Weekly Research Briefing: Watching More Closely

Mr. Market would like to apologize for hard kicking your beach chair while you were in a deep slumber. Cutting the Fed Funds rate by 25 basis points last week would have been the easy thing to do. Instead, the Fed has decided to attempt a barrel roll before landing our economic airplane. Last week's weaker than expected jobs and ISM manufacturing data have now increased the market's thoughts of a future recession. That choice is not at the top of the menu, but it is down in the side dish section which means that we must still pay attention to it. Not something that you wanted during your August recess.

The Fed's lack of action on Wednesday cost them the central banking gold medal. Now the U.S. central bank will have to work hard in August and September just to get on the podium. Next up for the Fed is Jackson Hole the third week of August followed by hopes of a bigger rate cut in September. The rude awakening from such a deep sleep helped cause the worst two-day decline in Japan equities history (-18%), the Nasdaq to move into a -10% correction territory and even the Russell 2000 to give up all of its gains for 2024. The S&P 500 volatility index (VIX) even jumped to a high of 65.7 placing it among the top 3 percentage jumps of all-time before retreating back near 38.

So where is the good news? Well, most U.S. Treasury yields are now 40-60 basis points lower than a month ago pulling the 30-year mortgage rate down near 6.3%. The credit markets remain stable which is good, but also unusual given the craziness in equity volatility. VIX spikes over 30 typically create good buying opportunities as past spikes have shown. Monday's ISM services figure was strong where last week's manufacturing number was weak and as you recall, services make up 70%+ of U.S. GDP. The economy and businesses will continue to grow, but just like before, at a slower rate. The Fed has been given a yellow card by the markets and now it is time to see how they will react. They have plenty of firepower to lower rates and help businesses and consumers navigate this slowdown. I can't think that they will give the markets any reason to reach for its red card. Score the goal and grab the medal Jerome.

The Fed sets the table for a September rate cut...

But such a missed opportunity to cut by 25 bps last week!

"The job is not done on inflation, but nonetheless, we can afford to begin to dial back the restriction in our policy rate...a reduction in our policy rate could be on the table as soon as the next meeting in September." - US Federal Reserve Chair Jerome Powell

The Fed's Goolsbee was first to the mic today and he tried his best to show how good a position they are in to help any future economic weakness...

"As you see jobs numbers come in weaker than expected but not looking yet like recession, I do think you want to be forward looking of where the economy is headed for making the decisions,” Goolsbee said on CNBC Monday.

“If we blow through normal, then we’re in a different situation and we would, in my opinion, we would need to react more robustly,” he said...

“The Fed’s job is very straightforward, maximize employment, stabilize prices and maintain financial stability,” Goolsbee said. “So if the conditions collectively start coming in that on the through line, there’s deterioration on any of those parts, we’re going to fix it.”

Now the market's consensus thought?

The central bank’s job is risk management. It’s why policymakers continued to increase interest rates in the first half of 2023 well over a year after their preferred measure of inflation had peaked and begun to decline. In June, the Fed’s “dot plot” — an anonymous collection of policymakers’ rate expectations — showed a median projection for a 25-basis-point cut in 2024 followed by four more reductions in 2025, or 1.25 percentage points of easing overall. Both the labor market and inflation data have weakened since then. A revised dot plot today would likely show more aggressive cuts, and we know from Chair Jerome Powell’s comments on Wednesday that policymakers are prepared to lower rates in September.

So why wait? Inflation risks have moderated sufficiently, so the main argument against cutting more aggressively than they’ve previously signaled would be the risk that markets are alarmed by what that says about the economic outlook. Fortunately, Powell can use his upcoming speech at the Kansas City Fed’s conference in Jackson Hole, Wyoming, to shape the narrative.

Swift rate cuts would relieve pressure for Americans struggling to make payments on floating-rate credit card debt or to get financing for a new car. It would help the millions of homeowners who bought when mortgage rates were high, with refinancing at lower rates freeing up household budgets for other types of consumption. The main headwind for the economy right now is high borrowing costs.

