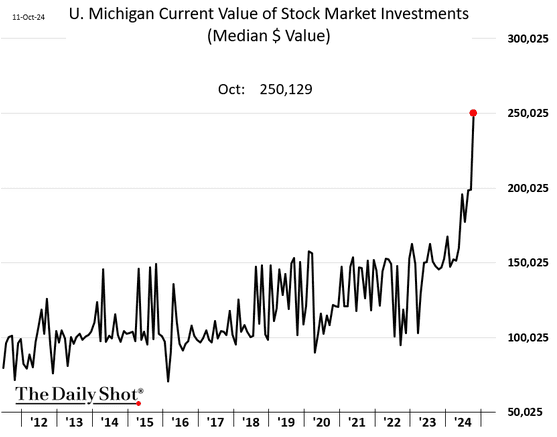

The median value of US households’ stock portfolios surged to $250k this month...

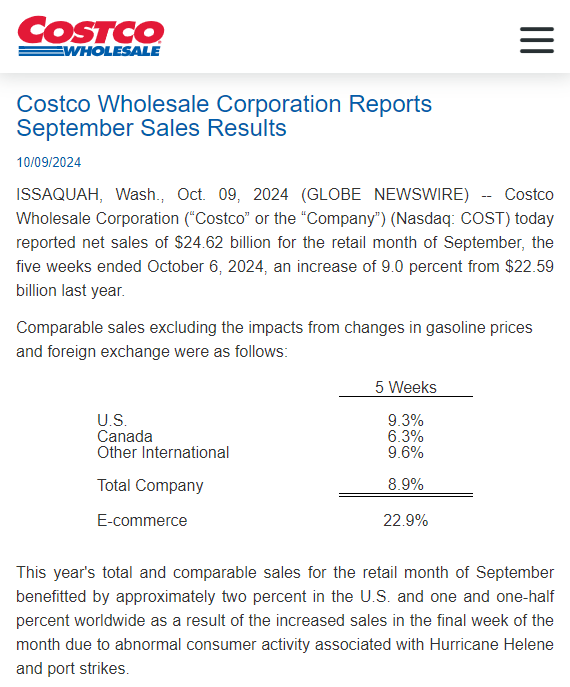

And now for a look at one of the better reads on the health of the U.S. consumer...

One has to believe that Costco comps are getting help from rising stock values, in addition to wage growth and gains in home equity.

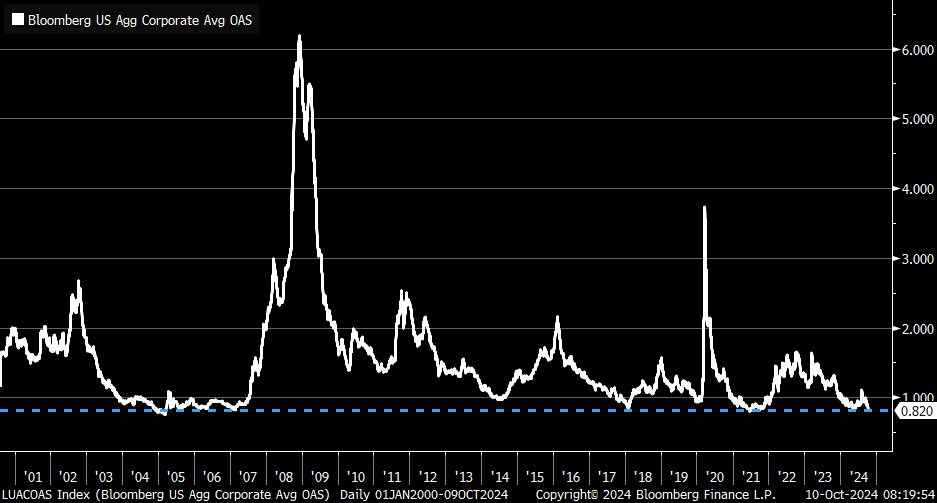

Can we get a round of applause to all CFO's issuing debt this month...

@KevRGordon: IG spreads back at their lowest since September 2021... if you go look to before the June 2021 low, they're back to where they were in February 2007.