Neil Dutta agrees that the Fed can correct their mistake quickly...

@RenMacLLC: Because the Fed failed to move yesterday, the ongoing deterioration in the economic data as evidenced by today’s rising initial jobless claims, Low unit labor costs, and abrupt slowing in global manufacturing activity suggest that we are getting close to a point where bad economic news is bad for markets. Until the Fed begins cutting, they are going to look behind the curve. In my view, the upshot is that this is a small policy mistake that can be undone very quickly.

Former White House economist agrees that the Fed should have cut last week...

@ernietedeschi: The Fed shouldn't panic. The US isn't in recession now. This isn't even close to March 2020. My god, prime-age participation hit a new post-2001 high in this report. But on balance it's clearer the Fed should have cut in July, so the Fed should rectify that mistake in September.

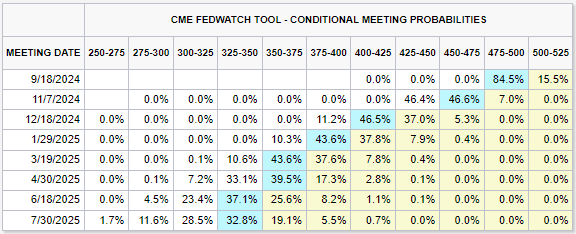

The markets now see a 84.5% chance of a 0.5% Fed Funds rate cut at the September meeting...

Followed by a 25-50 bp rate cut in November and a further cut in December. Lots of ammo, but now the question is when will the FOMC use it?

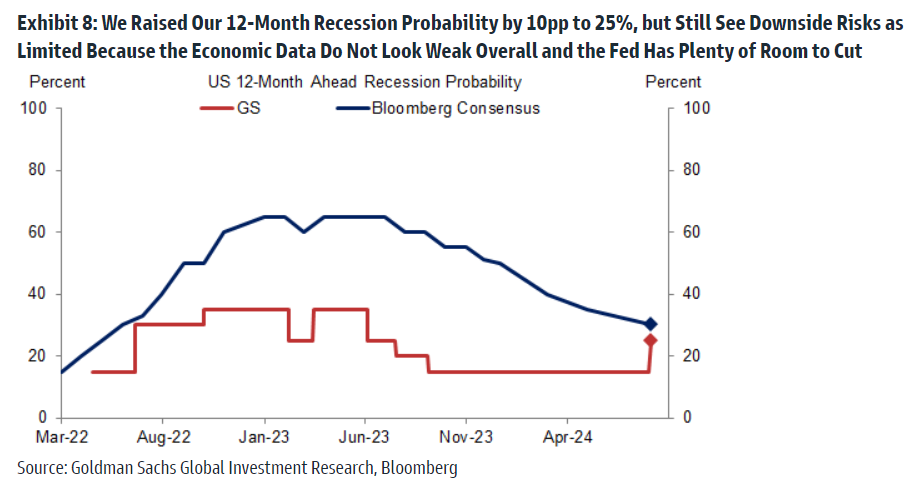

Goldman Sachs sends a small warning note to the Fed...

We have increased our 12-month recession odds by 10pp to 25%. While we now think the risks are somewhat higher than the historical unconditional average 12-month probability of about 15%, we continue to see recession risk as limited because the data still look fine overall and we do not see major financial imbalances.

We also take reassurance from the fact that—as Chair Powell emphasized last week—the Fed has 525bp of room to cut the funds rate and will surely be quick to support the economy if necessary. While some of the factors that dampened the impact of rate hikes might also dampen the impact of rate cuts, this should be plenty of room to solve what looks like an at most moderate problem so far.

Goldman Sachs

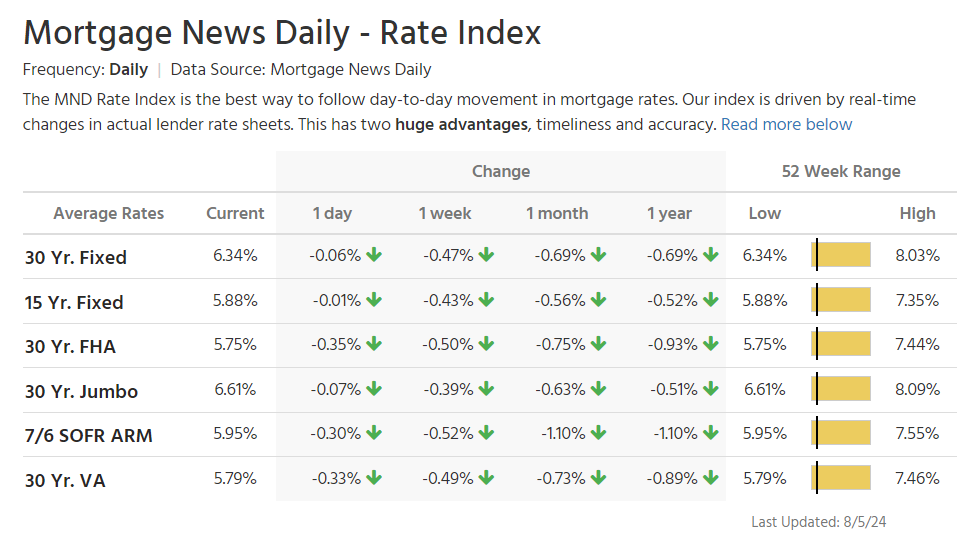

The housing construction and mortgage industry smiles begin to break wider...

Lowest mortgage rates in 16 months and down 40-50 bps in one week will give a lift to future residential housing activity. How long until someone begins to calculate how much the U.S. Government will begin to save on interest expense from the collapse in yields?

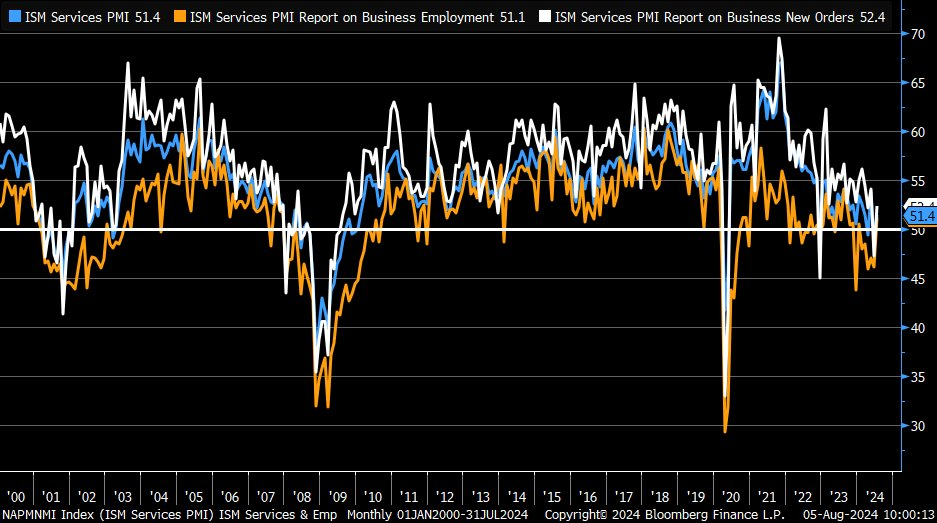

Monday's ISM services index was strong across the board which does not hint of a recession...

The ISM services index increased by 2.6pt to 51.4, slightly above consensus expectations for a more moderate increase. The underlying composition was strong, as the business activity (+4.9pt to 54.5), new orders (+5.1pt to 52.4), and employment (+5.0pt to 51.1) components all increased back to expansionary territory. The supplier deliveries component decreased by 4.6pt to 47.6 (nsa) and the new export orders index increased by 6.8pt to 58.5 (nsa). The prices paid measure increased by 0.7pt to 57.0 (sa).