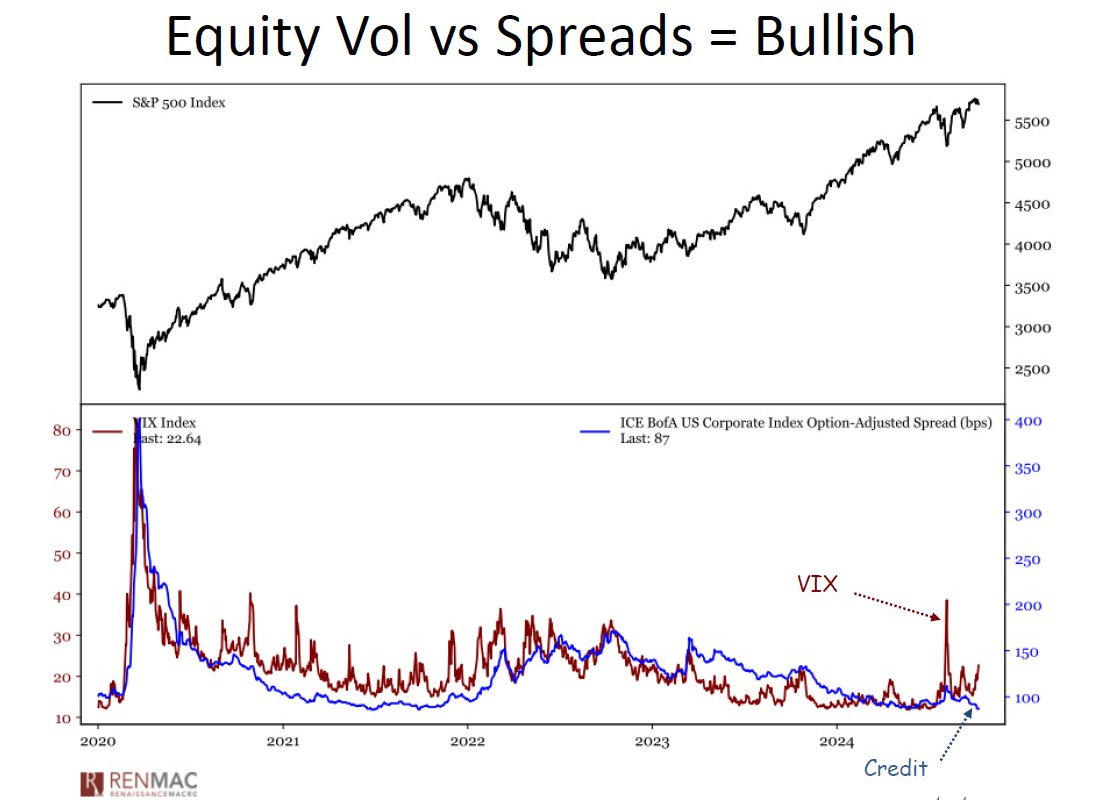

Remember that the Credit markets are the smart money. Ignore the 20-handle on the VIX for the S&P 500...

@RenMacLLC: $VIX vs Credit is set-up bullishly for $SPX. Basically, equities are pricing in risk (vol) that the credit markets are not bothered about. There's more math to it than what you see here, but it's extreme enough to provide a bullish back-drop for Q4.

Now for a small slice of M&A action: a Russell 2000 neurological biotech company is acquired by Germany's Lundbeck...

H. Lundbeck A/S agreed to acquire Longboard Pharmaceuticals Inc in a $2.6 billion deal that boosts its drug pipeline for serious brain diseases.

The Danish pharmaceutical company is offering shareholders $60 per share in cash for US-based Longboard, in a transaction that has been unanimously approved by the boards of both companies, according to a statement.

Shares of Lundbeck fell as much as 5.9% following the news. Longboard Pharmaceuticals rose as much as 52% to hit a record high at the New York market open.

Lundbeck specializes in treatments for serious brain diseases and its proposed acquisition of Longboard will boost its development pipeline in rare neurological conditions. Longboard’s main asset is bexicaserin, a potential blockbuster treatment for patients suffering from rare and severe epilepsies, for which there are currently very few good treatments available.