Goldman Sachs

@KevRGordon

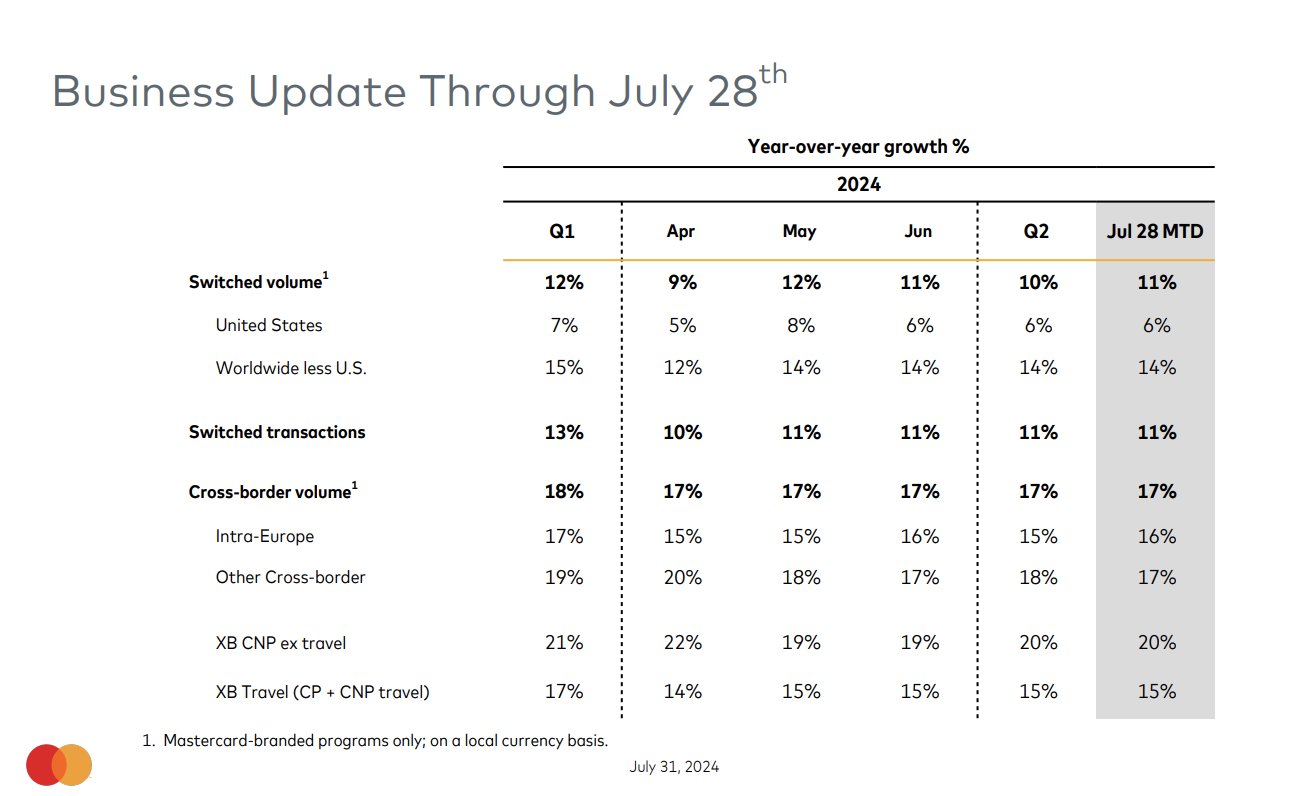

And no imminent recession seen in last week's Mastercard spending volume details...

@TheTranscript_: $MA CFO: " In terms of the trends we've seen for the first 4 weeks of July, like I said, look, I mean, general stability and drivers across the board."

Other consumer earnings tidbits show caution but also continued spending...

"We're seeing lower average selling prices or ASPs right now because customers continue to trade down on price when they can... Consumers being careful with their spend, trading down, looking for lower ASP products, looking for deals...That continued into Q2, and we expect it to continue into Q3. We're seeing signs of it continuing in Q3." - Amazon CFO Brian T. Olsavsky

"There's some cautious folks out there on the spend side. The good news for us is people are prioritizing getting on vacation. We're seeing that in our resort occupancies at 90-plus percent." - Marriott Vacations Worldwide Corporation CEO John Geller

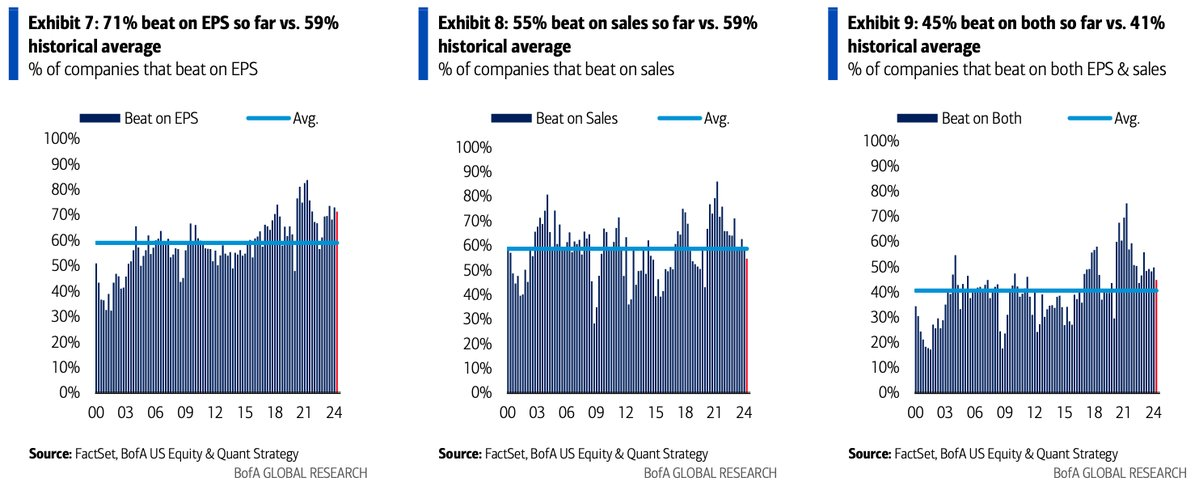

With the bulk of the S&P 500 earning season wrapped up, the Q2/2024 wasn't a bad one...

@dailychartbook: "71%/55%/45% beat on EPS/sales/both, worse than last quarter (73%/59%/50%)." - BofA Savita