Circle K is making a bigger run at 7-Eleven...

TOKYO -- Canadian convenience store operator Alimentation Couche-Tard has made a new takeover offer to Japanese retailer Seven & i Holdings that raises the valuation by more than 20% compared with its previous offer, people with knowledge of the deal told Nikkei.

The proposed all-share buyout would be worth $47 billion, up from an earlier offer of $38.5 billion. If the deal goes through, it would be the largest acquisition of a Japanese company by a foreign one. The new offer is $18.19 per share, about 20% higher than Seven & i's closing price of 2,230 yen ($15.03) on the Tokyo Stock Exchange on Tuesday. Couche-Tard had proposed to buy all Seven's shares for $14.86 per share in cash in July.

A large cap, go private healthcare deal proposed over the weekend...

Private equity groups TPG and Blackstone have teamed up to work on a joint bid for eyecare company Bausch + Lomb, according to people familiar with the matter.

If it goes through, the deal could be one of the largest private equity buyouts of the year, with Bausch Lomb’s enterprise value including debt totalling $11.5bn as of market close on Friday. Several other private equity funds assessing bids have dropped out of the process.

Bausch + Lomb was put up for sale to resolve an impasse over a separation from its heavily indebted parent company.

TPG and Blackstone have long been considered the frontrunners to take the business private, as before Bausch + Lomb publicly listed in 2022 the private equity groups had expressed interest in buying the business, the people added. TPG already owns ophthalmology company BVI Medical.

People familiar with the bidding said offers were expected to value the company at an enterprise value of between $13bn and $14bn, or up to $25 per share.

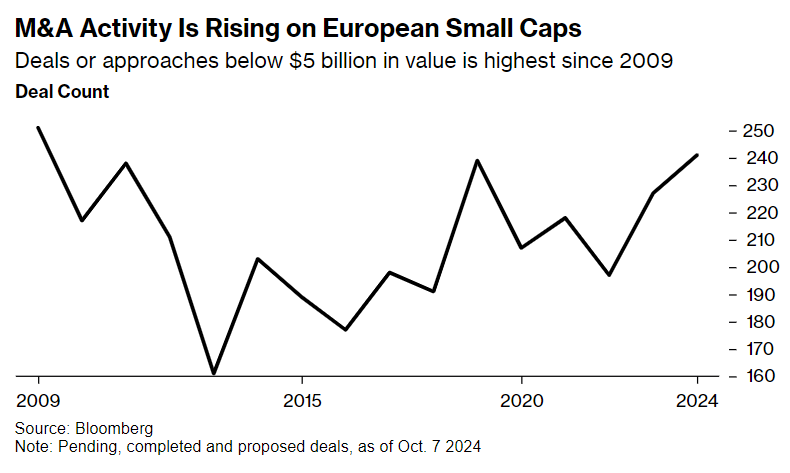

European small cap valuations have just become too attractive for acquirers...

Falling interest rates and a pick-up in mergers and acquisitions are proving to be a winning combination for Europe’s struggling small- and mid-cap market.

M&A activity for deals below $5 billion has rebounded after three years of underperformance versus blue chips, according to data compiled by Bloomberg. With 240 deals proposed, pending or completed this year, the total is already the highest since 2009.

The surge in M&A is backed by valuations. After years of underperformance, small and mid-caps in Europe trade at price-to-forward earnings levels relative to big caps unseen since the global financial crisis. Historically, the cohort has traded at a premium due to its potential for stronger growth, but for most of the past year it’s been at a discount.

“These companies are trading so low that they are attracting interest from both private equity and trade buyers,” said Hywel Franklin, head of European equities and who manages a European small cap fund at Mirabaud Asset Management.

This private to public medical device maker IPO is now trading above $25 for a market cap of $900 million...

TPG-backed CeriBell is targeting as much as $578.3 million valuation in its upsized initial public offering in the United States, the medical device maker said on Wednesday, indicating robust investor optimism for healthcare startups. September was the busiest month for healthcare IPOs this year, Dealogic data showed. The momentum has spilled into October, with three companies from the industry, including CeriBell, set to go public in the coming days.