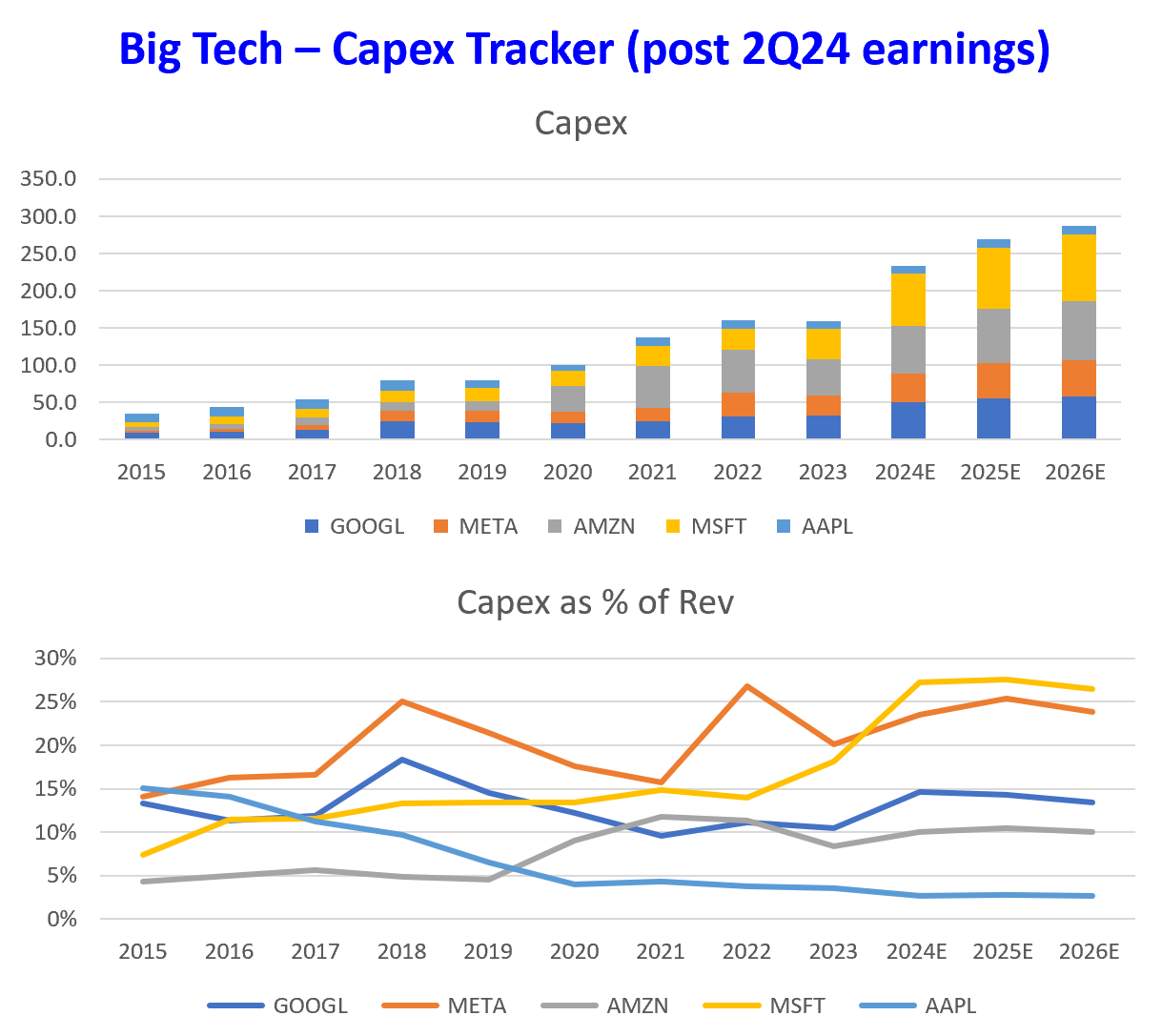

Plenty of focus on AI spending and how it runs through the economy...

Here are some good details as I know many of you are watching this closely across multiple sectors.

"At this point, I'd rather risk building capacity before it is needed rather than too late, given the long lead times for spinning up new infra projects. And as we scale these investments, we're, of course, going to remain committed to operational efficiency across the company." - Meta Platforms CEO Mark Zuckerberg

"I think the overall view on AI investment is we have to invest. I mean, the industry has to invest. The potential of AI is so large to impact the way enterprises operate and all that stuff. So I think the investment cycle will continue to be strong." - Advanced Micro Devices CEO Lisa Su

"We're not observing anything slowing down. And in fact, as you can see by the numbers and your commentary relative to what we talked about 12 months ago during the IPO, it's probably picked up." - Arm CEO Rene Haas

"When you think about the growth that we're seeing today in our data center business, and you think about the growth projections over time, very little of this today is a result of specific investments in AI. It's coming. We're quoting a lot of projects...If you think about this, this massive increase in data that we're all generating, consuming and storing, that's really what's driving the growth in data centers today. In AI, I would tell you, it fell largely a future. And in fact, when you look at the total backlog today, of data center projects close to $140 billion. And if you look at that in the context of historical build rates, that's eight years of production, and we haven't hit the inflection point yet for AI. So, we think what happens ultimately is that this market expansion and this build-out cycle just gets extended for quite a number of additional years." - Eaton CEO Craig Arnold

"Earlier this year, the IEA updated its projections for electricity consumption, noting that global demand for data centers driven by cryptocurrency and AI could double by 2026. This robust data center growth implies its annual electricity consumption could account for 4% of global energy demand. To put this in perspective, this would equal roughly the same amount of electricity used by the entire country of Japan. We believe natural gas will be essential to meet this growing power demand, which will be additive to the growth required for New Energy sources in the future. Therefore, the notable rise in generative AI could provide upside to our current expectations for natural gas demand to increase by almost 20% between now and 2040." - Baker Hughes CEO Lorenzo Simonelli

Here is how capex spend is tracking at the biggest five spenders with AI making the bulk of the growth...