Recent strong debuts by weight-loss drug developer BioAge Labs and TPG-backed cancer therapy developer Bicara Therapeutics among others, have also bolstered investor confidence in the sector and encouraged listings among other IPO candidates. CeriBell, backed by alternative asset manager TPG's The Rise Fund, is now aiming to raise as much as $180.3 million by offering about 10.6 million shares at $16 to $17 each.

The Sunnyvale, California-based company had earlier planned to sell 6.7 million shares priced between $14 and $16 each. Founded in 2014 as Brain Stethoscope, CeriBell makes artificial intelligence-powered brain monitoring system to detect neurological conditions.

And Upstream Bio jumps nearly 30% to a $1.1 billion market cap after its IPO pricing...

Boston, USA-based Upstream Bio (Nasdaq: UPB), a biotech developing treatments for inflammatory diseases with an initial focus on severe respiratory disorders, has made an impressive start to life as a public-listed company.

Shares in the firm opened 26.5% above the initial public offering price in its Nasdaq debut on Friday, valuing the drug developer at $1.05 billion. Upstream raised $255 million by selling 15 million shares, 20% more than initially planned, at the top end of its marketed range of $15 and $17 each.

By the end of Friday's trading in New York, shares in Upstream were more than 29% higher.

After missing the IPO window in 2021, KinderCare found plenty of buyers to push it toward a successful public launch and a $3.3b market cap last week...

KinderCare Learning Cos. shares rose nearly 9% after the company raised $576 million in an initial public offering priced toward the bottom of a marketed range.

The Partners Group Holding AG-backed childhood education company’s shares closed at $26.13 each on Wednesday in New York, above their IPO price of $24 apiece.

The trading gives KinderCare a market value of about $3 billion, based on the outstanding shares listed in an earlier filing.

The share sale comes as US IPOs look to return to the pace set in the decade before the pandemic. Some $36.3 billion has been raised via first-time share sales on US exchanges this year, according to data compiled by Bloomberg. That’s about a 64% jump from the same period last year, but still well below the average for 2010 to 2019, data compiled by Bloomberg show.

Speaking of private companies: America’s New Millionaire Class: Plumbers and HVAC Entrepreneurs...

For years, Rice, 43 years old, was skeptical when out-of-state investors offered to buy his company. He assumed most of them knew little about skilled-trade work or his customers. They were just looking to make a buck. But in 2022, when approached by a local HVAC company backed by private equity, he changed his mind, figuring that they knew the business.

“The trades are hard work. A lot of today’s society, picking up a shovel is foreign to them,” he says.

Private equity, however, is no foreign player in the skilled trades these days. PE firms across the country have been scooping up home services like HVAC—that is, heating, ventilation and air conditioning—as well as plumbing and electrical companies. They hope to profit by running larger, more profitable operations.

Their growth marks a major shift, taking home-services firms away from family operators by offering mom-and-pop shops seven-figure and eight-figure paydays. It is a contrast from previous generations, when more owners handed companies down to their children or employees.

The wave of investment is minting a new class of millionaires across the country, one that small-business owners say is helping add more shine to working with a tool belt.

"What if private is both safe and risky and public is safe and risky?”

According to Apollo, the world’s largest 200 pension plans have an average 22% allocation to fixed income and a 1% allocation to private credit. Although fixed income provides liquidity not available in private credit, it comes at the expense of lower returns. At BBB credit ratings, Apollo reckons it can squeeze out a 7.8% total return from its origination ecosystem compared with 5.9% Bloomberg benchmark for Baa US corporates. “You have to go from daily to monthly liquidity, but you pick up close to 200 basis points of yield,” says John Zito, Apollo’s Deputy Chief Investment Officer of Credit.

In any event, Apollo reckons that daily liquidity is overrated. Long-term holders of capital catering to prospective retirees don’t need it and even when they do, it’s not always available. A distinct feature of the post financial crisis marketplace is that banks that previously provided market making capacity to create liquidity have retrenched. Primary dealer inventory of corporate bonds has fallen by around 90% at the same time as the total stock of US corporate bonds outstanding has grown three times...