@TheTranscript

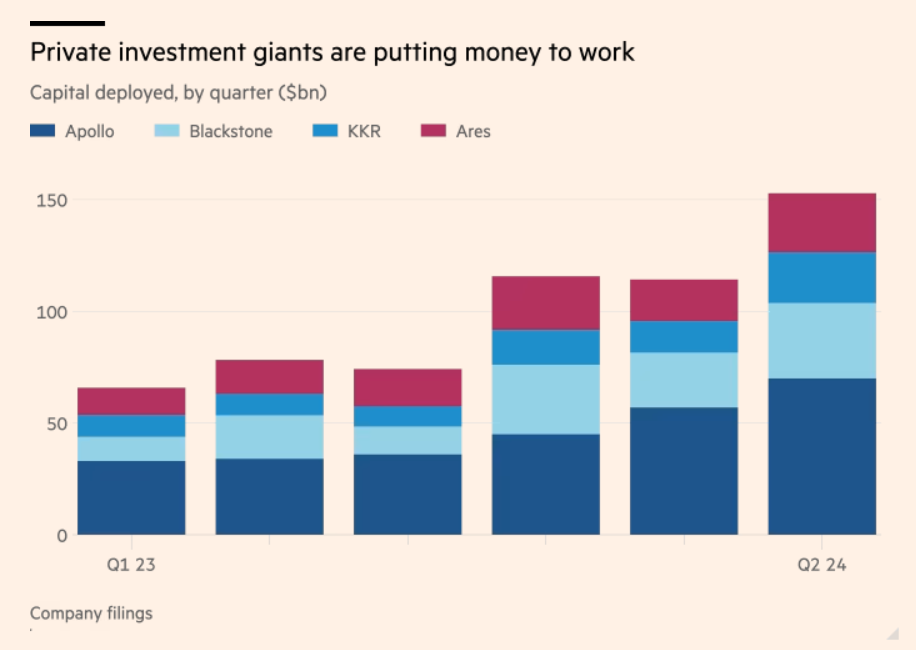

The big private market companies continued to have good things to say about the current environment...

"We are seeing significantly greater market activity since the beginning of the year. The macro inflation and rates backdrop has improved, markets are open, and the deal market is back. To give you a sense, globally, year-to-date, leveraged credit issuance is up over 100%, IPOs are up nearly 50%, and announced M&A is up approximately 25%. And given it typically takes a couple of quarters for the market to turn back on, these numbers understate the run rate activity we are feeling today. If this momentum continues, we believe you will see even more activity and announced deals and exits in the second half of the year. We are seeing this dynamic across our businesses." - KKR Co-President & Co-COO Scott C. Nuttall

And the PE Buyout deal market continues to pickup according to Q2 deployment data...

“My briefcase indicator continues to be getting full and indicates that there should be increasing solid levels of transaction activity,” Blackstone president Jon Gray said in a reference to the number of deal term sheets stuffed in his briefcase.

“The fact that we’re seeing rates coming down, markets being more conducive, more people are thinking about selling assets, I think as the IPO market reopens we should see more,” he added.

Credit-focused investment manager Ares also said it was seeing a pick-up in new buyout activity. Ares chief executive Michael Arougheti told the Financial Times that banks and private credit funds were increasingly being tapped to assemble new buyout financing packages instead of just refinancing existing debt or funding small acquisitions.

Speaking of, here is a Russell 1000 and S&P 400 component choosing to go private in a near $9 billion deal...

RCM To be acquired by TowerBrook and CD&R for $14.30/shr in cash, valuing it at $8.9B Announced that it has entered into a definitive agreement to be acquired by investment funds affiliated with TowerBrook Capital Partners and Clayton, Dubilier & Rice (“CD&R”), in an all-cash transaction with an enterprise value of approximately $8.9 billion.

TradeTheNews

And a Russell 2000 component going private after a rough three years of being public...

Thoughtworks (TWKS.O), opens new tab on Monday agreed to be taken private by Apax Partners in a deal worth about $1.75 billion, the technology consultancy firm said, nearly three years after its stock market debut. The private equity firm will purchase all the outstanding shares of Thoughtworks common stock that it does not already own for $4.40 per share. The offer by funds affiliated with Apax represents a premium of about 30% to the Thoughtworks stock's last closing price. Shares of the Chicago-based company rose 26.8% in premarket trading. The company's stock has lost 87% of its value since the start of 2022.

Here is Thoma Bravo looking to making a spike in the Q3 PE fund distribution numbers...

After a relatively barren few years for deals, backers of the world’s biggest private equity firms have one thing on their minds: returns.

For Thoma Bravo, the Chicago-based buyout group known for its big bets on enterprise software, a couple of transactions announced across a few days in late July is helping the firm to buck the logjam narrative that’s plaguing the buyouts industry.

The firm sold education software provider Instructure Holdings Inc. to KKR & Co. for $4.8 billion including debt and 50% of its stake in exchange operator Nasdaq Inc. for $2.7 billion. Those transactions generated realizations of about $2.9 billion and $2.4 billion respectively, according to a letter to Thoma Bravo’s investors reviewed by Bloomberg News. The fund had owned almost 84% of Instructure’s outstanding shares.

Thoma Bravo also “completely closed out” its investment in software observability platform Dynatrace Inc., according to the letter.

Soon, portions of the U.S. will be uninsurable...

Without the states or federal government having the resources to step in, these neighborhoods will become wasting assets as people leave. Choose your next homestead property and its location to natural disasters wisely. We cannot fight mother nature.

Natural catastrophes caused about $62 billion of insured losses in the first half of 2024 — roughly 70% above the 10-year average — as extreme wildfires, droughts and floods upend historical norms.

The data, which were compiled by Munich Re, show that “weather catastrophes in the US” dominated losses in the period, Tobias Grimm, the reinsurer’s head of climate advisory, said in a phone interview. Other developments of note include “floods in regions where they are very rare, such as Dubai,” he said.

“It is clear that climate change plays a role in this development,” Grimm said.

In all, natural catastrophes caused $120 billion of losses in the first six months, with little to indicate that the rest of 2024 will offer much respite. That’s as meteorologists predict one of the most active hurricane seasons in recent years, while wildfires raging from California to Alberta have left large parts of North America in shock.

Alexa, I need a flight to New York and a room at The Continental for September 2025...

“Their instant chemistry and their shorthand and their friendship is going to be so valuable,” Lloyd said of Reeves and Winter in an interview. “This is a very deeply complex play, as we all know, but it’s also a very funny play, and they’re very witty people and their shared sense of humor in those movies and in real life is going to be very beneficial to the production.”

In “Godot,” Reeves will play Estragon and Winter will play Vladimir, who banter and bicker while waiting for a mysterious figure who never arrives. “Those characters take solace in their companionship as they stumble toward the void,” Lloyd said, adding, “that’s going to be the central thesis of the production, with Keanu and Alex’s own friendship.”

“Waiting for Godot,” by the Irish playwright Samuel Beckett, was first staged in French in 1953 and then in English in 1955. The play was first performed on Broadway in 1956, and has been revived there three times since, most recently in 2013 with Ian McKellen and Patrick Stewart.

Learn more about the Hamilton Lane Strategies

DISCLOSURES

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Hamilton Lane is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Hamilton Lane.