[Apollo CEO Marc] Rowan reflects: “For those of us who have been in the business 40 years, we have it beaten into our head that private is risky and public is safe. We know that in our bones… But what if we're wrong?… What if private is both safe and risky and public is safe and risky?”

The demand to own HPS should tell you something about the interest of the largest players to expand in private credit and where the business is headed...

A potential bidding war for HPS Investment Partners is set to swell the fortunes of its three founders as rival groups vie for a piece of the red-hot private credit market.

HPS has been weighing the possibility of an initial public offering that may value it at $10 billion or more, and several suitors have considered an investment or acquisition that could yield an even higher payout for the firm’s founders. Those suitors include BlackRock Inc., Abu Dhabi-based asset manager Lunate and private equity firm CVC Capital Partners...

HPS now represents an acquisition target that could launch other asset managers into the top rungs of private credit, or another way for investors to bet on an industry that its backers say is still in the early innings of potentially explosive growth. The share prices of Apollo Global Management Inc. and Ares Management Corp., both big players in private credit, have each more than doubled since the start of last year.

The interest from several potential bidders — including the world’s largest asset manager, BlackRock — validates the HPS founders’ bet on private credit. In 2016, HPS bought itself out of JPMorgan Chase & Co. in a deal that valued it at almost $1 billion. Assets under management have more than tripled since — to $117 billion as of June.

Finally, Amazon is going to drive a truck over the drugstore industry.

It seems like a decade ago that Amazon made its first news into the business. It took a long time, but now that they have same day delivery to half of America, the drug and grocery store pharmacy business should disappear.

Amazon Pharmacy plans to open pharmacies in 20 new cities across the U.S. in 2025, more than doubling the number of cities where customers can get Same-Day Delivery of their medications. Amazon is leveraging its vast logistics network and advanced automation technology to solve one of pharmacy’s biggest pain points: the lack of convenient, affordable access to medications...

Amazon Pharmacy customers already receive their medications in two days or less on average. By the end of 2025, nearly half (45%) of U.S. customers are expected to be eligible for Same-Day of their prescription medications. In most cases, that means a customer can order medication by 4 p.m. and receive it at home by 10 p.m.

As “pharmacy deserts” grow, digital-first pharmacies like Amazon offer a solution to care gaps. A recent study found nearly half of U.S. counties have communities over 10 miles from the nearest pharmacy, limiting their access to medications and pharmacist care. Traditional mail-order prescriptions can take up to 10 days to arrive, leaving many underserved. Rapid delivery of medications and 24/7 access to a pharmacist ensures customers can get care within hours, bridging health care accessibility divides.

Michael Lewis writes another gem. This time, about a lump of coal...

For reasons he could never fully explain, even to himself, he loved being inside a coal mine. “It was just so cool,” he said. “You go down into a place most people think you are crazy to be. And you like it.” But a year into the job, his enthusiasm for the actual work flagged. He didn’t really belong in West Virginia. Everyone knew everyone else, and he knew no one. “It was like being an immigrant,” he said. “You could be there your entire life and never fit in.” Partly out of stubborn pride, he refused to even consider heading home. He enrolled in Penn State instead, to study mining engineering.

His mother had left him some money. His father, mollified that his son had returned to college, chipped in a bit more. And Chris would help pay for his education — by moonlighting inside coal mines as he studied.

His political interest in workers’ rights was morphing into a technical interest in their safety. Coal mining had long been the most dangerous job in the United States. At the height of the Vietnam War, a coal miner was nearly as likely to be killed on the job as an American soldier in uniform was to die in combat, and far more likely to be injured. (And that didn’t include some massive number of deaths that would one day follow from black lung disease.) Up to that point in the 20th century, half of the coal miners who had died on the job — roughly 50,000 people — had been killed by falling roofs. In his classes at Penn State, Chris saw at least one reason for that: The coal mining industry had learned to see the problem as the cost of doing business.

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The author has current equity ownership in: J.P. Morgan Chase & Co., Costco Wholesale Corp. and Amazon.com Inc.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.